What a wonderfully hopeful species the human being is! After one day the Brexit fallout has been quite limited. The US dollar was strong but not insanely so:

Yen was strong but euro only modestly weak:

Commodity currencies fell but not far and the Aussie least of all:

Advertisement

Gold jumped to new rebound highs:

Oil took a decent hit:

Advertisement

Base metals yawned:

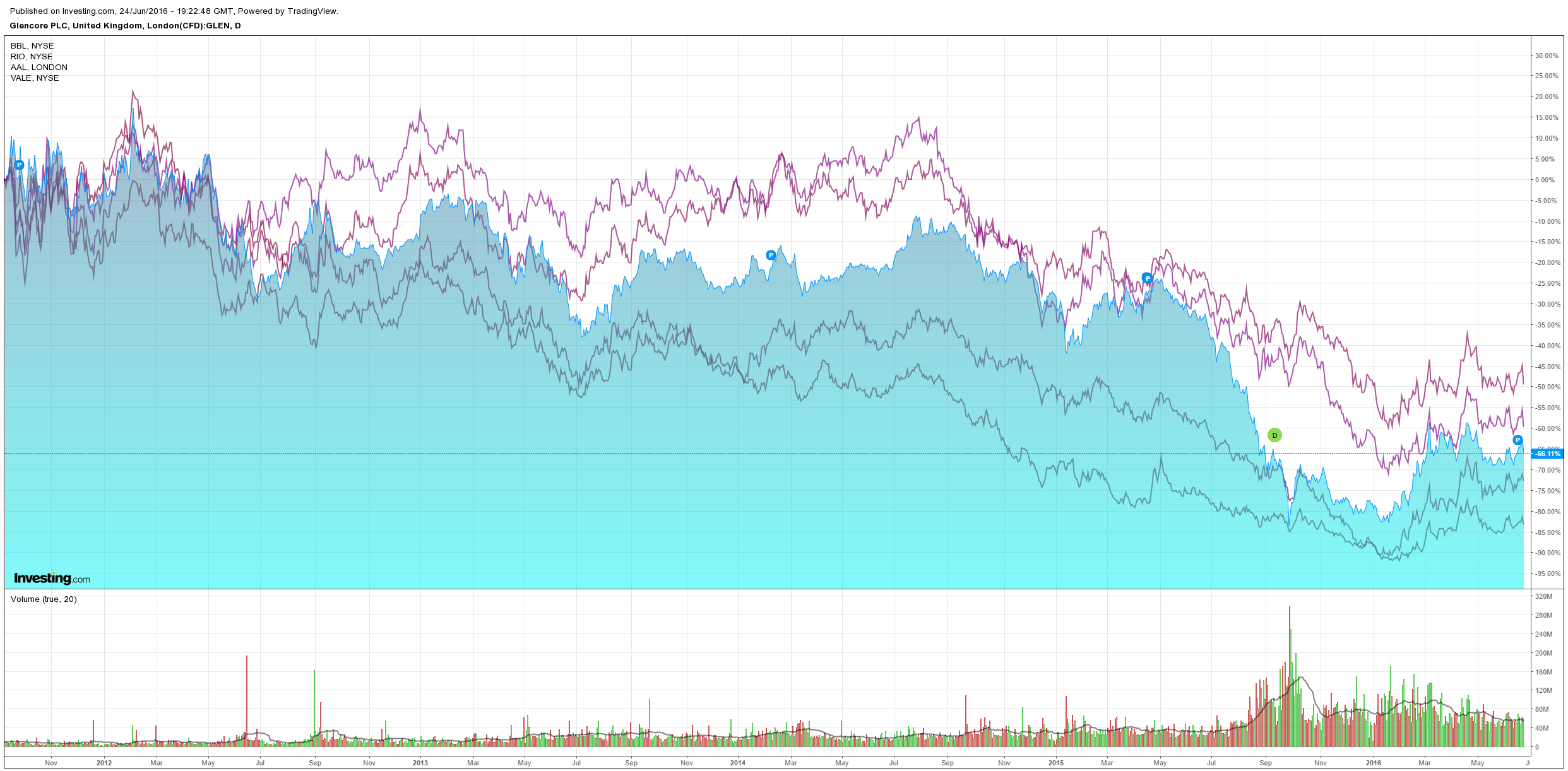

Miners fell but much less than here:

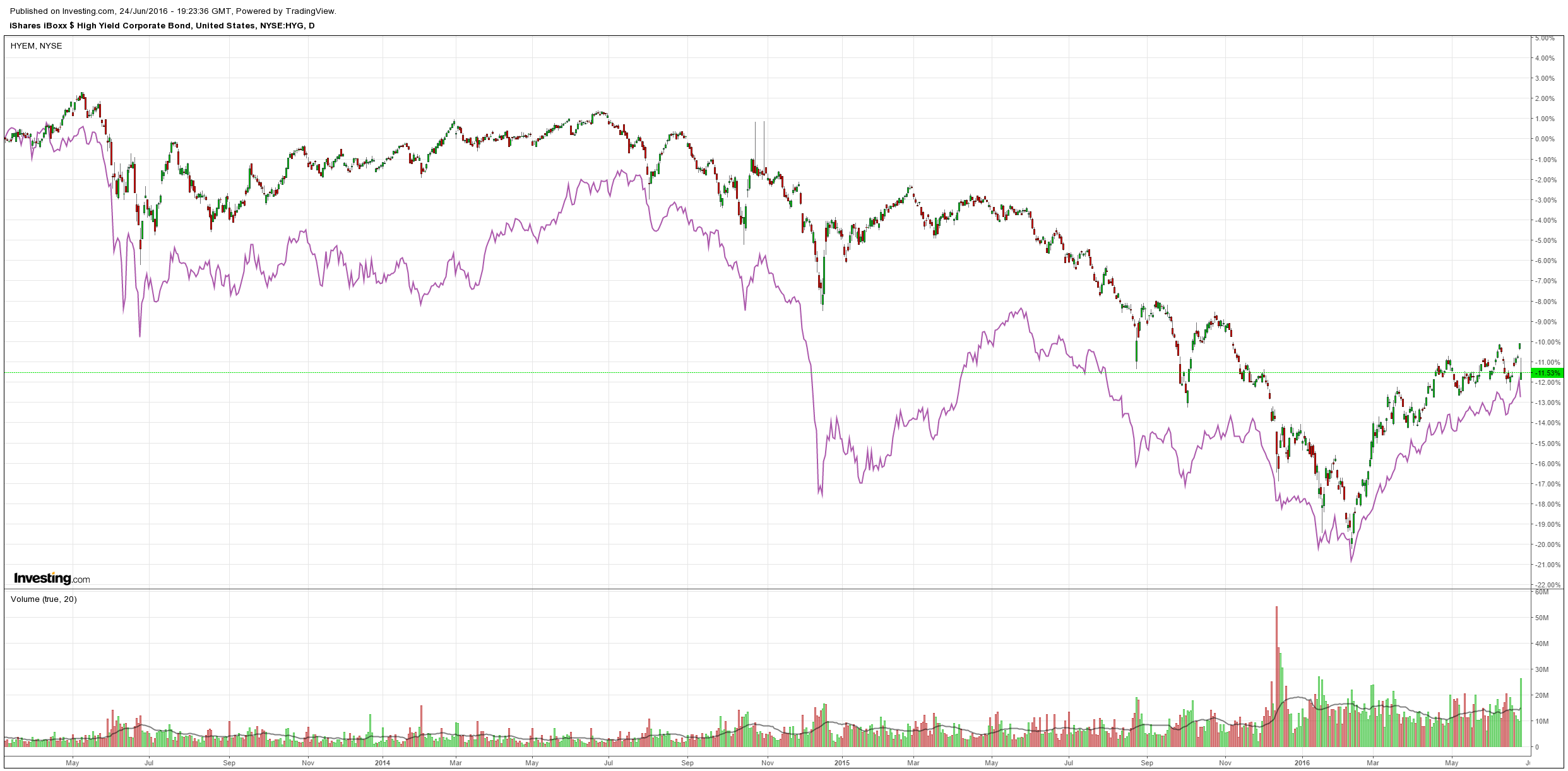

And US/EM high yield was whacked but not in an alarming way:

Advertisement

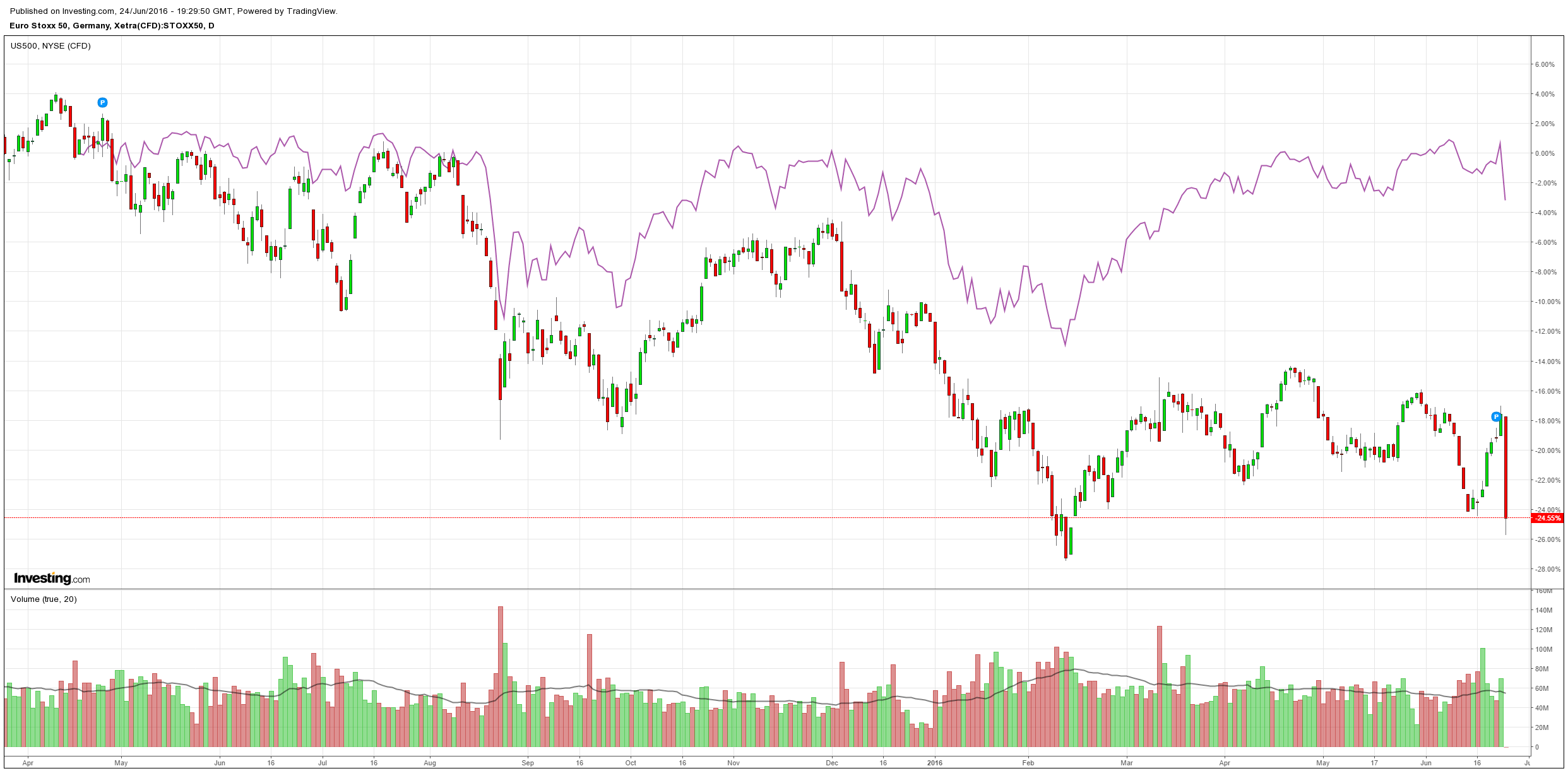

European stocks fell pretty hard at -8% but S&P500 only fell -4.2%:

Advertisement

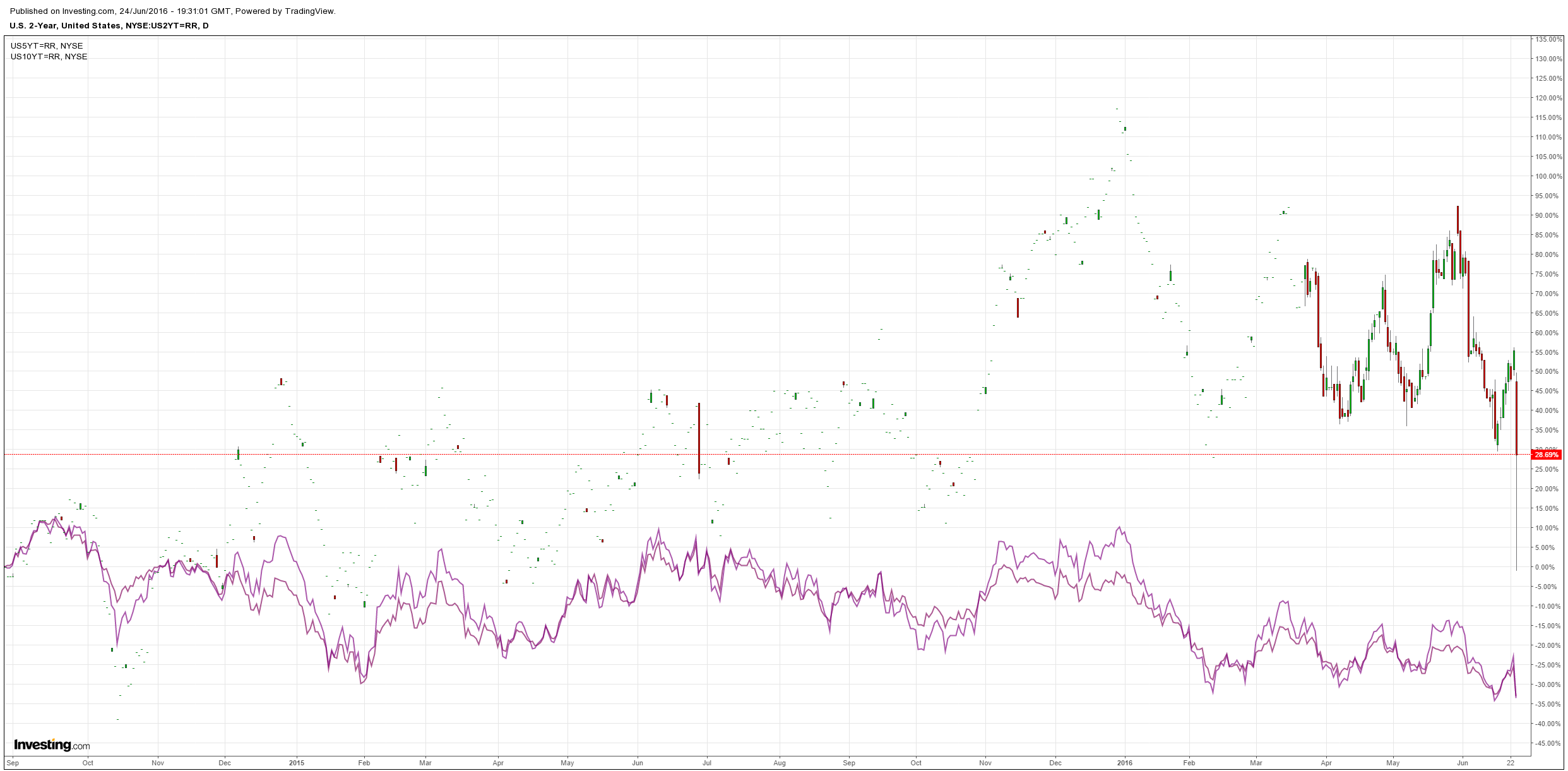

And after their initial crash, bonds yields recovered half their losses:

All in all, it’s probably about the right reaction so long as you’re only looking at the short term implications. Below I’ve excerpted some sell side research that more or less sums up the price moves. MS looks at the hit to Britain:

Advertisement

Key consequence – profound and protracted uncertainty: Although the final votes arestill being counted, it looks increasingly clear that the UK has voted to leave.Following this vote, weexpecta surgein political and economic uncertainty. Initially, we expect the focus to be on the political uncertainty, especially around whether Cameron continues as Prime Minister,and whether the Conservatives can maintain a working majority in parliament.

Further down the line, we see a heightened risk of a second Scottish independence referendum. Economically, we see uncertainty regarding the UK’s future trading relationship with the EU, its main trading partner, where we see a risk of a significant reduction in market access.

Economic impact – a hit to sterling and demand; a less open and more volatile economy: We think that the uncertainty after a vote to leave will have two immediate effects. First it will hit sterling,as uncertainty reduces nonresidents’ appetite for UK assets against the background of the UK’s record current account deficit. Second, it will hit growth, as firms hold back on investment, and households increase precautionary savings. Longer term, we expect a less open and more volatile economy, with reduced inflows of capital and labour,and a lower rate of potential growth.

JPM assesses the hit to European growth:

As we noted earlier today, the Euro area growth is likely to be hit by direct trade spillovers from the uncertainty hit to the UK. In addition, there is likely to be an impact on growth from lower Euro area confidence and financial markets. It is far too early to assess this with much confidence. In addition, the impact across Euro area countries is likely to operate through varying channels. Germany may be affected mainly via trade and uncertainty channels. In France, the trade impact is likely to be smaller but the uncertainty impact is likely to be amplified by existing fragilities and by next year’s presidential election. Trade channels are likely to be even smaller for Italy, while uncertainty effects and financial pressures on the sovereign and the banks (already under stress due to the high level of NPLs) may be larger. In Spain, uncertainty and financial shocks are likely to add to a shaky political outlook. Outside of Ireland, which is likely to be hit most severely, our inclination is to cut our growth forecasts by similar amounts across most of the region (see table below). Except in 2Q16 and 3Q16, where 0.25%pt of the forecast change relates to tracking/momentum, the remainder is entirely due to the Brexit shock. Hence, we now see the Euro area economy growing at only a 1.25% pace for the next few quarters.

The only modest source of encouragement is that the business surveys look strong in June, at least outside of France, which may have been dragged down by strikes and flooding. Yesterday, the Euro area composite PMI rose solidly in the periphery, while the German details were strong with new export orders hitting a two and a half year high. Today’s IFO reinforced the sense of a solid pickup in Germany. The expectations index rose 1.4pts to a solid 103.1, driven by manufacturing. While this backwardlooking news is encouraging about the region’s cyclical recovery, it provides limited comfort at this stage given the size of the UK shock. Already in today’s IFO press release, a little more than a third of manufacturers expected some impact from the UK’s decision to exit the EU.

We also revised down our Euro are inflation forecast. Movements in the price of Brent and the currency since we released our latest forecast on June 16 are modest. However, our new growth forecast implies that core inflation will be lower during the course of 2017 than we previously expected (we left the 2H16 trajectory unchanged due to lags in the growth/inflation relationship). We previously expected core inflation to gradually increase to reach 1.3%oya in 4Q17. We now think core inflation will increase more moderately to reach 1.1%oya, which would be around two tenths lower than the ECB forecast. Our headline inflation forecast now assumes that headline inflation will reach 0.8%oya in 4Q16, and 1.2%oya in 4Q17.

Citi assesses the policy response:

Advertisement

Contagion vs Policy Response — This result will likely send shockwaves around political elites and financial markets. Risk off. We would not be surprised if European shares fell to February lows in a single session, down c10%; that has not happened in the last 40 years. Losses for international investors are likely to be exaggerated by FX moves (GBP, EUR). Contagion risk and our volcano thesis, ie investors such as HFs crowding and following price trends, have to be taken seriously. Failure to limit contagion could have dangerous consequences. Policy reaction is critical, but policymakers have less “room to act” than previously.

Most Likely Policy Responses — Citi economists: “In the short term, we expect major central banks and regulators to take steps in case of excessive market turbulence and to launch liquidity support measures. In the following days and weeks, we would look for the BoE to cut the Bank Rate by 25bp (at least by 14 July) and perhaps restart additional asset purchases. The ECB (21 July) and other European central banks will likely envisage a cut in their policy rate if FX strengthens or inflation weakens, resulting in an unwanted tightening of financial conditions. For the Fed, a delay in the next rate hike to Dec-16 or beyond is likely, in our view. Focus will be on the BoJ given the recent currency moves. In the event of disorderly currency moves, G7 central banks could launch coordinated FX interventions.”

How Low Can we Go? — Returning European equities to 2011-12 European Sovereign Debt Crisis P/E (Figure 9), P/B or DY (Figure 10) levels would imply falls of 40%, 20% and 10% from one week ago share price levels. A 40%+ fall would imply “significant and synchronised” global GDP and EPS recession and the return of widespread global systemic risk; we think this is unlikely for two key reasons: 1) post-vote (co-ordinated?) policy actions, and 2) less capital risk/leverage across US and (many) European banks. This should, in our view, limit downside risk to 10-20% from Thursday’s closing level. Risk levels have risen, uncertainty has risen, growth prospects have fallen. All negatively impact our equity targets in Europe. We lower our end-2016 and mid-2017 Stoxx targets to 310 and FTSE 100 targets to 6000; we see greater FX support in the UK in the absence of high-level systemic risk. We also lower exposure to European Financial sectors (see report for details).

All pretty modest so far and Capital Economics is positively sanguine:

Not surprisingly, the outcome of yesterday’s referendum in the UK has hit sterling hard and driven down the prices of equities and most commodities. At the same time, it has boosted the “safe-haven” appeal of the yen, high-grade government bonds and gold. Nonetheless, some of the initial moves have already been partially unwound, and, in some cases, we expect them to be more than reversed. • The initial knee-jerk reaction in the markets clearly reflects the fact that a vote to remain had been heavily discounted. For example, sterling’s depreciation against the dollar, to a low of $1.32/£ this morning from just above $1.50/£ late last night (UK time), was preceded by a gradual appreciation from $1.40/£ on 16th June, when the polls pointed most clearly to a “Brexit”.

• Nonetheless, the exchange rate has already rebounded to above $1.38/£ at the time of writing, as the rhetoric of pro-Remain policymakers has changed from “Project Fear” to “Project Reassure” and it has dawned on investors that a long period of negotiation, rather than sudden upheaval, now lies ahead.

• In particular, while signalling his intention to step down, the UK Prime Minister has stressed that his successor will trigger Article 50. As a result, the formal process of the UK’s withdrawal from the EU may not even begin for a few months. And the Governor of the Bank of England has emphasised both the health of the UK’s financial system and the Bank’s willingness to provide support where needed.

• We warned a long time ago that the exchange rate might fall to $1.20/£ in short order in the event of a “Brexit”. In light of this morning’s developments, a decline to this level now looks unlikely. That being said, we would be surprised if the exchange rate didn’t fall back a little once the dust has settled.

• A key reason is our view of monetary policy. Investors have wasted no time in discounting more easing in the UK and less tightening in the US. However, there has not been that much change in the spread between expected interest rates in the two countries. Our view is that this spread is likely to be greater than investors are assuming, even today. Admittedly, the Bank of England’s MPC might not ease further if the markets settle down. But we think such calm would clear the way for the FOMC to tighten by much more than discounted in the markets, as inflation in the US picks up steam. And if the economic consequences for the UK do prove to be as adverse as many warned before the referendum, then the need for looser monetary policy will surely be much greater there than across the Atlantic.

• We also expect the outcome of the vote to have more of an influence on the policy of the ECB than on that of the Fed, given the closer economic and financial ties to the UK of the euro-zone than of the US and the risk that the vote could heap more pressure on the troubled countries of the euro-zone. It could have more of a bearing on the policy of the BoJ too, despite Japan being on the other side of the world. This is because the additional strengthening of the yen increases the chances that Japan’s central bank will ease policy further in order to bring her currency back down.

• If we are right about the prospects for monetary policy, government bond yields are also likely to tread rather different paths to the ones we had expected. The path may not be very dissimilar in the US, where we have been forecasting that the 10-year yield will end 2016 at 2.0%. But in the UK, it now seems unlikely that the 10-year yield will reach this level. (The two yields are currently around 1.5% and 1.1%, respectively.) It also seems less probable that the 10-year yield in Germany will edge up to our forecast of 0.25% from its level now of about -0.1%. In Japan, though, the vote has cemented our view that the yield is set to nudge lower, from nearly -0.2% currently to our forecast of -0.25%.

• As far as equities in developed markets are concerned, we doubt their weakness is a sign of things to come. Indeed, we are actually more upbeat about the prospects for those in Europe than in the US, given the stages of their economic cycles and the outlook for exchange rates. Even in the UK, a lower currency should cushion equities from some of the concerns about the consequences of a “Brexit”.

• We also anticipate that equities in emerging markets will recover in due course. This is partly due to the prospects for China’s economy, which are likely to come under fresh scrutiny. In our view, there is no sign of a forthcoming hard landing in China. Indeed, our view is that growth there is likely to rebound in response to looser policy. If so, most commodities should also benefit further in time.

All good then. Buy the dip? Not so fast!

Advertisement

This thinking is so shockingly short term that it represents a complete mis-pricing of what just happened. Credit Suisse has a better idea:

The UK has voted to leave the EU, by a narrow margin of 52-48, in what is the most significant pull back to-date from the post WWII consensus of closer integration and open trade.

While the actual path to exit is not yet clear, there are nonetheless profound implications for the UK. We expect a recession in the second half of the year and policy easing from the Bank of England. The domestic political turbulence may complicate the process of actually leaving the EU.

There are also significant implications for the EU. We expect the euro area economy to slow, with growing support for populist political parties of both left and right across Europe likely to raise the risk of further fragmentation of the Union.

For the rest of the world, the direct impact should be more muted, although there is a risk that financial turbulence has a real economy impact, with the market likely to begin to focus more acutely on the upcoming US election.

While this vote does not represent a systemic shock to the financial system on a par with Lehman or a Greek departure from the euro, it does represent a powerful turning point. The UK has taken a significant step back from globalization. That’s a trend gaining political support across the west. Such a significant secular shift has the potential to have substantial implications for growth, corporate profits and asset prices in the medium term.

Given the dramatic changes in asset prices overnight, the temptation for many may be to fade the moves. While we acknowledge the risk of a technical bounce back, we think the repricing in many markets has further to run:

FX Strategy: The dollar rally is likely to continue, with cable moving into the 120s, while dollar Yen could settle below 100. The only note of caution is the possibility of central bank intervention – possibly in a coordinated fashion.

Fixed income strategy: Benchmark yields are likely to rally further, with US 10-year yields threatening historical lows, while Germany and Japan will move further into uncharted negative territory. We also expect the UK rates market to eventually price for policy easing, with front-end curves inverting.

Equity Strategy: Our FTSE 100 year-end target falls to 6,200 from 6,600. We also take our S&P 500 year-end target to 2,000 from 2,150, and our Euro Stoxx 50 target to 2,950 from 3,350. We expect the FTSE 250 to underperform the FTSE 100 by 10% to 15%.

Credit Strategy: Our view is that the expected panic in credit markets will only last a day or two, and will provide an opportunity to buy at better levels.

EM Fixed Income: EM assets will be hit because they constitute risk assets and the leave vote will pull down commodity prices, which in turn help guide prices for many EM assets. However, we believe the negative risk market response to the referendum will be much smaller than the one that unfolded in the worst spell of the Eurozone crisis in 2011. We think EM spread-widening of 30% or less is likely.

Cenkos takes it further:

It’s not just Brexit; markets will now also have to price-in the probability that both Scotland and Northern Ireland will eventually vote to leave the UK. In macroeconomic terms, it is hard for us to see upside in this 3- 5 year scenario of interlinked breakups – the aggregated GDPs of separated England/Wales, Scotland and Northern Ireland are almost certainly going to be lower than that of the formerly United Kingdom, average household incomes will be correspondingly lower, and house prices as well. Yes, there is the opportunity for the politicians in each of these countries-to-be to restructure their economies to be more competitive – but there will be several years of logistical turmoil (eg currency separation, sovereign debt reallocation, establishing separate central banks) to contend with beforehand.

The closest historical analogy to this impending scenario is the breakup of Czechoslovakia in 1993-4. We were there; in terms of GDP, it took the Czech Republic 3-5 years to recover; it took Slovakia a decade. If memory serves, Slovakian politicians instigated the breakup, with a sovereignty pitch similar to that used by the Brexiteers. These same dynamics will apply to the possible breakup of the UK, we fear.

For the banks, obviously none of this is good news. Falling house prices will hurt Lloyds the most, whilst Scotland voting to leave the UK in a rehash of their referendum will hurt Lloyds and RBS particularly badly in terms of how much it will cost to separate their Scottish operations. In a Northern Ireland breakup, RBS will also have Ulster Bank to worry about.

Yep, and that’s not real risk. For that we turn to Nomura:

Advertisement

Do not underestimate the global contagion

At first glance, it would seem that the financial and economic impact of this result should be largely confined to the UK, given that its economic size is quite small at less than 4% of world GDP and world imports in 2015. However, we believe that this is too simplistic of a view and that the impact of the Brexit will be far reaching and long lasting, for two main reasons.

First, we expect non-trivial spillover to the euro area economy and financial markets.While the value of merchandise exports from the rest of the EU to the UK is only 3% of the rest of the EU’s GDP1, the UK’s position as a global financial hub – UK financial sector assets account for more than 8x its GDP – leaves the rest of the EU much more exposed to the UK in terms of financial and investment linkages, in part reflecting the UK’s relatively liberalised domestic market and its strong legal framework and institutions.

For example:

One-third of the UK’s financial and insurance services exports are to the EU

More than half of the UK banking sector’s cross-border lending is directed to the EU

Almost half of the foreign direct investment received by the UK comes from the EU2

In addition, Brexit could further inflame anti-EU sentiment in other EU member states, heightening fears of more countries opting to leave the union. It is largely due to these non-trade-related channels that we expect a reduction in euro area GDP growth by 0.5 percentage points (pp) and a weaker EUR/USD.3 While UK share of global GDP is less than 4%, the rest of EU’s share is 18%, so once second-round effects on Europe are taken into account, the global impact is no longer trivial.

Extreme uncertainty is an anathema to financial markets

This extreme uncertainty in the City of London, one of the world’s largest financial centres, is anathema to global financial markets, especially when the global economy is as fragile as it is and as there are limited monetary and fiscal policy easing buffers available to most of the world’s major economies.

At this early stage, great uncertainty exists over just what the Brexit will ultimately mean for the UK economy. For example, how soon and how successful will the UK be able to negotiate with the EU the terms of its withdrawal, and renegotiate trade relationships with 60 non-EU economies where trade is currently governed by EU relationships? Will there be constitutional havoc in amending legislation from EU law to UK law? Will Scotland push for another referendum on independence? Heighted uncertainty and risk aversion is likely to discourage new investment in the UK and weigh on consumer sentiment. The danger is that all these factors – rising inflation, falling asset prices, high uncertainty and weakening private domestic demand – reinforce each other in a downward spiral, dwarfing any positive impetus from a more competitive exchange rate or monetary and fiscal policy easing.

The psychological impact – a link to the US elections

Moreover, one should not underestimate the psychological impact and how quickly markets could link the outcome to a rising risk of Donald Trump winning the US presidential election. As Anatole Kaletsky warned in an article on Project Syndicate (see Brexit’s impact on the world economy, 17 June 2016), the UK referendum is part of a global phenomenon – the rise of nationalist sentiment and populist revolts against established political parties. The demographic profile of Brexit supporters is found to be strikingly similar to that of American Trump supporters. The opinion polls are also strikingly similar: The UK polls showed the Brexit and Bremain camps to be close to neck and neck going into the referendum, as are the US polls on the two main US presidential candidates, Trump and Hilary Clinton. In contrast, investors, judging from recent price action, did not anticipate a Brexit, and option pricing suggests markets are also discounting a Trump victory. The UK betting markets too have downplayed the results of opinion polls: the odds of Brexit were generally about 1-in-3, similar to what US betting markets assign to a Trump victory.

The surprise Brexit result should now increase the credibility of opinion polls – they had indicated a much closer race than the odds published by bookmakers – in gauging how people actually vote. Statistical theory even allows us to quantify how expectations about the US presidential election should shift following the Brexit wins in Britain. To quote Kaletsky, imagine “for the sake of simplicity, that we start by giving equal credibility to opinion polls showing Brexit and Trump with almost 50% support and expert opinions, which gave them only a 25% chance. Now suppose that Brexit wins. A statistical formula called Bayes’ theorem then shows that belief in opinion polls would increase from 50% to 67%, while the credibility of expert opinion would fall from 50% to 33%.” The upshot is that investors are likely to take the results of opinion polls more seriously now and, as such, financial markets could start pricing in a greater risk of a Trump victory in the 8 November election and, possibly, a greater chance of populist insurgencies in the rest of Europe.

The financial tail wagging the real economy dog

In a nutshell, we expect the global impact of the Brexit to be more through the financial, confidence and psychology channels than simply through trade. Our warning is to not underestimate the depth and reach of global financial market contagion, which seems to have increased since 2008. For instance, during the European crisis of 2011, when there were significant fears of EU breakup, Asia’s stock and bond markets became much more highly correlated to the Euro Stoxx 50 and the German government bond yield than over 2000-07 (Figures 1 and 2). And as Hyun Song Shin, economic advisor and head of research at the BIS, recently described it (see Global liquidity and procyclicality, 8 June 2016), “the real economy appears to dance to the tune of global financial developments rather than the other way around”, through wealth, confidence, loan collateral and liquidity effects.

Granted, one potential cushion to a global financial market selloff is expectations of a further delay in the next Fed rate hike, but markets have already significantly priced out Fed hikes for this year (following the Brexit outcome, the market is now pricing a mere 6% likelihood of a Fed rate hike in 2016, down from 58% prior to the EU referendum).

Our US team now believes that the most likely timing of the next Fed rate hike is December (see Policy Watch: Brexit vote will likely delay FOMC rate hike, 24 June 2016). Instead, we believe that the more dominating factor will be renewed concerns over global growth and a likely stronger USD – together they are likely to cause oil prices to continue falling, adding more fuel to the fire of a major risk-off event in emerging markets. A globally coordinated central bank response to a global financial market meltdown is quite likely, such as liquidity support through FX swap arrangements and possible FX intervention, but with policy credibility at such a low it is unclear how successful these emergency measures will ultimately be when there is extreme market risk aversion.

Yes, it is, but you can forget the Fed, its tightening is done which hints at the real problem that Brexit has just unleashed upon the world. Central banks are going to print again, because that’s what they do, but can they put back the secessionist genie now loose from the bottle? Can they turn off Europe’s refugee crisis? Can they undo Britain’s legitimisation of every anti-European movement across the Continent with all elections and referendums, indeed polls, now flash points for fragmentation? Can they prevent the rise of Donald Trump?

No, they can’t. They can print. And make all of these things worse by doing so via increased wealth disparities.

Advertisement

More to the point, nobody is now going to print like the European Central Bank. What investor in his right mind would want to hold euro now? Or euro denominated assets? There’s a rolling series of fragmentation shocks ahead, starting with France mid next year in an election in which the anti-euro National Front is already charging the polls. It’s possible that within a year that the euro will cease to be as one of its core two partners walks out. With that kind of risk embedded in the currency’s future, the euro is now a zombie-currency, worse, a zombie reserve currency, and the buyer of last resort for all euro-denominated debt, the ECB, is going to be very busy indeed.

So, that means chronic euro weakness.

The second central bank to print will be Japan, operating under the cover of the Brexit global shock. It’s business cycle is already failing and inflation falling. It needs moar and will deliver it. That should also equal a return to yen weakness, assuming they get their methods right.

That leaves the US Fed facing the unprecedented situation of a strong US dollar even as it backs off tightening. Europe’s zombie currency will permanently dent the Fed’s ability of deflate the US dollar. By how much who knows? Materially.

Advertisement

Thus, over the stretch, the commodity bear market just got structurally worse because the US dollar has been made structurally stronger. The Capital Economics misrepresentation of Chinese growth deserves a special mention here too. China is already in a hard landing. Its ebbs and flows of policy are about managing what is a swift glide slope to slower and less commodity-intensive growth. We’ve gone from 12% growth to 6.5% (and much lower in reality) in five years. The next slowing is already baked in for later this year as stimulus fades so before long commodity prices will confront the double whammy of falling demand and a strong US dollar.

That means more Chinese easing from the PBOC and further falls in the yuan as capital flight continues.

This is bad news for emerging markets, which will now see manufacturing exports to the developed world hit as raw materials exports to the developing world are hit, and the US dollar being structurally stronger means structurally weaker capital inflows as well. And this will happen while China devalues meaning EMs are also losing competitiveness.

Advertisement

The Brexit base case then is that the zombie-euro just turned the global business cycle into a zombie as well. Every rally in risk will hit a lid in every European opinion poll. Markets have nowhere to go upwards. Whether they price this in a panic now or more slowly is the only question in my mind. The initial reaction suggests that it will be chronic rather than acute and if so that is a blessing given it offers more chances to position for the bust. The speed of it will probably be determined by the degree of contagion into commodities and especially oil. The oil rebalancing will be delayed by slower growth now and, as I wrote last week, if some of the curtailed production in Nigeria or Libya were to suddenly reappear then the glut would return and the price crash below $40. Then we’d see a combined credit shock of jumping developed market interbank spreads and emerging market high yield. That has global bust written all over it as Brexit, the Mining GFC and quantitative failure all collide.

So a bust it is, whether it happens next week or next year.

For Australia and Australian investors, how will this play out? The zombie-euro is a double blow Downunder. As well as structurally shifting commodity prices lower, wholesale Australian bank funding costs have just shifted structurally higher as Anglo-European interbank markets take years to digest the rolling fragmentation shocks. Moreover, as the zombi-euro marches on and the UK enters a current account adjustment, I expect markets will reassess and reprice the risks of supporting current account deficit economic models in general in a de-globalising world.

Advertisement

Thus this morning I find the pricing of Aussie bonds hilarious. Hilariously bullish that is. The two year bond is now pricing 1.62%, it hasn’t even priced the next rate cut, let alone the following four or five. Does anyone think that Australian demand will be lifted by any of the above? That inflation will bounce back under any of the above? The RBA will cut until rates are at 1% and below so bonds are cheap. It’s the same right across the curve. At some point there is still a worrying risk of a reversal in bond yields owing to Australia entering its own current account crisis but we’re not here yet.

Gold is the next bullish candidate. Although a structurally stronger US dollar should be very bad for gold, the unprecedented circumstances of the zombie-euro will repeatedly raise fundamental questions about the efficacy of global fiat currencies. The only logical hedge to that is gold so I expect it to decouple from the strong US dollar.

The Australian dollar stood up well under the initial shock but that’s not going to last owing to all of the above. It’s going to fall and keep falling. MB’s 45 cents target by cycle end remains.

Advertisement

All equity market rallies are now sells with the exception of gold miners which remain a “buy the dips” play. Pressure on Australian bank equity will intensify.

Last but not least we come to Australian property. The two forces coming to bear upon it are extreme. On one hand we have massive over-inflation driven in part by population growth that authorities are determined to hold to. On the other hand we are entering an environment intrinsically hostile to the offshore funding model that supports those valuations. The tipping point may be that Brexit is going to strengthen anti-immigration movements everywhere including in Australia. We can’t secede from Asia of course but it is likely that the population ponzi will come under increasing political stress.

Australia is literally run by a property cabal these days that will do everything it can, anything, to support housing values but they are swiftly being outflanked by history and property, too, is a sell.

Advertisement

Don’t kid yourself, fast or slow, the next global shock is upon us.

Please note that these are asset allocations opinions not investment advice.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific's leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.