It appears the Fed is over its case of the yips. From the minutes:

Participants discussed whether their current assessments of economic conditions and the medium-term outlook warranted increasing the target range for the federal funds rate at this meeting. Participants agreed that incoming indicators regarding labor market developments continued to be encouraging. They generally concurred that data releases during the intermeeting period on components of private domestic demand had been disappointing, but most participants judged that the slowdown in growth of domestic spending would be temporary, citing possible measurement problems and other transitory factors. Financial market conditions continued to improve, providing support to aggregate demand and suggesting that market participants saw some reduction in downside risks to the outlook: Equity prices rose further, credit spreads declined somewhat, and the dollar depreciated over the intermeeting period. Taking these developments into account, participants generally judged that the medium-term outlook for economic activity and the labor market had not changed appreciably since the previous meeting. Furthermore, most participants continued to expect that, with labor markets continuing to strengthen, the dollar no longer appreciating, and energy prices apparently having bottomed out, inflation would move up to the Committee’s 2 percent objective in the medium run.

Still, with 12-month PCE inflation continuing to run below the Committee’s 2 percent objective, a number of participants judged that it would be appropriate to proceed cautiously in removing policy accommodation. Some participants pointed to the risk that the recent weak data on domestic spending could reflect a loss of momentum in the economy that might hinder further gains in the labor market and raise the likelihood that inflation could fail to increase as expected. Accordingly, these participants believed that it would be important to evaluate whether incoming information was consistent with their expectation that economic growth would pick up and thus support continued improvement in the labor market. In addition, a number of participants judged that the risks to the outlook for inflation remained tilted to the downside in light of low readings on measures of inflation compensation and the fall over the past year in some survey measures of longer-term inflation expectations. Also, many participants noted that downside risks emanating from developments abroad, while reduced, still warranted close monitoring. For these reasons, participants generally saw maintaining the target range for the federal funds rate at 1/4 to 1/2 percent at this meeting and continuing to assess developments carefully as consistent with setting policy in a data-dependent manner and as leaving open the possibility of an increase in the federal funds rate at the June FOMC meeting.

Some participants saw limited costs to maintaining a patient posture at this meeting but noted the risks–including potential risks to financial stability–of waiting too long to resume the process of removing policy accommodation, especially given the lags with which monetary policy affects the economy. A couple of participants were concerned that further postponement of action to raise the federal funds rate might confuse the public about the economic considerations that influence the Committee’s policy decisions and potentially erode the Committee’s credibility.

A few participants judged it appropriate to increase the target range for the federal funds rate at this meeting, citing their assessments that downside risks associated with global economic and financial developments had diminished substantially since early this year, that labor market conditions were consistent with the Committee’s maximum-employment objective, and that inflation was likely to rise this year toward the Committee’s 2 percent objective. Two participants noted that several standard policy benchmarks, such as a number of interest rate rules and some measures of the equilibrium real interest rate, continued to imply values for the federal funds rate well above the current target range. Such large and persistent deviations of the federal funds rate from these benchmarks, in their view, posed a risk that the removal of policy accommodation was proceeding too slowly and that the Committee might, in the future, find it necessary to raise the federal funds rate quickly to combat inflation pressures, potentially unduly disrupting economic or financial activity. Overly accommodative policy could also induce imprudent risk-taking in financial markets, posing additional risks to achieving the Committee’s goals in the future.

Participants agreed that their ongoing assessments of the data and other incoming information, as well as the implications for the outlook, would determine the timing and pace of future adjustments to the stance of monetary policy. Most participants judged that if incoming data were consistent with economic growth picking up in the second quarter, labor market conditions continuing to strengthen, and inflation making progress toward the Committee’s 2 percent objective, then it likely would be appropriate for the Committee to increase the target range for the federal funds rate in June. Participants expressed a range of views about the likelihood that incoming information would make it appropriate to adjust the stance of policy at the time of the next meeting. Several participants were concerned that the incoming information might not provide sufficiently clear signals to determine by mid-June whether an increase in the target range for the federal funds rate would be warranted. Some participants expressed more confidence that incoming data would prove broadly consistent with economic conditions that would make an increase in the target range in June appropriate. Some participants were concerned that market participants may not have properly assessed the likelihood of an increase in the target range at the June meeting, and they emphasized the importance of communicating clearly over the intermeeting period how the Committee intends to respond to economic and financial developments.

The Mining GFC just roared back to life. The dollar took off:

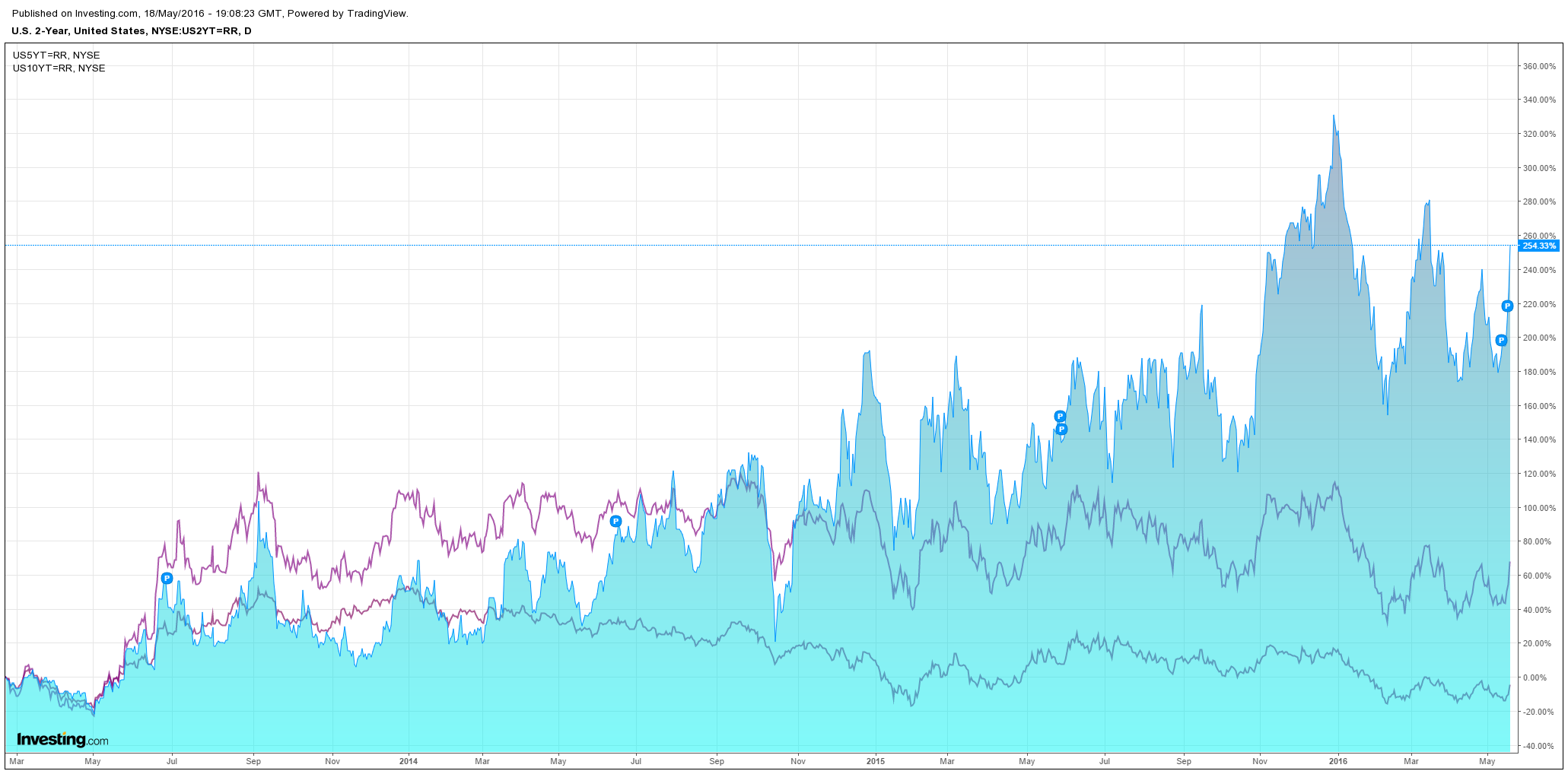

As bond yields soared:

Euro and yen slumped:

Commodity currencies were savaged:

Gold was smacked:

Oil was whacked:

Base metals are in trouble:

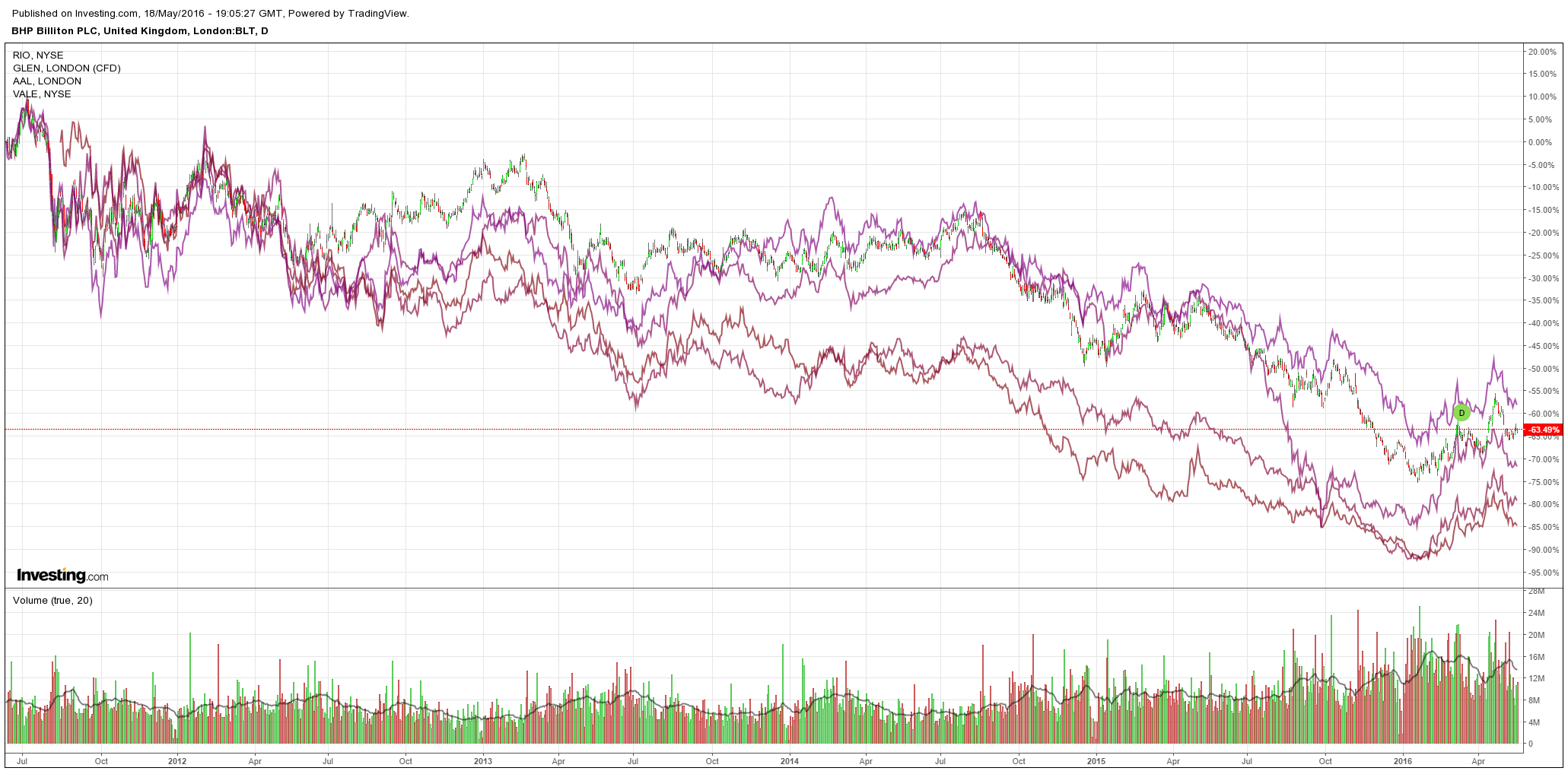

Big miners sank:

High yield fell but not as much as it should have:

Bloomberg’s Mark Cudmore is onto it:

The risk-aversion sparked by China in January is on course for an imminent replay unless the trend of the weakening yuan amid a strengthening dollar is checked.

Chinese data this weekend missed expectations across the board. But that isn’t the real concern — retail sales expanding at 10.1% year-on-year is still an exceptional pace of growth even if it’s a slowdown relative to the rate of the last decade. The real problem is the creep higher in USD/CNY.

It’s an expectations game. The more the currency pair climbs, the more traders fear that unsustainable capital outflows will force a more sudden yuan devaluation and result in global turmoil. Panic started in January when the rate climbed above 6.56 yuan. Today’s fix was within 0.4% of that level.

On Friday, the offshore yuan traded at the weakest level relative to the onshore yuan in more than three months. That’s a good barometer of building speculation.

The critical issue now is that the U.S. dollar is appreciating again. The Bloomberg Dollar index is up 2.8% in the last two weeks and another 2% wouldn’t be an unreasonable consolidation in the context of it dropping more than 7% in the previous three months.

That previous dollar slide distracted from the fact that yuan depreciation never abated. Against the basket, it’s been weakening at an average rate of almost 1.2% per month for the last five months.

The market’s single-minded focus on USD/CNY is crucial and it’s also why disaster can still be averted. It will require the PBOC to temporarily suspend their yuan-weakening policy for as long as the dollar is climbing.

Otherwise, prepare to batten down the hatches for the coming storm.

I’m not sure we’re quite there yet. We’ll need Chinese data to begin weakening again more substantially but the basic thrust is right.

The Mining GFC is back.