You can always tell when the heat is on global credit markets by the mushrooming number of articles celebrating Australian bank strength. Chanticleer leads us off:

Australia’s big four bank stocks stand out like knights in shining armour in a world left dazed and confused by Britain’s vote to leave the European Union.

After several months being pounded in the heat of the election campaign events are starting to turn in the bank’s favour, including the fading prospect of a Labor Party victory on Saturday.

The first and most obvious positive development for the banks is the Brexit vote because it provides a valuable reminder of the strength of the Australian financial system and their attractiveness in terms of profits and dividend yield.

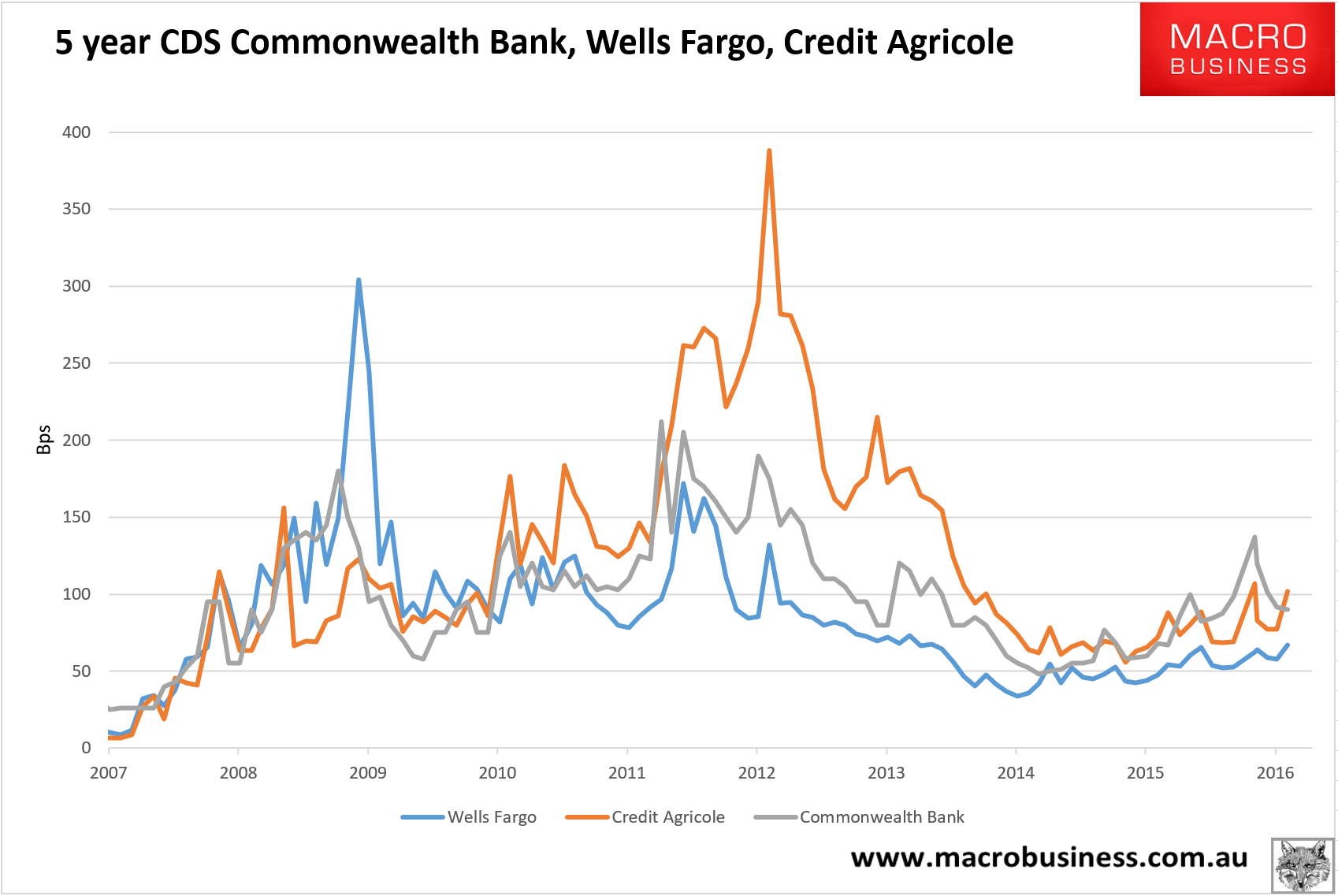

That’s laying it on a bit thick isn’t it? The first thing markets think of when there’s global credit uncertainty is that Australian banks owe them a lot of money. Hence, when a British butterfly flaps its wings Australian bank funding costs take off. Thankfully, CBA CDS did not add to Friday’s gains yesterday but neither did our European and US proxies:

Banking stocks in Europe and Britain plunged again overnight amid concern about the effect the Brexit vote will have on the already under-pressure sector, but the threat to Australian banks is “tiny”, Aurora Funds Management says.

Shares in some of Europe’s biggest banks have shed more than a third of their value in just two days of trading. The heaviest losses overnight were felt in British and Irish banks. The Bank of Ireland fell 20.9 per cent, down 38 per cent over two days, while Barclays dropped 17.4 per cent, capping off a two-day slide of 32 per cent.

But Hugh Dive, portfolio manager at Aurora Funds Management, said the direct impact on Australia’s big four banks would be minimal, apart from some selling on negative sentiment in the sector.

“Is [Brexit] impacting credit markets in the short term and their ability to access finance? No, this is not the GFC,” he said.

“The banks are in a better funding position than in 2007, they are less reliant on wholesale funding from Europe,” he said.

Note to self, short Hugh Dive. We don’t know what Brexit is yet. But the clear risk is that it will trigger an existential crisis for the euro which would be much worse than the GFC. The next crucial event in determining the future of the zombieuro is twelve months away in the French election. At what point will markets begin discounting the influence of the National Front? Are they doing it now? Or is this this just Brexit fallout? I don’t know and neither does Hugh Dive. From Karen Maley:

Can Europe’s political leaders convince their disgruntled populations that the region still has a united and prosperous future?

In the wake of the Brexit vote, leaders from Germany, France and Italy overnight tried to present a common front, promising to set new policy priorities and to unveil fresh programs aimed at increasing economic growth in an attempt to rekindle flagging support for the European Union.

“We must do everything in our power to prevent a strengthening of centrifugal forces”, German Chancellor Angela Merkel said at a news conference in Berlin.

But the continuing turmoil in global share markets shows that investors are deeply worried about the future of the European project. Populist, anti-EU parties in the Netherlands, France and Italy are already demanding referendums, similar to the one in the UK.

And this worry is showing up in a continuing slide in the share prices of European banks. Italy’s Intesa Sanpaolo, for instance, fell a further 11 per cent in trading overnight (it has now fallen 55.4 per cent in the past year), while French banks Societe Generale lost 8.4 per cent (down 40.7 per cent in the past year), and BNP Paribas fell 6.3 per cent (its share price is down 36 per cent in the past year). Meanwhile, Germany’s Deutsche Bank fell 6.2 per cent overnight, bringing its decline in the past year to 56.5 per cent.

And from Goldman some landscape:

The outcome of a fragmenting euro is a disaster for the global economy and would result in:

global bank Balkanisation;

outright chaos in global funding markets with unimaginable counter-party risk;

global banking equity wreckage;

neutered central banks;

and, the demolition of any economy reliant upon external funding (especially if it is bank based).

It has nothing whatsoever to do with whether or not Australian banks are funded from Europe. It is simply the case that anyone holding the second largest reserve currency on earth, or assets denominated in it, will have to discount those holdings in some very large measure resulting in global banking chaos.

We’ve been bearish on the Aussie banks for several years anyway given excessive payout ratios and the various domestic risks. But I put it to you that the above outcome is best understood in reference to the kind of events that have been seared by pain into collective national myth, such as the external shock of the 1890s that collapsed the Melbourne land bubble and took 75 years to see the same prices again.

If you have significant Aussie bank exposure you need to be either shortening or hedging it.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific's leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.