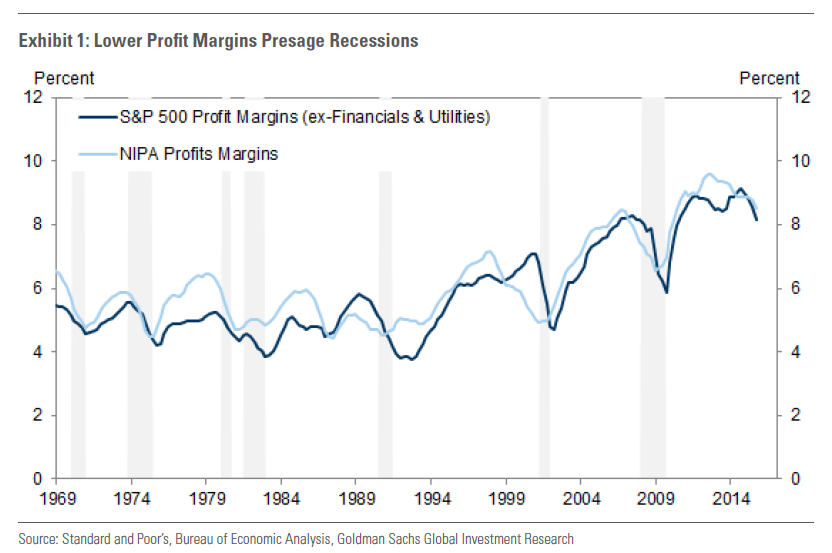

For a year or so MB has been warning that we’re entering dangerous territory for the global business cycle. This has been pretty obvious to those that have the eyes to see. US Fed tightening cycles nearly always ends in recessions and there is no reason to think that this one will be any different, from Goldman Sachs:

But no two business cycles are the same and this one is very different. Normally a business cycle dies of some combination of ponzi lending, inflation and higher interest rates. This time it’s dying of ponzi lending, deflation and lower interest rates, albeit with a little tightening at the end.

There are some more specific elements at work as well. As shockingly muted as it has been, the US tightening has unleashed a US dollar bull market. That, in turn, has exacerbated a commodity bear market emanating from slowing Chinese growth. That has had the knock on effect of hitting emerging markets twice over as domestic demand is hit by capital being repatriated to the US on a narrowing yield spread and external demand is hit by declining exports to China.

The full text of this article is available to MacroBusiness subscribers