The Mining GFC was a mixed bag last night as the US dollar firmed:

Euro and yen fell:

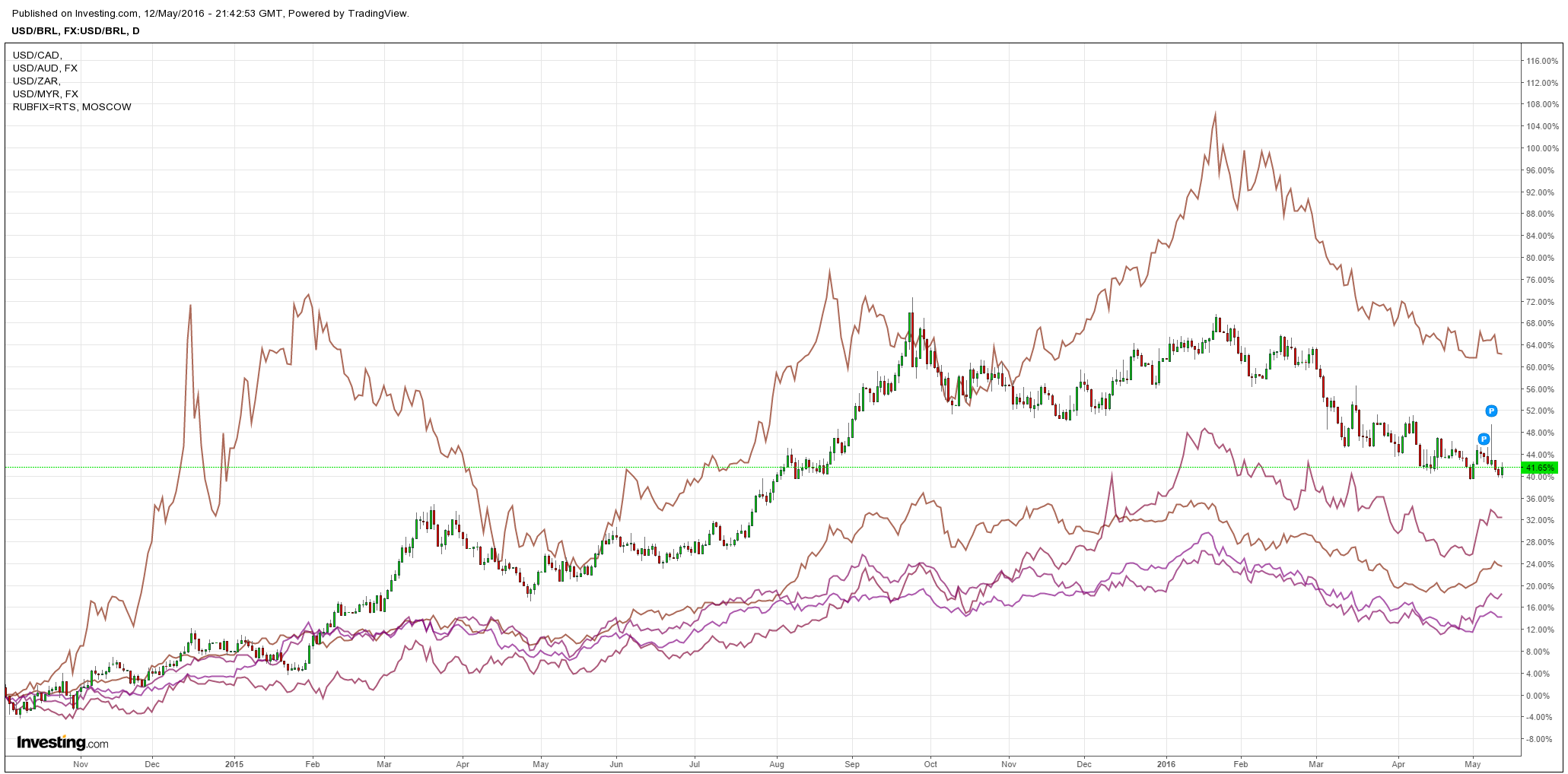

Commodity currencies were mostly firm on oil but not the iron ore exposed:

Brent is threatening to break out or double top:

Base metals were weak:

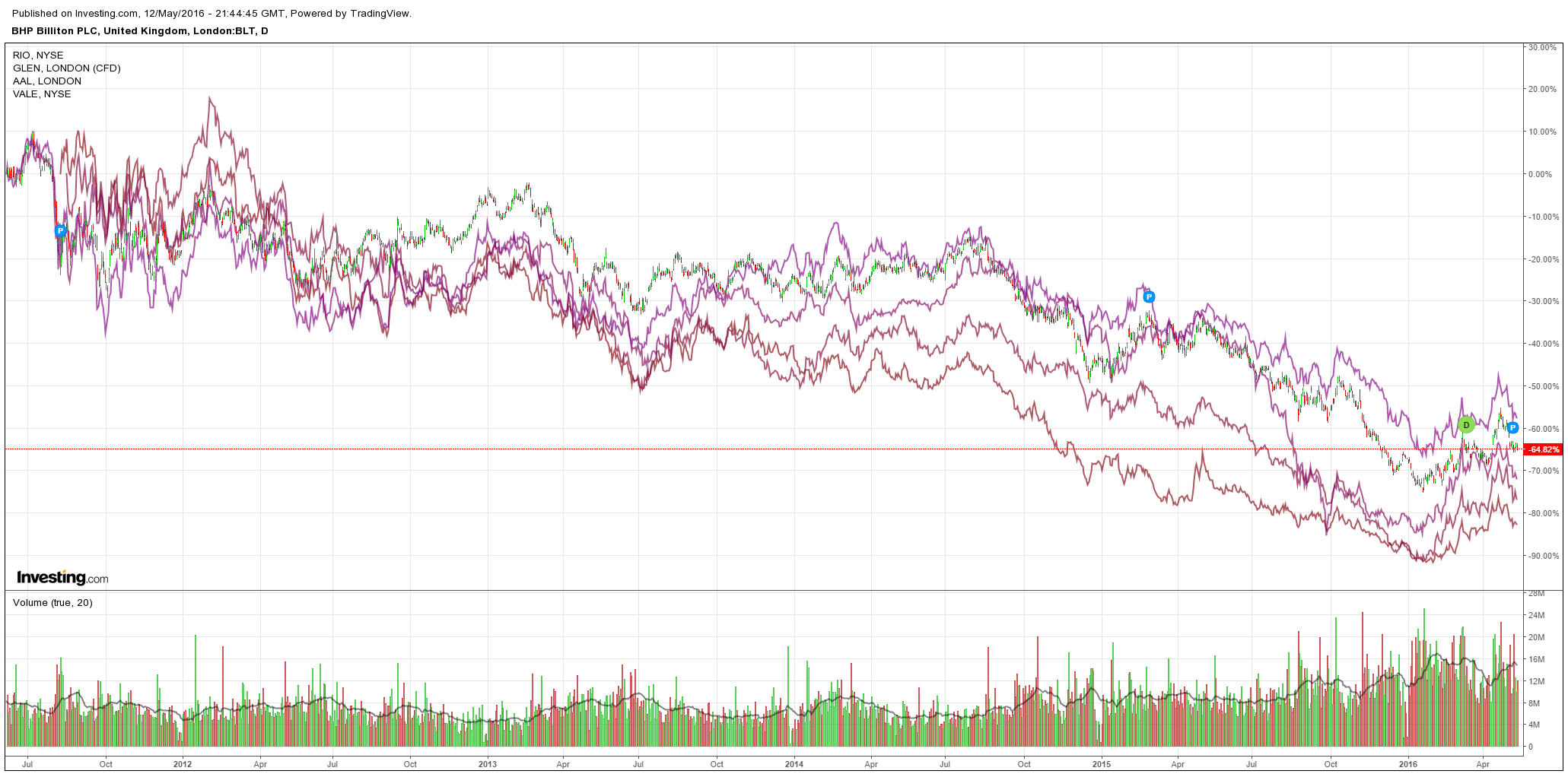

Miners hammered:

And EM high yield is diverging from US for now as the former follows oil but the latter is stalled as shale shakes out:

So, where are we? A note from the Horseman Global hedge fund is very interesting:

Your fund fell 4.29% net last month.

To lose 4.29% last month was a bit of a surprise to me, as most of the technical indicators I use indicated that the short squeeze was largely over at the end of March, and yet it continued into April.

The question to be answered after a drawdown is always the same, “Has something changed?”. In this case, I think something has changed. The overwhelming theme of the market for the past 18 months or so has been that of a strong dollar. European and Japanese markets had performed well as their currencies weakened versus the dollar, and commodity prices were generally weaker. Furthermore the strong dollar put pressure on the renminbi and encouraged thoughts of a Chinese financial crisis.

I was aware of the consensus in the market and put hedges in place to offset a weak dollar. I have had since last year long euro and long yen positions in the currency book, while having short Japanese and European exporters in the short book since last year. These hedges have performed very well, and have been the main reason that despite the drawdown, the fund has managed to hold on to most of the gains from last year.

The message that I am getting from the market, the “something” that has changed is that the US dollar is no longer a strong currency. Typically the US dollar falls when its economic cycle begins to roll over. Many of the indicators that I look at show the US is either in or heading for recession. These indicators include; the US trade deficit ex petroleum products which is back to 2006 levels; US capacity utilisation peaking in late 2014 and declining rapidly ever since; and US high yield have generally been widening since 2014.

Historically, a weak US dollar is good for commodity prices, and it is also good for emerging markets. This has played out this year, where we have suffered pain on emerging markets and commodity shorts, but have gained on Japanese and European shorts. Given that the US dollar could potentially fall significantly from here, it seems to me that we should take what have been hedges to our portfolio (that is long euro and yen, short Japanese and European equities), and make this the core of the portfolio, while our emerging market and commodity related shorts should become the hedges.

Having realised this late in the month, we have already made substantial progress to making this change in the portfolio. We have increased our long euro position to 50% of the fund, and long yen to 30% of the fund. We have closed a number of emerging market financial shorts, and opened European financial shorts. We are now net short European financials. We have closed a number of US listed oil shorts and replaced them with shorted euro denominated oil stocks.

It is possible that the US dollar could be so weak, that the US equity bull markets can continue, but it would probably lead to depression and crisis in Europe and Japan. At the beginning of the year, an investor asked me to sum up current central bank policy. I described it as a circular firing squad, where at best perhaps one economy could escape, but most likely everyone dies. The gun that they hold is competitive devaluation. We know now who is most likely to live and who is most likely to die, and are making the appropriate changes.

That smells like a bit of panic to me. The US dollar is not going to get far to the downside while other central banks are out-easing it and the odds still favour one more rate hike from the Fed.

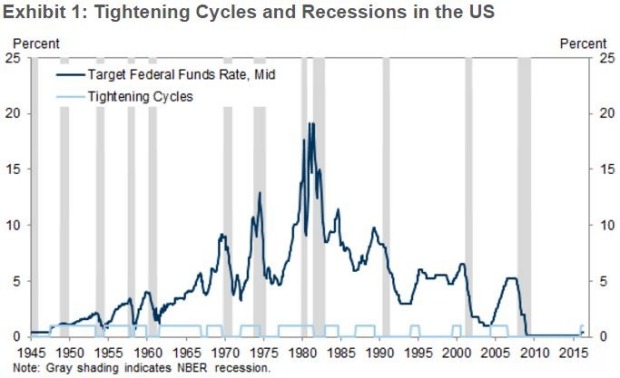

As I’ve said many times, the Mining GFC will not end until the Fed embarks on QE4. We’re not there yet and we have to consider what happens before we are. This chart from Goldman offers a clue:

Nearly every post-war Fed tightening cycle has resulted in a US recession. If that ball starts rolling again as the Fed tightens then there may still be a flood of money into the US dollar as things fall apart.

Regardless, these musing point to one pretty simple idea. When the shock does ultimately come, it will be followed by QE4, and that will put a rocket under one commodity above all others. This one:

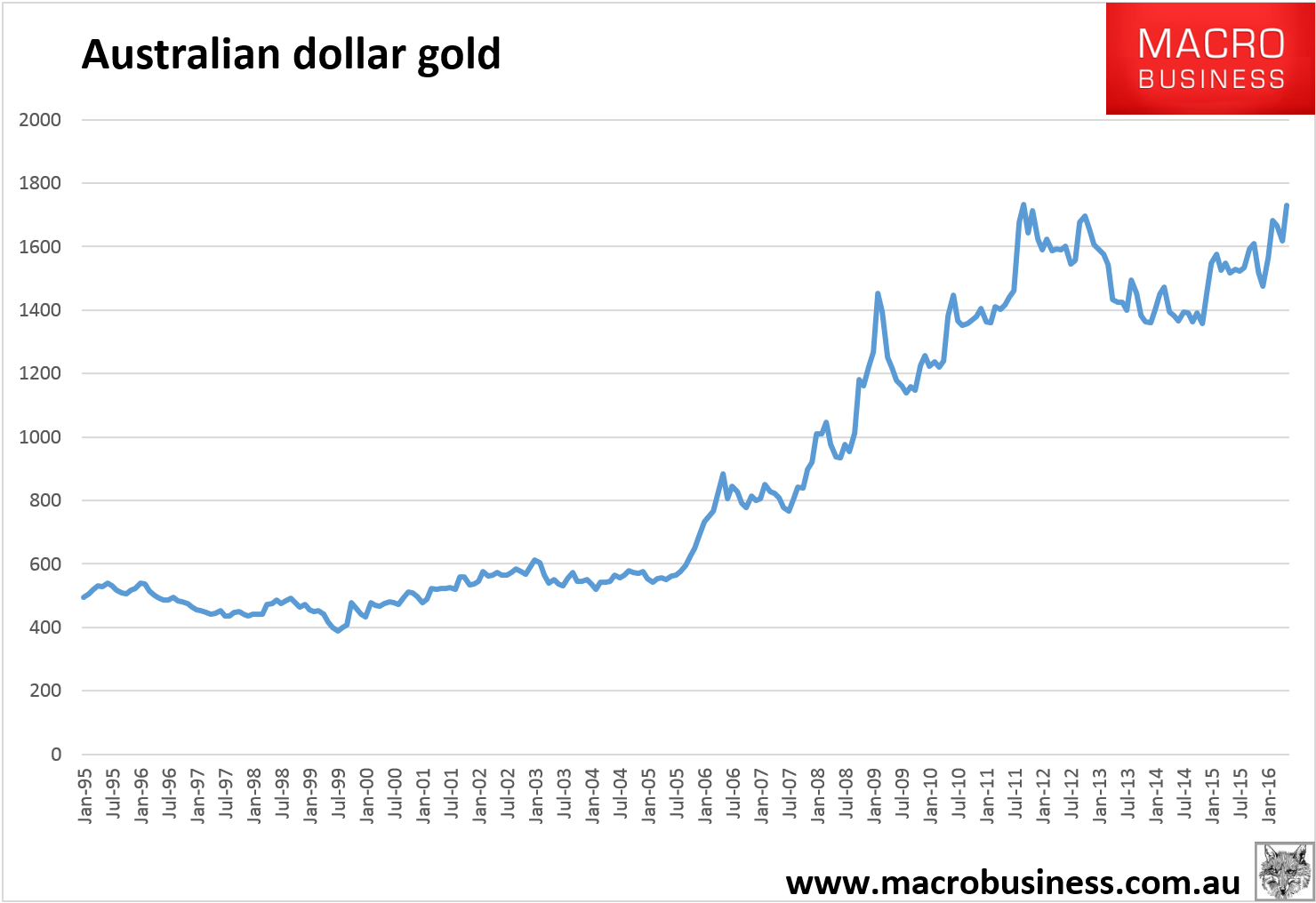

Gold. And for Aussies, it’s even better with gold in Australian dollars just hitting a new all-time high on the monthly chart:

There is a strong risk that gold will fall into the next global shock owing to short term US dollar strength as it did in 2008 depending upon how long the Fed takes to print again. As I’ve said before, that could be a good entry point for gold.

But the Aussie dollar is going to outpace gold to the downside anyway so the case to pick up at least some gold exposure now is strengthening. It is also a partial hedge for any long position Australians have in the US dollar without disrupting the trade. The Fed might move earlier than I expect and if so gold will fly more than the Aussie as the latter is weighed down by global growth and broader China-exposed commodities.

As a former gold trader, I mostly used mining equities as my preferred vehicle, obviously those with Australian costs and no hedges are preferable.