Australia versus chaos theory

According to Wikipaedia “chaos theory is a branch of mathematics that deals with complex systems whose behaviour is highly sensitive to slight changes in conditions, so that small alterations can give rise to strikingly great consequences”.

Australia exists in a state of blissful ignorance of this theory. How else to explain an economic model that relies upon the smooth running of just about every other economy on earth? Let me explain.

Back in 2009 when I co-wrote The Great Crash of 2008 with Professor Ross Garnaut, the book proved to be very influential in policy circles owing to one central observation. The book described the process through which the Australian economy had been transformed in the late nineties and millennium to a model highly vulnerable to external disruption:

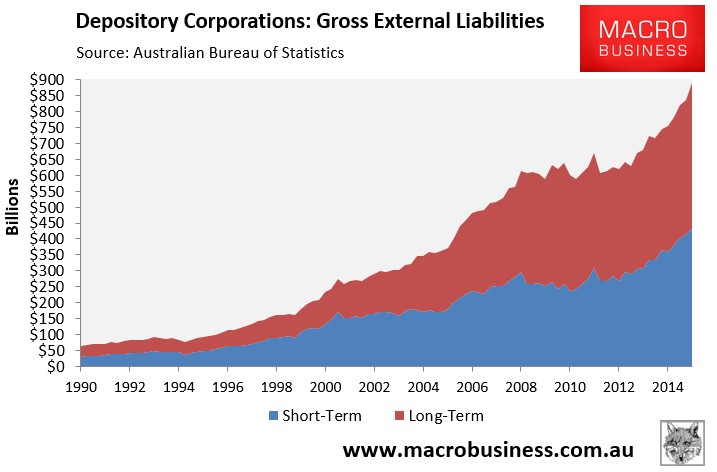

The growing asset boom and falling savings rates meant that ANZ, NAB, CBA and Westpac found that the demand for loans outstripped deposits. Australian banks’ ratio of deposits to total liabilities was 59 per cent in December 1994. By 2000 the ratio had dropped to 46 per cent. It finally hit 43 per cent in late 2007.30 Competition for loans with the new shadow bank sector was also intense, which gave rise to the big four’s own shadow banking activities. They were cautious about securitisation, but their high (AA) ratings provided them with a different method for accessing funds to lend: the issue of bonds directly to international investors.

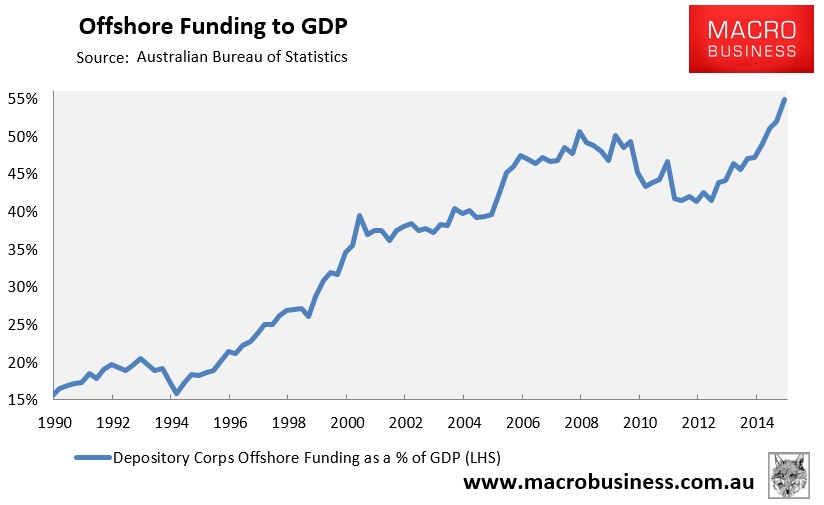

The banks’ foreign wholesale borrowings grew from A$30 billion in 1990 to A$100 billion in 2000. From there the borrowing escalated, reaching A$357 billion in 2008.31 The Australian housing and consumption boom of the early twenty-first century was funded by foreign borrowing by the banks on a scale far greater than had ever happened before.

Traditionally, banks had been cautious about this method of raising funds because it carried the added risks of managing currency and foreign interest-rate fluctuations. Consequently, according to Philip Bayley, former director of Capital Markets at Standard & Poor’s Australia, ‘there was a direct correlation between the big four’s steady mastery of currency and interest rate swap derivatives and the rise of their borrowing in international wholesale markets’. These shadow instruments grew even more rapidly than the underlying borrowing. In 1990, Australian bank books showed a combined total of A$1.57 trillion notional derivative exposure. By 2000, the notional figure had grown to A$3.59 trillion, and in 2007 shot above A$13 trillion

The policy fallout from the GFC and the book was an acknowledgement that Australia had, in effect, developed a fragile economic model, one overly exposed to the flapping of far flung butterfly wings. There were three policy implications to this, all of them openly acknowledged by Australia’s key economic managers at the time:

- Treasury recognised that in a world where major offshore financial centers could close overnight then its doctrine of allowing foreign borrowing to run riot because it was derived from the decisions of “mature adults”, creating huge current account deficits in the process, was high risk and required serious mitigation. What followed was the largest fiscal consolidation since WWII;

- the Reserve Bank of Australia deliberately raised interest rates to difficult levels for Australia’s east coast mortgage economies in 2010 driving historic levels of deposit growth and flat-lining offshore borrowing;

- the Australian Prudential Regulation Authority (APRA) pursued a policy of dollar-for-dollar deposit-in, loan-out for banks, ensuring deposit competition and a push outwards in the maturity profiles of offshore borrowing.

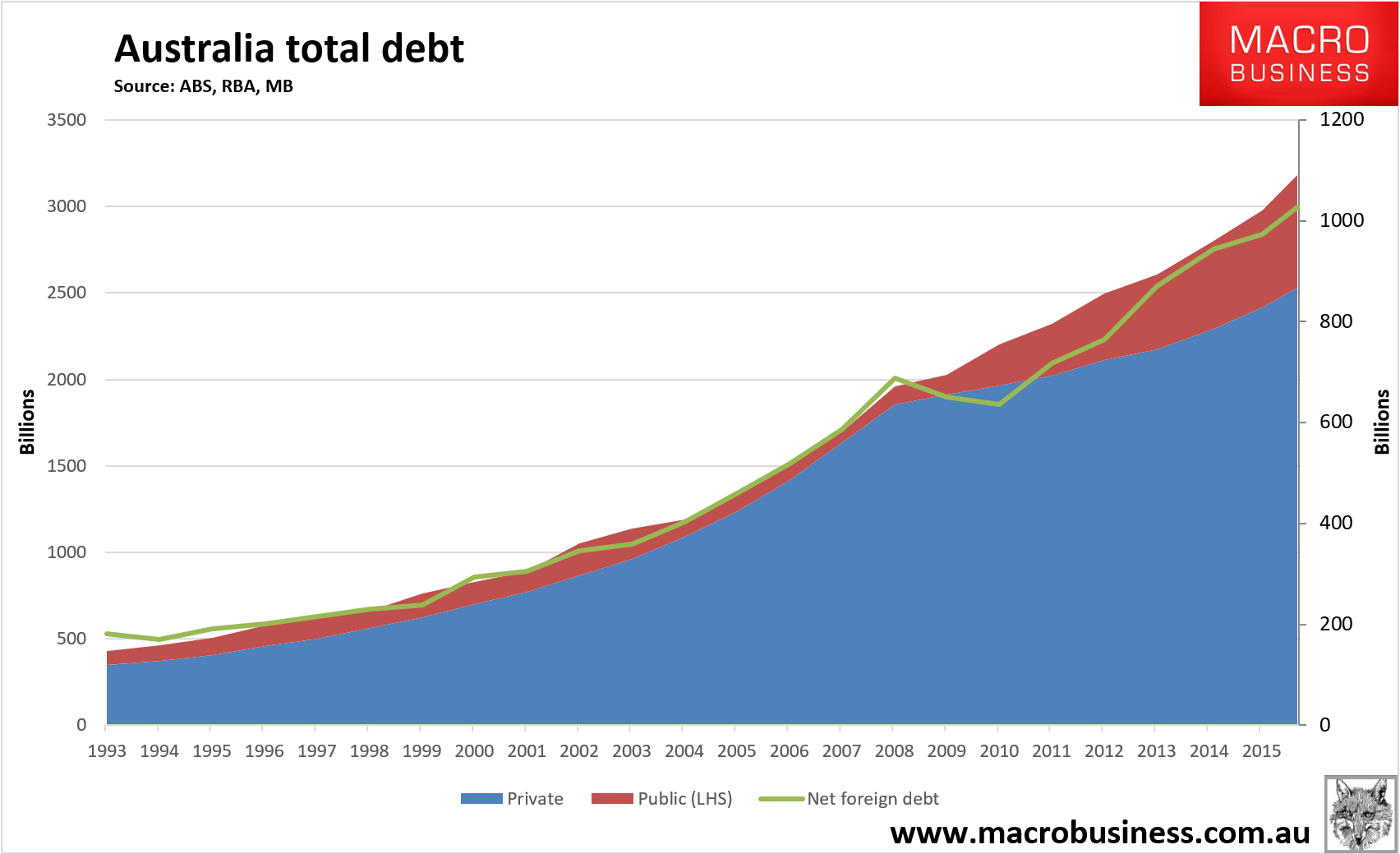

All of this was enabled by the serendipity of the commodities boom and was handled well if not as aggressively as it needed to be. The result was an historic four year buffering of Australia’s fragile economic model as offshore borrowing stalled and its ratios to growth fell, what MB described at the time as the Great Disleveraging from 2008-2012:

However, what appeared to be a structural change in thinking proved ephemeral. The same commodities boom that had allowed the lessons to be learned with little pain, in time fed into the old way of thinking, that Australia was exceptional, that its adults were somehow more wise and all-seeing than those of other countries and, as the commodities boom ended so did the repair work on Australia’s fragile economic model.

Indeed, one could be forgiven since for concluding that no lesson was learned at all as offshore borrowing screamed higher after 2011, its maturity profile radically shortened and fragility poured back into the economy, made all the worse by a dramatic deterioration in public finances, funded again from offshore:

In the past two years we’ve seen two more countervailing policy waves by folks in the system that still grasp this fragility. The first was the Murray Financial System Inquiry which ruled in favour of higher capital for banks and lower leverage ratios for mortgages in particular. It was incremental rather than step change but defined the “fragility” problem very clearly. Alas it was too late and not radical enough to prevent the post 2011 borrowing binge, nor could it prevent the public debt splurge now underway.

The next wave of policy innovation came with APRA finally moving to dampen the borrowing binge via macroprudential policies, something that the Murray Inquiry had unfortunately failed to endorse. We are seeing the excellent results of that today with mortgage growth rates tumbling as lending standards trending higher despite rate cuts and offshore borrowing slow sharply. However, there is more work to be done to prevent this debt from taking off again and, in reality, if it is pursued with appropriate vigour will probably prove to be pro-cyclical because it came too late.

It is at this last point that come back to today. Since the GFC, good people have done good things to stabilise the fragility built into the Australian economic but the structure of the system has still pushed it towards greater risk. Australia is only marginally less exposed to external disruption today compared with 2007. Non banks have been washed out and major banks are better capitalised, as well as having 60% deposit funding funding versus 50% back then but any serious freeze in global finance will still render the major banks insolvent in a ridiculously short period given they will be unable to roll over their liabilities. They’ll be able to lean on the RBA for nearly free liquidity but even so credit ratings agencies explicitly build in a two notch upgrade to bank ratings based upon an implicit public guarantee of the bank’s liabilities and as the Budget deteriorates so too does that guarantee.

So, we haven’t entirely wasted the previous cycle in terms of an anti-fragility policy agenda but we’ve done an awful lot less that we should have. And we are about to discover the efficacy of those efforts as first Brexit then a whole series of butterflies flap their wings across the globe. Anatole Kaletsky sums it up pretty well at Project Syndicate:

The febrile behavior of financial markets ahead of the United Kingdom’s referendum on June 23 on whether to remain in the European Union shows that the outcome will influence economic and political conditions around the world far more profoundly than Britain’s roughly 2.4% share of global GDP might suggest. There are three reasons for this outsize impact.

First, the “Brexit” referendum is part of a global phenomenon: populist revolts against established political parties, predominantly by older, poorer, or less-educated voters angry enough to tear down existing institutions and defy “establishment” politicians and economic experts. Indeed, the demographic profile of potential Brexit voters is strikingly similar to that of American supporters of Donald Trump and French adherents of the National Front.

Opinion polls indicate that British voters back the “Leave”campaign by a wide margin, 65% to 35%, if they did not complete high school, are over 60, or have “D, E” blue-collar occupations. By contrast, university graduates, voters under 40, and members of the “A, B” professional classes plan to vote “Remain” by similar margins of 60% to 40% and higher.

In Britain, the United States, and Germany, the populist rebellions are not only fueled by similar perceived grievances and nationalist sentiments, but also are occurring in similar economic conditions. All three countries have returned to more or less full employment, with unemployment rates of around 5%. But many of the jobs created pay low wages, and immigrants have recently displaced bankers as scapegoats for all social ills.

The degree of mistrust of business leaders, mainstream politicians, and expert economists is evident in the extent to which voters are ignoring their warnings not to endanger the gradual restoration of prosperity by upending the status quo. In Britain, after three months of debate about Brexit, only 37% of voters agree that Britain would be worse off economically if it left the EU – down from 38% a year ago.

In other words, all the voluminous reports – by the International Monetary Fund, the OECD, the World Bank, and the British government and the Bank of England – unanimously warning of significant losses from Brexit have been disregarded. Rather than trying to rebut the experts’ warnings with detailed analyses, Boris Johnson, the leader of the Leave campaign, has responded with bluster and rhetoric identical to Trump’s anti-politics: “Who is remotely apprehensive about leaving? Oh believe me, it will be fine.” In other words, the so-called experts were wrong in the past, and they are wrong now.

This kind of frontal attack on political elites has been surprisingly successful in Britain, judging by the latest Brexit polling. But only after the votes are counted will we know whether opinions expressed to pollsters predicted actual voting behavior.

This is the second reason why the Brexit result will echo around the world. The referendum will be the first big test of whether it is the experts and markets, or the opinion polls, that have been closer to the truth about the strength of the populist upsurge.

For now, political pundits and financial markets on both sides of the Atlantic assume, perhaps complacently, that what angry voters tell pollsters does not reflect how they will actually vote. Analysts and investors have consistently assigned low odds to insurgent victories: in late May, betting markets and computerized models put the probabilities of Trump’s election and of Brexit at only around 25%, despite the fact that opinion polls showed almost 50% support for both.

If Brexit wins on June 23, the low odds accorded by experts and financial markets to successful populist revolts in America and Europe will immediately look suspect, while the higher probabilities suggested by opinion polls will gain greater credibility. This is not because US voters will be influenced by Britain; of course they will not be. But, in addition to all the economic, demographic, and social similarities, opinion polling in the US and Britain now face very similar challenges and uncertainties, owing to the breakdown of traditional political allegiances and dominant two-party systems.

Statistical theory even allows us to quantify how expectations about the US presidential election should shift if Brexit wins in Britain. Suppose, for the sake of simplicity, that we start by giving equal credibility to opinion polls showing Brexit and Trump with almost 50% support and expert opinions, which gave them only a 25% chance. Now suppose that Brexit wins. A statistical formula called Bayes’ theorem then shows that belief in opinion polls would increase from 50% to 67%, while the credibility of expert opinion would fall from 50% to 33%.

This leads to the third, and most worrying, implication of the British vote. If Brexit wins in a country as stable and politically phlegmatic as Britain, financial markets and businesses around the world will be shaken out of their complacency about populist insurgencies in the rest of Europe and the US. These heightened market concerns will, in turn, change economic reality. As in 2008, financial markets will amplify economic anxiety, breeding more anti-establishment anger and fueling still-higher expectations of political revolt.

The threat of such contagion means a Brexit vote could be the catalyst for another global crisis. This time, however, the workers who lose their jobs, the pensioners who lose their savings, and the homeowners who are trapped in negative equity will not be able to blame “the bankers.” Those who vote for populist upheavals will have no one but themselves to blame when their revolutions go wrong.

Quite right, except for the last paragraph. We are only here because people blame the bankers and their policy buddies and even an elective unraveling of the system will make that worse not better. After all, the globalists built the system that folks want out of. If anything Kaletsky is, I think, underestimating the psychological shift against globalisation underway and there are a series of lightening rods ahead:

- taken at face value, a Trump Administration will be anti-China, pro-protection and nationalist with all kinds of economic struggle likely to turn hot across the Pacific;

- Fraxit looms as a real possibility in 2017 as National Front leads national polling which is the end of the euro as we know it;

- China’s debt mountain appears manageable until the Sixth Plenary of the Chinese Communist Party in mid-2017. After that, the reformist Xi Jinping should have complete control of the Politburo and be able to renew his economic transformation to much slower growth.

Chaos is coming in one form or many and Australia is not ready for it.