The US dollar eased back last night after it’s solid run:

Yen and euro rebounded:

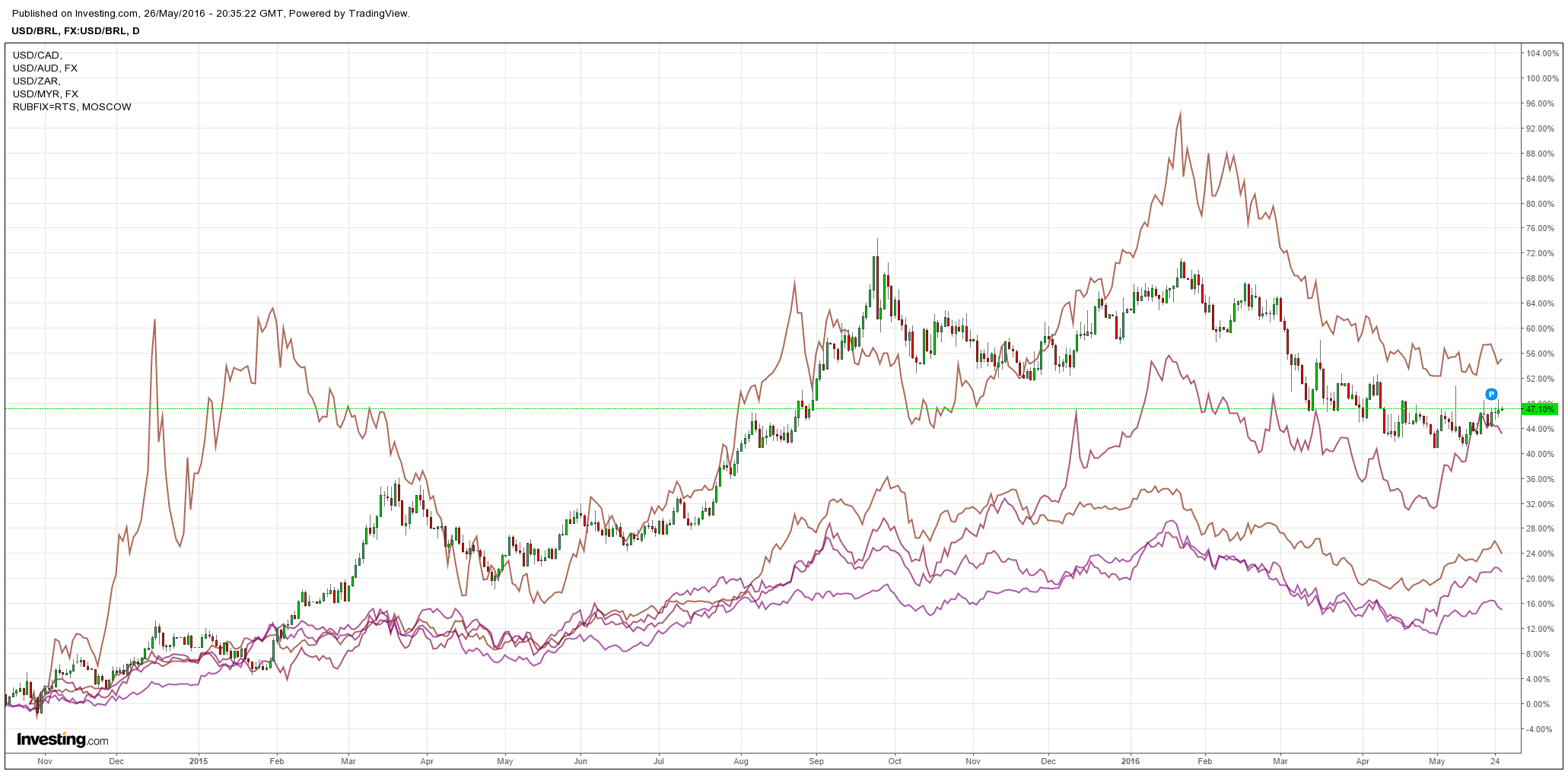

Commodity currencies too:

Advertisement

The US dollar eased back last night after it’s solid run:

Yen and euro rebounded:

Commodity currencies too:

The full text of this article is available to MacroBusiness subscribers