As Janet Yellen hawked up a bit and US data was solid, the US dollar rocketed Friday night:

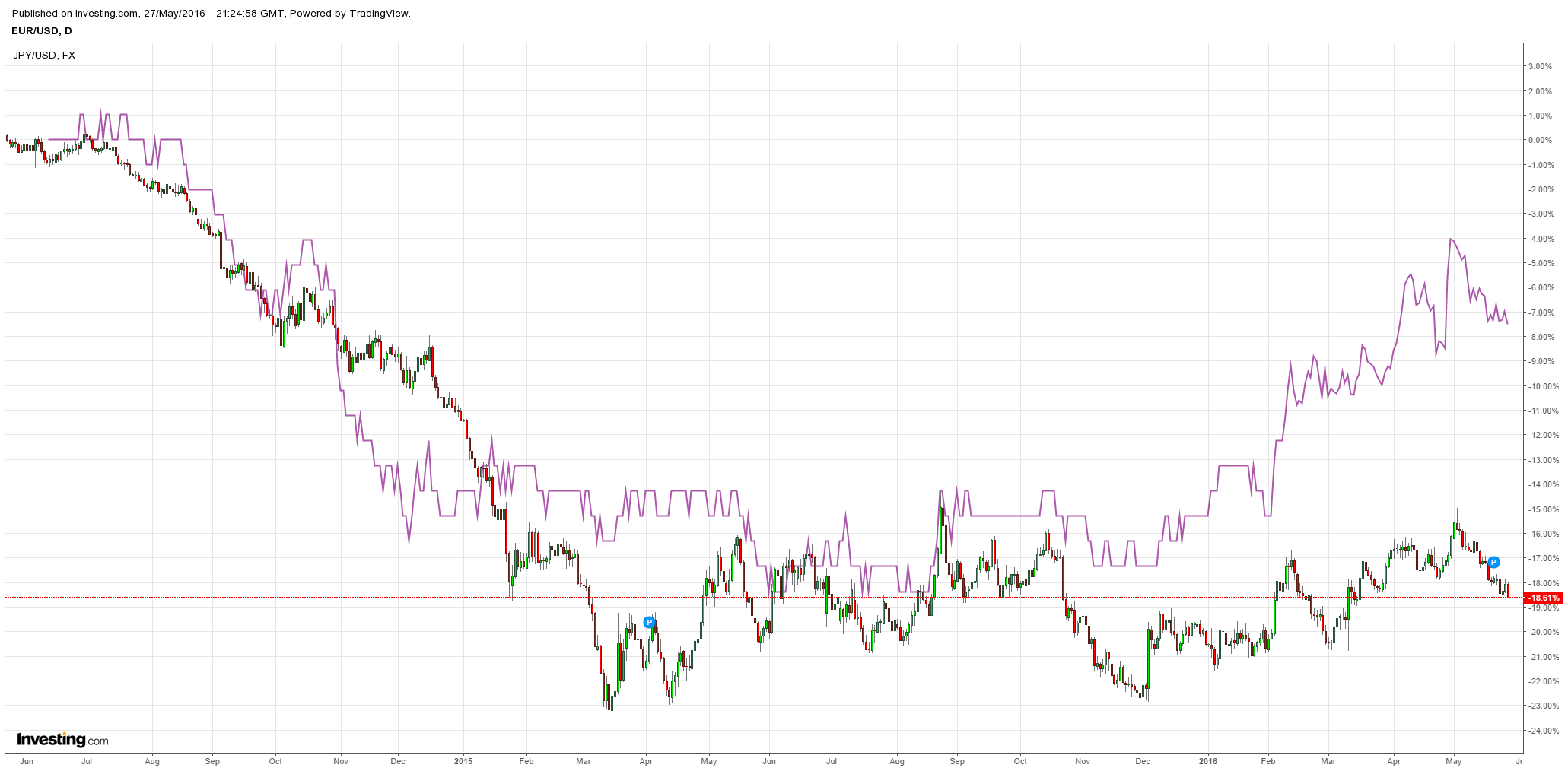

Yen and euro hit new lows:

Gold was pole-axed and if the US dollar really gets going then I’d be a buyer as it falls:

Advertisement

As Janet Yellen hawked up a bit and US data was solid, the US dollar rocketed Friday night:

Yen and euro hit new lows:

Gold was pole-axed and if the US dollar really gets going then I’d be a buyer as it falls:

The full text of this article is available to MacroBusiness subscribers