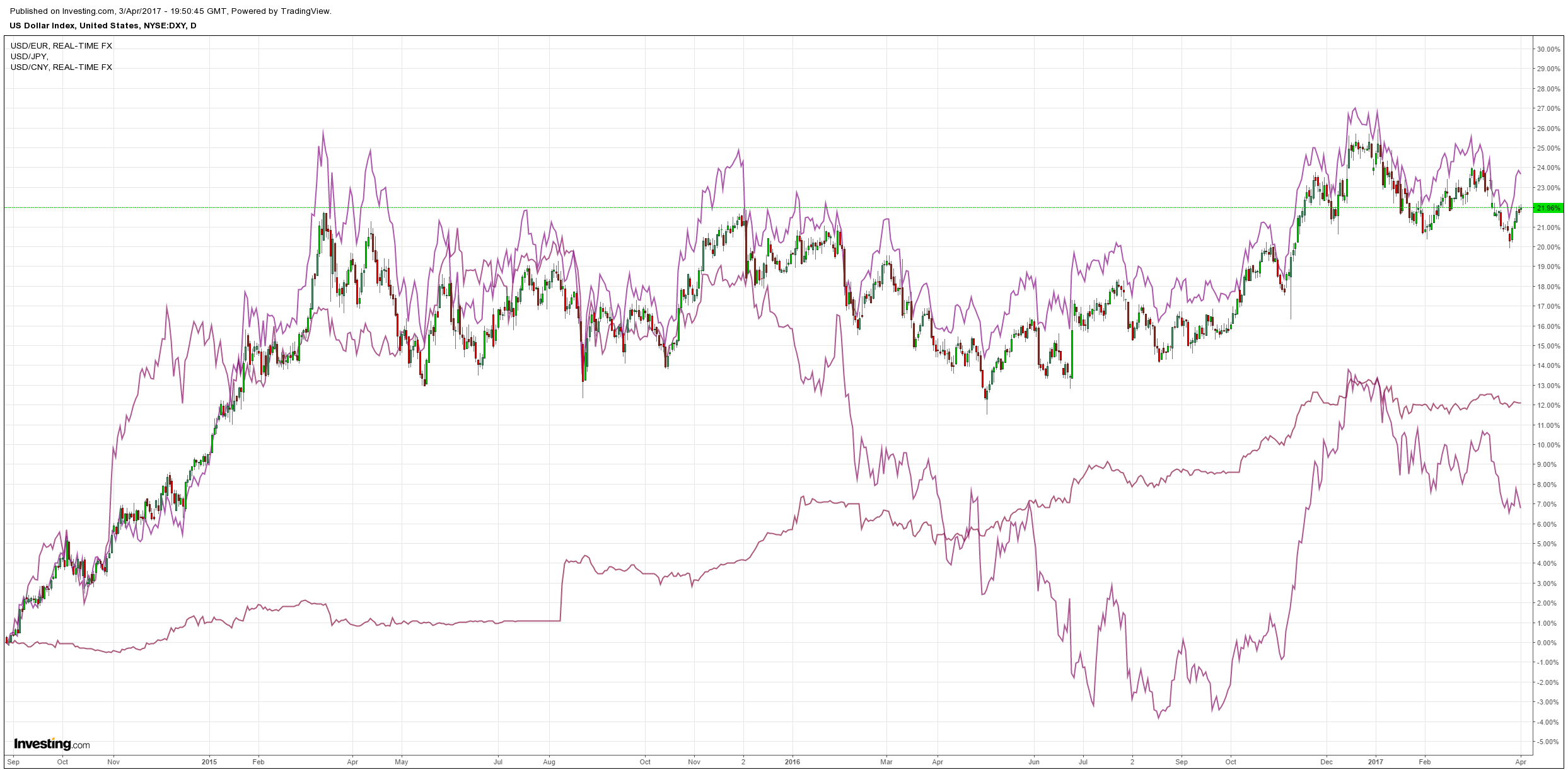

Gold is strong and near breakout despite the recovering DXY:

Advertisement

Oil was hit:

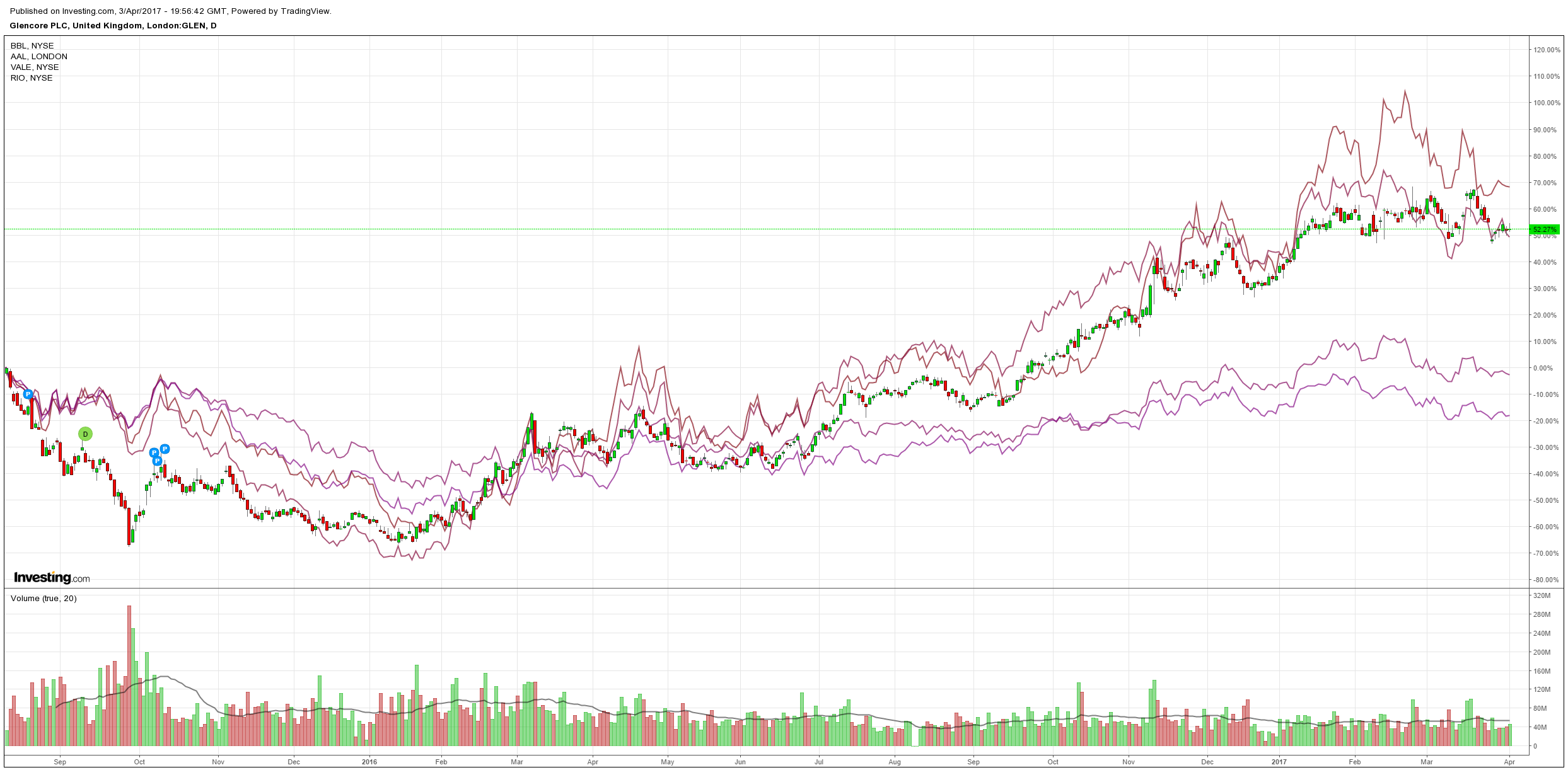

Base metals were thumped:

Big miners fell:

Advertisement

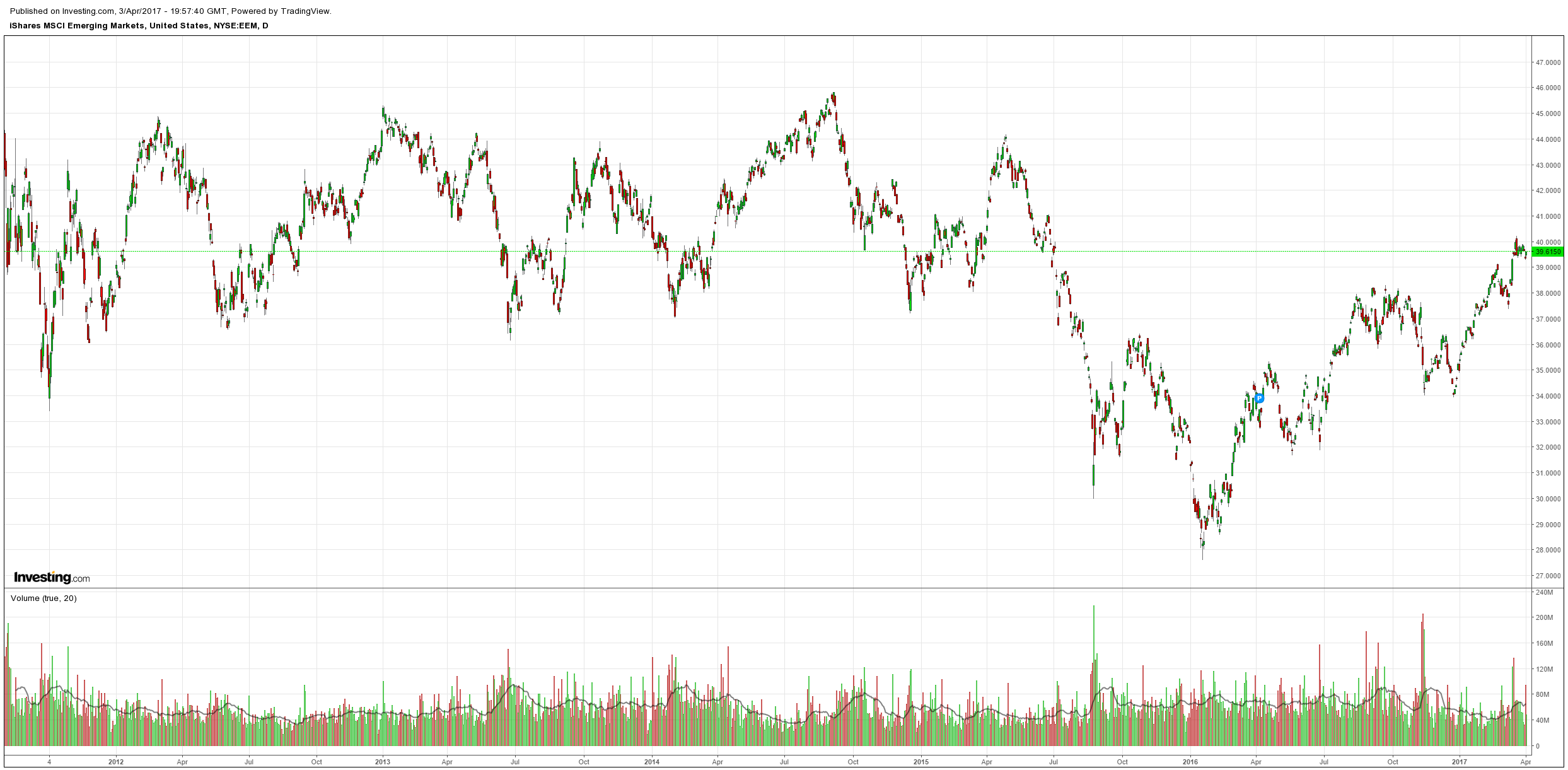

EM stocks bounced:

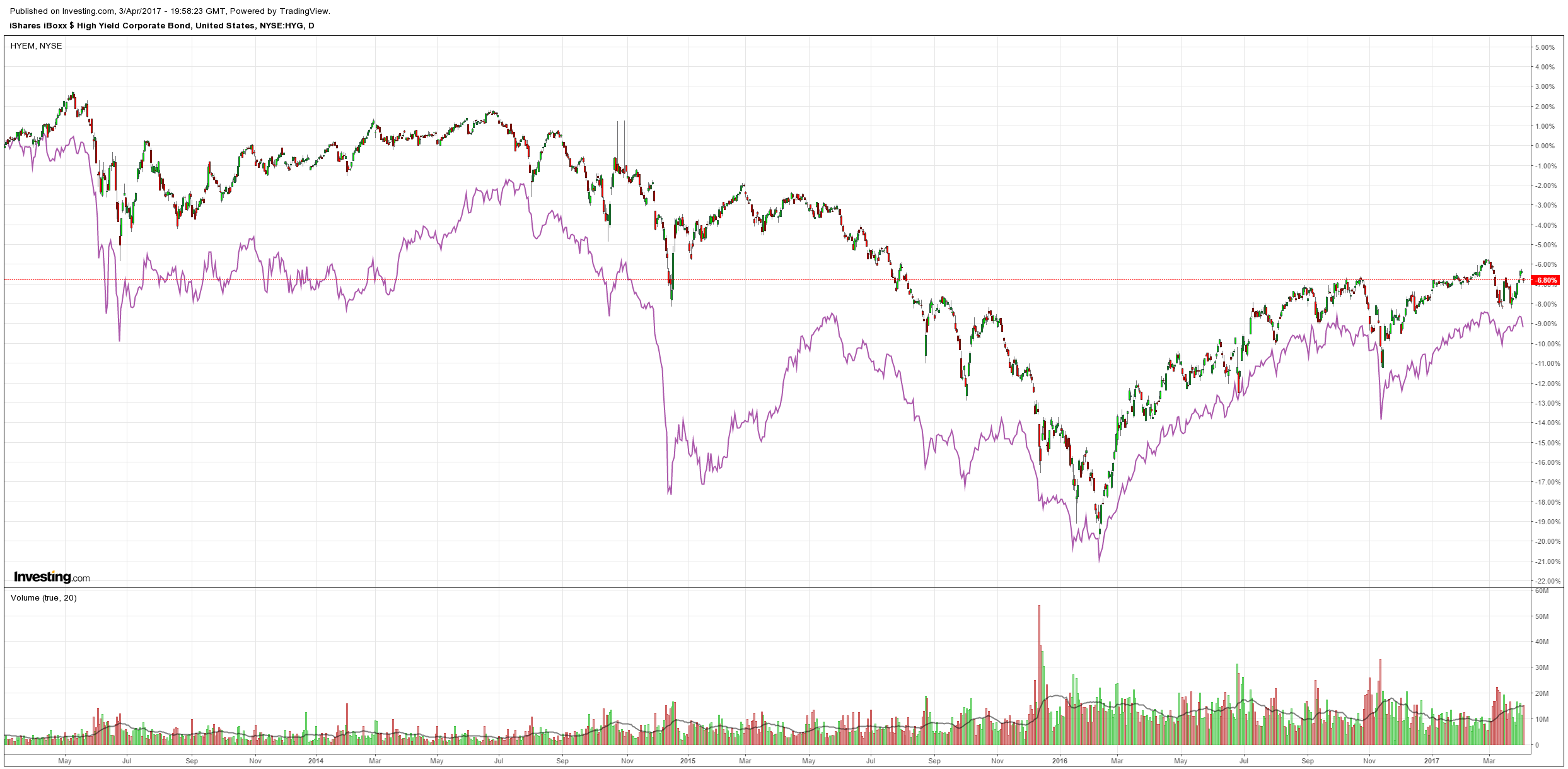

High yield do not:

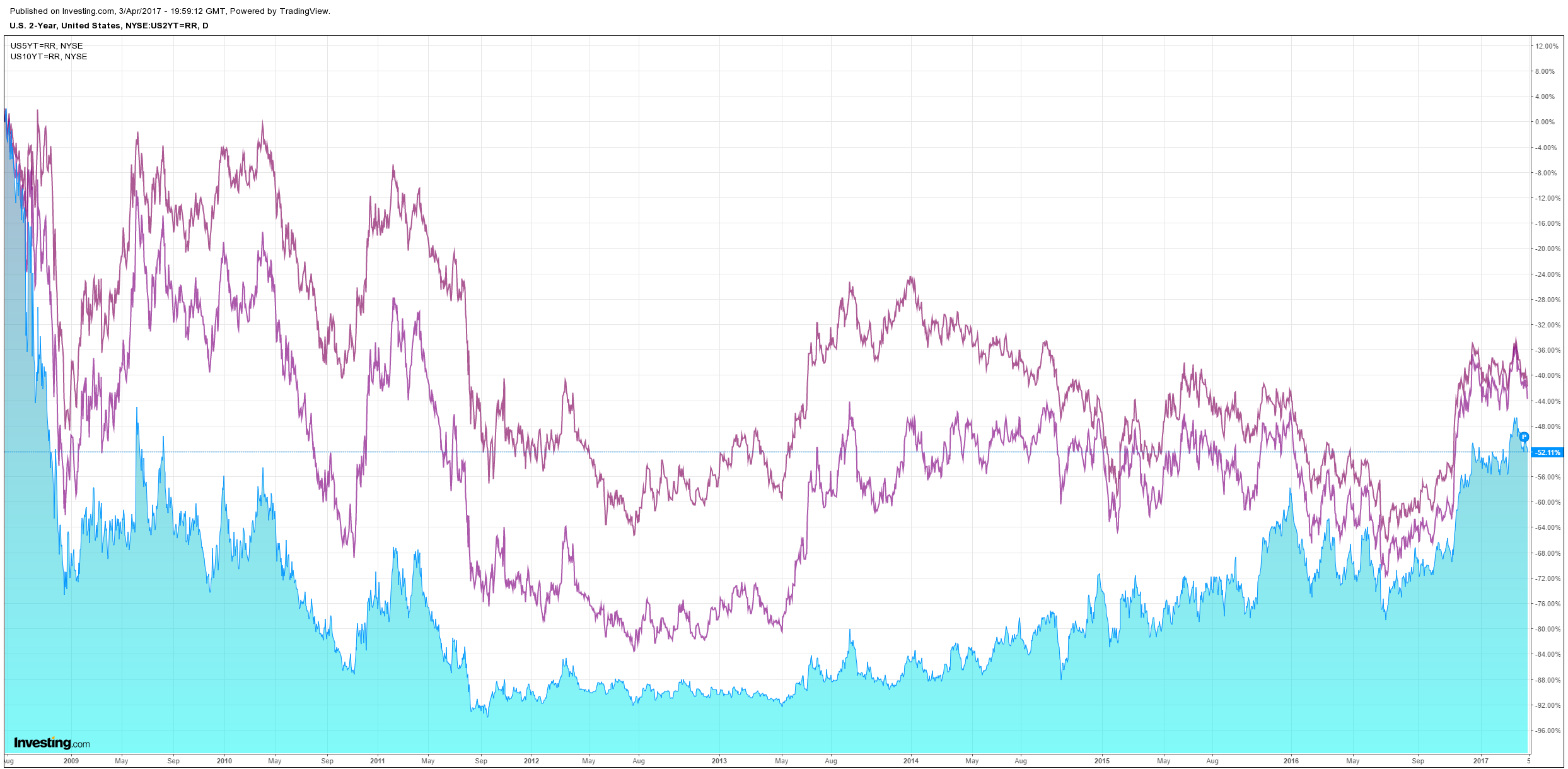

US bonds were bid:

Advertisement

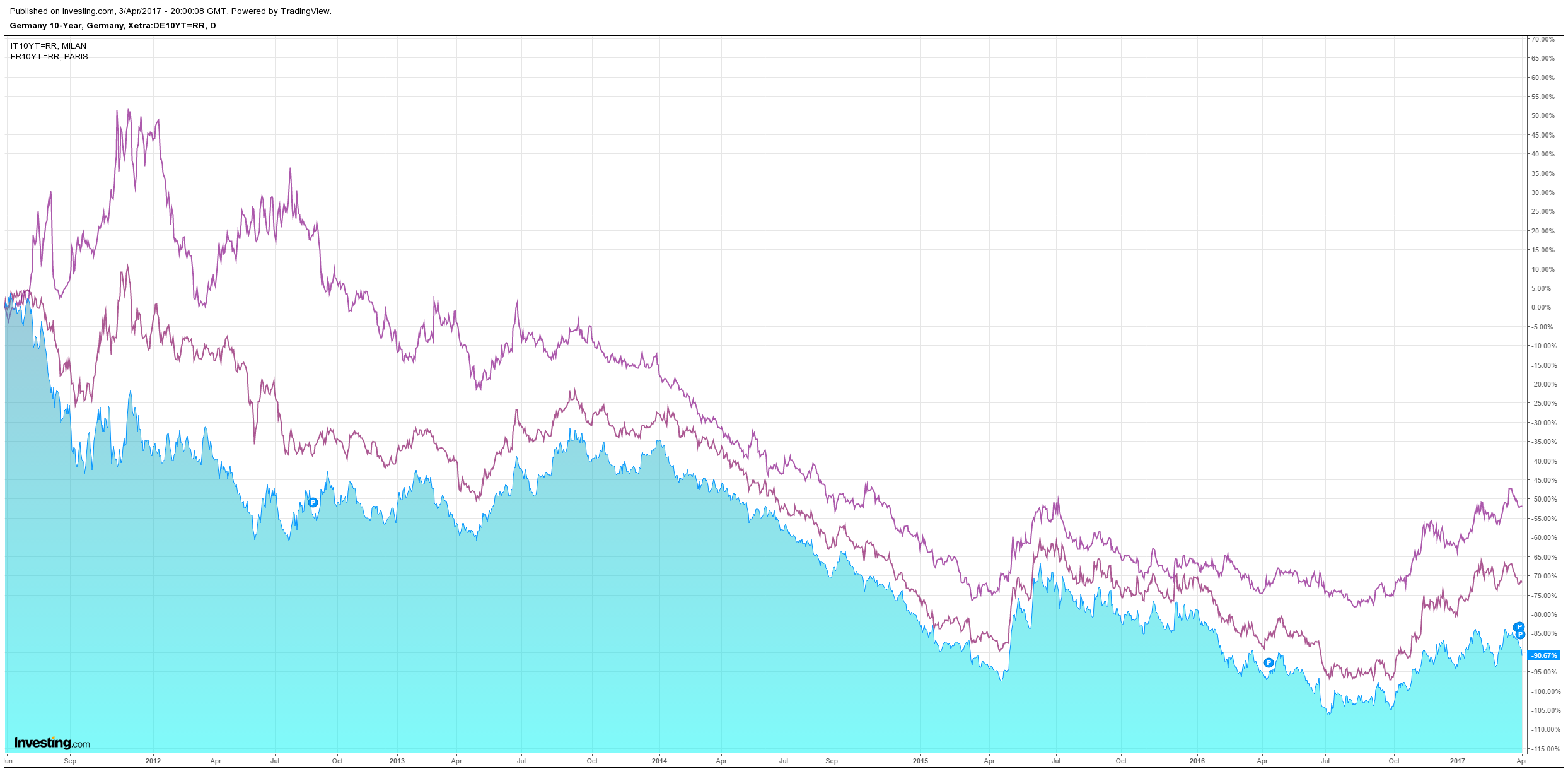

European spreads exploded:

And stocks took a decent hit before rebounding:

This is quite an odd mix but I reckon we can make sense of it via this at the FT:

Advertisement

Donald Trump has warned that the US will take unilateral action to eliminate the nuclear threat from North Korea unless China increases pressure on the regime in Pyongyang.

In an interview with the Financial Times, the US president said he would discuss the growing threat from Kim Jong Un’s nuclear programme with Xi Jinping when he hosts the Chinese president at his Florida resort this week, in their first meeting. “China has great influence over North Korea. And China will either decide to help us with North Korea, or they won’t,” Mr Trump said in the Oval Office.

“If they do, that will be very good for China, and if they don’t, it won’t be good for anyone.”

But he made clear that he would deal with North Korea with or without China’s help. Asked if he would consider a “grand bargain” — where China pressures Pyongyang in exchange for a guarantee that the US would later remove troops from the Korean peninsula — Mr Trump said:

“Well if China is not going to solve North Korea, we will. That is all I am telling you.”

Bellicose stuff. I guess this moment was always going to come. It’s one thing to have the great salesman reforming tax, it is quite another to have an deeply inexperienced and iconoclastic narcissistic celebrity with his finger on the Big Red Button. Safe havens were rightly bid in the USD, bonds, gold and bunds. Risk assets got hit, especially those most closely related to China, that is, commodities.

If this develops, and it rather looks as if it might, then you can expect those trends in buying and selling to accelerate. JPM is confident in buying the sip:

Advertisement

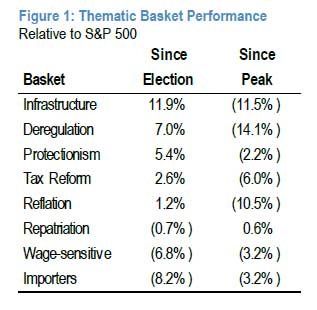

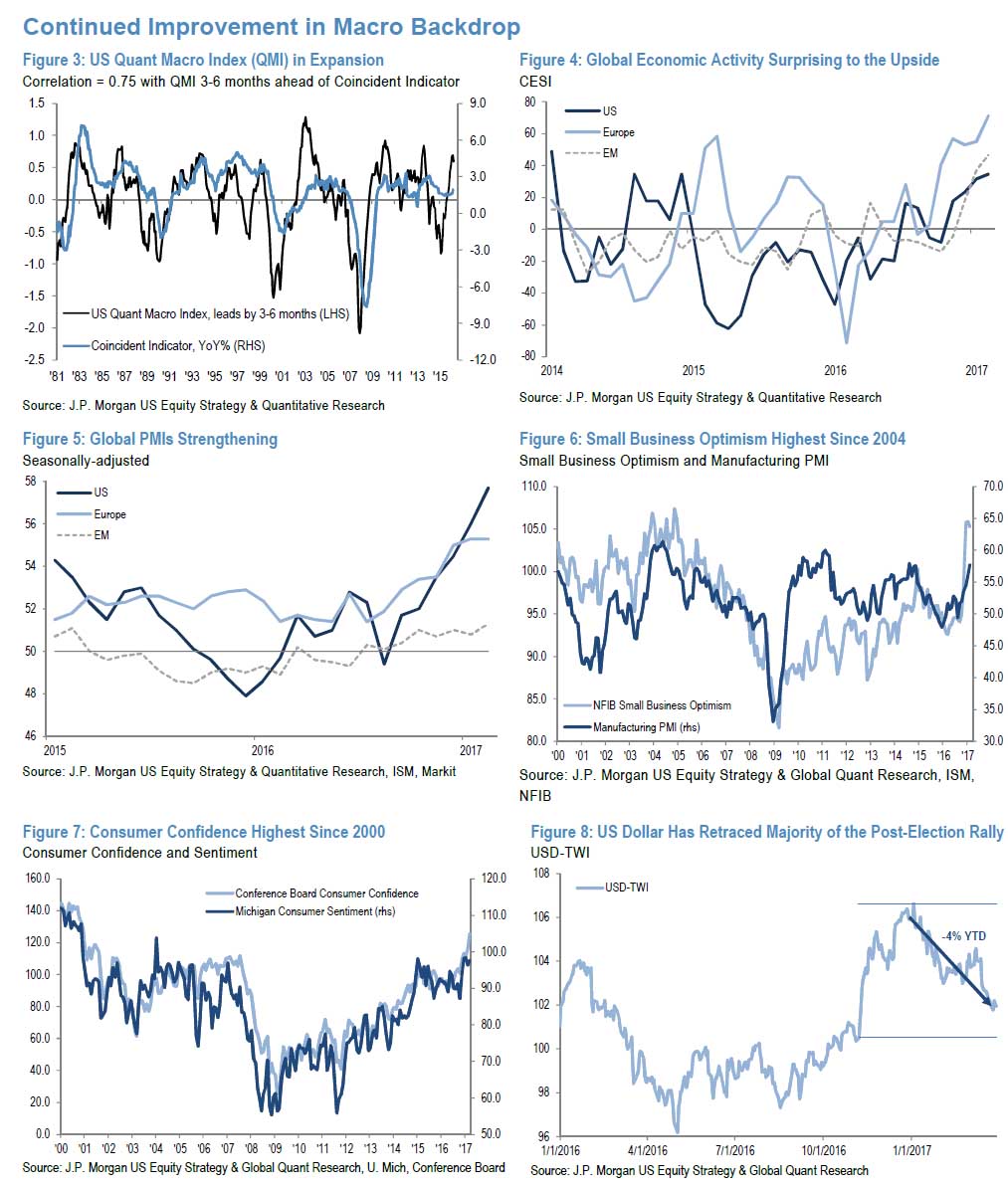

After S&P 500 touched our price target of 2,400 in March, we argued that the market could face higher volatility and some weakness in the short-term at a time when both fundamental and systematic investor positioning was stretched. While the broader market fell by ~3% from the peak, there has been more pronounced weakness in trades tied to reflation and Trump’s agenda (see Figure 1).

Uncertainty around the upcoming French election and lack of clarity on timing of the US tax reform could continue to weigh on the market in the near term. However, we see limited risk of a larger pullback and recommend buying the dip(s).

The market is likely to remain resilient and supported by the Trump and Fed “puts” as well as the continued improvement in the fundamental backdrop both domestically and abroad. On balance, we continue to maintain a broadly constructive view. If anything, we see a confluence of conditions potentially coming together in the months ahead and setting the stage for the market to reach new highs.

Policy remains a source of upside risk for equities. As detailed in our 2017 Outlook, a key source of upside risk to our price target is the passage of corporate tax reform. The failed AHCA bill last week has led investors to question the administration’s legislative efficacy. In our view, the lack of sufficient GOP support to replace ACA is not necessarily a negative for equities. Instead, the failed vote could potentially pull forward the timeline for the tax reform, which has broader and more bipartisan support than the healthcare bill. Currently, the market does not seem to be pricing in much upside from pro-growth policy reforms. Equities tied to Trump’s agenda have unwound most of their post election gains: deregulation (JPAMDREG -14% from peak relative to S&P 500), corporate tax reform (JPAMTAXP -6%), and infrastructure spending (JPAMINFR -12%), see Figure 1. We recommend investors to opportunistically add exposure to these themes.

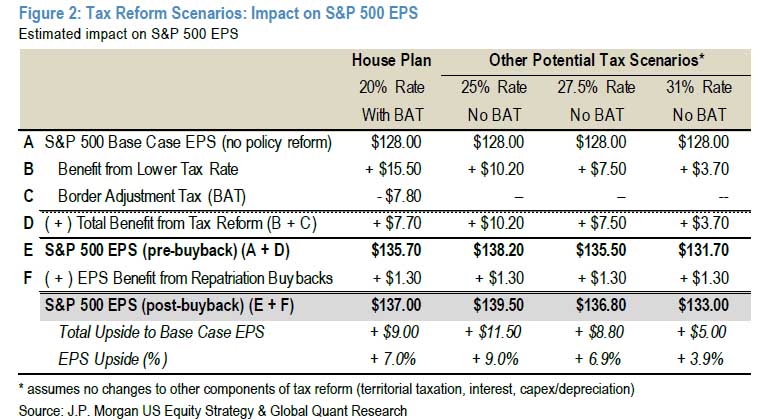

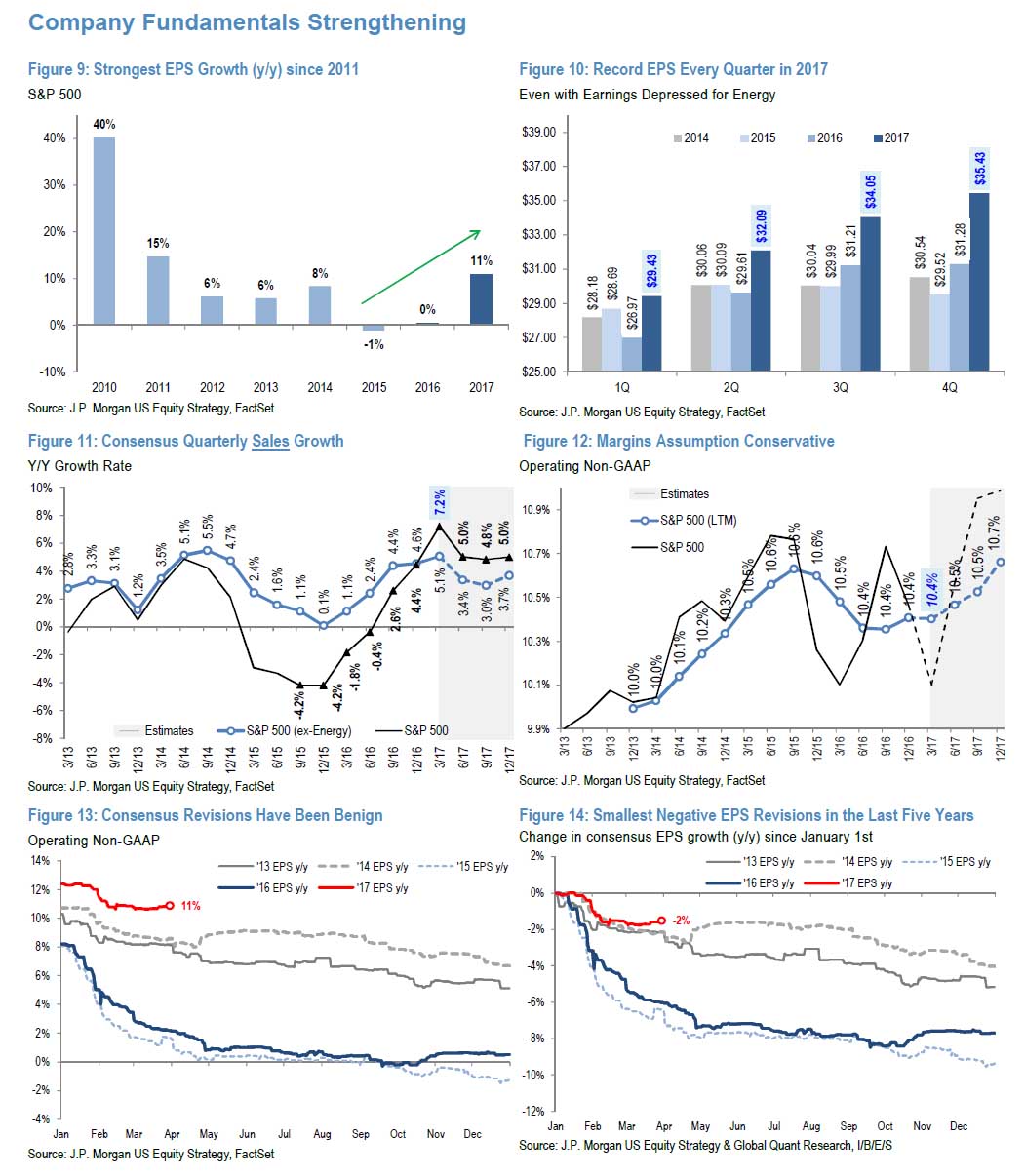

Even if the Tax Reform Blueprint pivots to a less ambitious plan, we still see upside for earnings and equity values. For instance, implementing a tax rate of 27.5% (midpoint between current 35% and original GOP 20% rate) and excluding the highly controversial BAT, we estimate should add $8 to S&P500 EPS, see Figure 2.

In an even more conservative scenario where the tax rate is cut by only 4% (similar to the last Reagan tax cut in 1986), EPS should still increase by $4. While the reduction in statutory tax rate should accrue mostly to domestic companies, a move to a territorial system including cash repatriation should benefit US multinationals. If multinationals were to onshore ~$1 trillion of foreign cash, we estimate this would lift S&P 500 EPS by an additional ~$1.30. At the current 18.5x P/E multiple, the total EPS boost of ~$5 is worth an incremental ~100 points for S&P 500. With the market trading near our policy-neutral YE 2017 price target of 2,400, we see little of Washington’s agenda priced into the market currently. Also, if infrastructure spending is included in some form with the tax plan, there could be further upside to our EPS estimate. While there is still much ambiguity around this plan, the Trump administration could gradually release details ahead of the more comprehensive budget proposal in May.

Downside risks of higher rates and stronger USD contained for now. On the whole, Fed’s stance remains relatively balanced, while global growth continues to improve and USD reverses from peak levels. With the unemployment at the natural rate of 4.7% (the job market is neither too hot nor too cold) and core inflation still running below 2% target, the Fed sees near-term risks to the economic outlook roughly balanced (i.e. “goldilocks” economy) and continues to reiterate that the path of future hikes will be data dependent. Furthermore, it is not unreasonable to expect that President Trump (as is often the case with incumbent presidents) might appoint more dovish members to the Federal Reserve Board. There are two vacancies already and perhaps two more likely to open in the next one year on the seven-member board. The year to date weakening USD trend could also be further reinforced especially if ECB and/or BOJ signal(s) gradual reversal in monetary policy, allowing interest rate differentials to narrow. Further weakening in USD would likely result in positive earnings revisions given that the consensus view in FX markets is still mostly biased towards stronger dollar. We estimate that for every ~2% decrease in the USD TWI, S&P500 EPS should be revised up by ~1%.

Earnings recovery is resilient and we remain confident in our policy neutral EPS of $128 for 2017. After S&P 500 companies delivered a record-high EPS of $31.28 in 4Q16 (+6.0% y/y), we are expecting growth to accelerate further to >10% in 1Q, highest growth rate since 2011. Additionally, company guidance activity has been encouraging YTD, which reflects strengthening global growth, healthy labor market as well as strong business survey data and consumer confidence (at 16yr high). To reflect this improvement, the Street’s revisions have been much more benign so far YTD compared to recent years. This supports our view for a high-single-digit EPS growth this year driven by mid-single-digit organic sales growth, minor margin expansion (due to improving operating leverage and expense rationalization) and continued share repurchases.

That seems fair enough to me, though I remain more bullish on the USD. But these “buy the dip” theses will not hold up if the good ship US sails into battle against North Korea with Captain Donald Trump at the helm. The idea of the Pacific’s two great powers coming into close proximity within a theater of conflict in the East and South China Seas is not pretty, even if they mull helping one another along the way.

One thing of note is that for those long US stocks from Australia, if this gets moving I would expect the USD to be bid and the Aussie to get clubbed, so there is some built in hedge.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific's leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.