The Mining GFC firmed again Friday night as the US dollar was strong:

Euro and yen were conversely weak:

Commodity currencies were mixed with a weakish Aussie:

Advertisement

Oil was flat:

Base metals were weak:

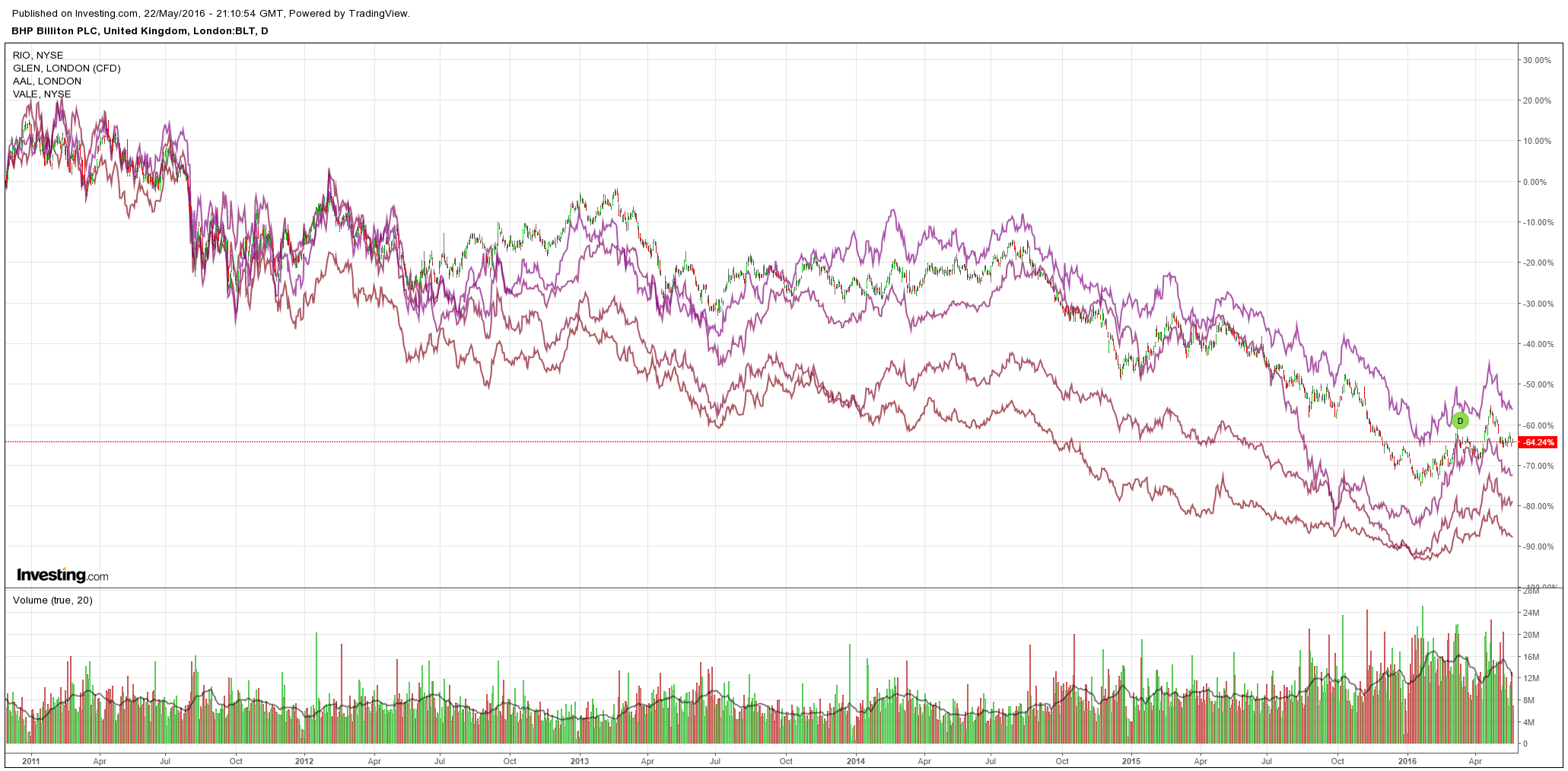

Big miners were flat:

Advertisement

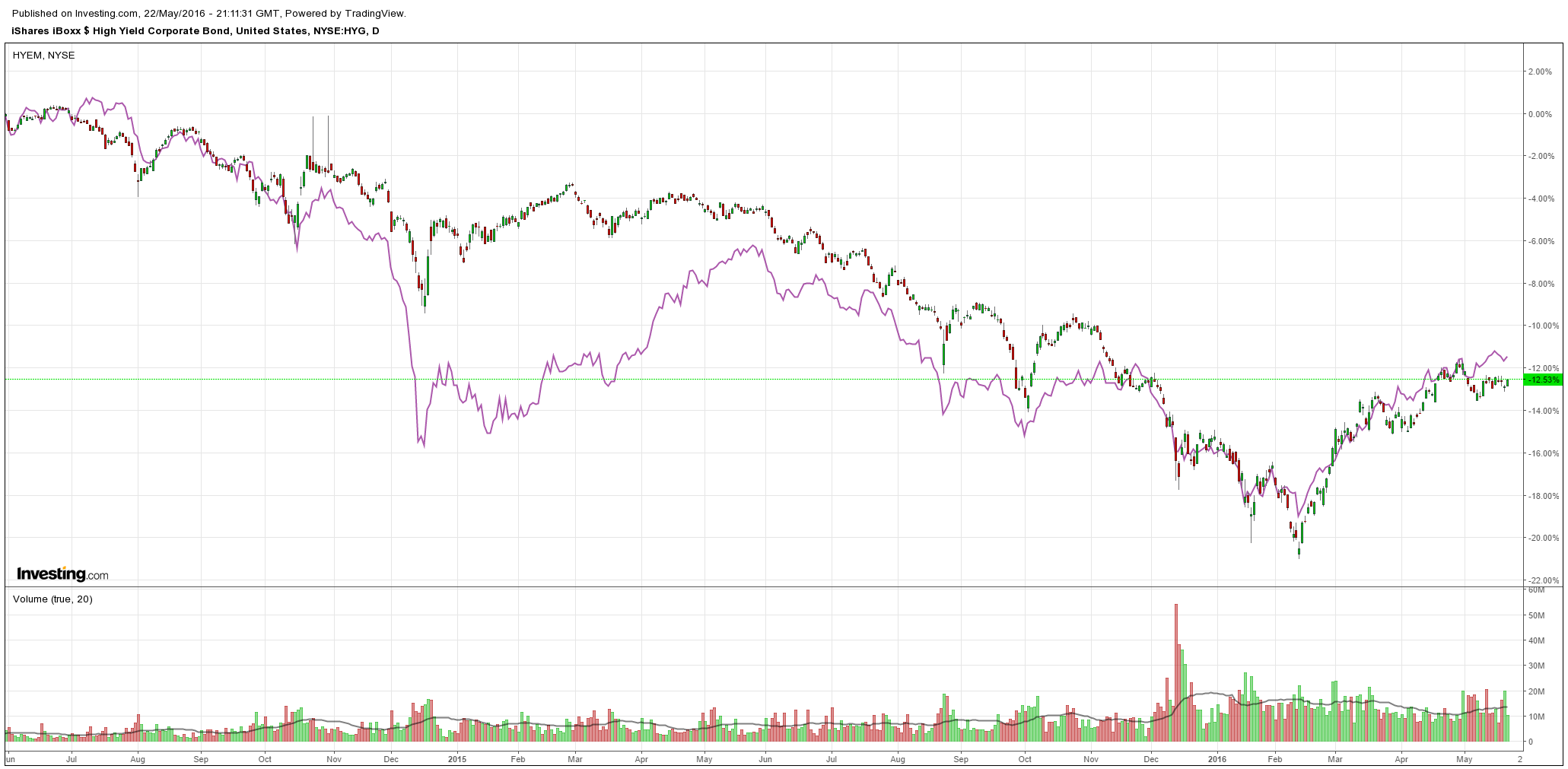

High yield too:

However, two stories today give a good read on why we are approaching Mining GFC 2.0. The is by David Uren:

The calm that has settled over world financial markets since the Chinese-induced turmoil early this year is at risk amid speculation that global inflation might at last be lifting, taking US interest rates with it.

JPMorgan forecast last week that global inflation would lift from 1.7 per cent now to 3 per cent by the end of the year on the strength of rising commodity prices. It says inflation is running at an annualised 4.5 per cent rate in the June quarter.

These forecasts came as US inflation figures were released showing a 0.4 per cent lift in prices in April, the largest monthly jump in three years. Although the annual rate is still a lowly 1.1 per cent, it has risen sharply from 0.7 per cent at the beginning of the year.

The April inflation report, along with the strong messaging from the US Federal Reserve that an increase in its benchmark cash rate was possible at next month’s meeting, have challenged the prevailing market sentiment that expected continuing stagnation to be the dominant theme in the global economy at least until late this year.

Advertisement

One should not overreact to this. Commodity inflation is temporary these days because it does not pass through to wages. As such it also hurts consumption. So, the Fed will “look through” the inflation not suddenly begin jacking up rates.

That said, it will prompt it to raise rates sooner rather than later so we’ll get our second hike before long.

But it’s false signal in my book and story number two tell us why, from Morgan Stanley:

Advertisement

It’s remarkable that in this day and age, when we can encode whole genomes and land spacecraft on comets, we struggle to answer basic questions on how big economies are doing. Although I’m going to focus on China, my fellow Americans shouldn’t be smug: The US enjoys some of the best economic statistics in the world and yet the market seems legitimately confused over whether the US economy is ‘weak’, ‘fine’, or actually starting to see a cyclical pick-up.

But in a contest for size and economic question marks, China may hold the crown. The speed and scale of the country’s growth has been remarkable, making China an essential part of the global economic fabric. The country consumes 45% of the world’s copper, produces 50% of the world’s steel, and is responsible for roughly 12% of global trade. Yet this importance is coupled with a level of uncertainty. Most investors that we meet believe China is extremely important to their outlook, and yet express a low degree of confidence in their ability to predict where it is headed next.

This dilemma is particularly relevant today. In response to slowing economic growth, China eased policy aggressively in the early part of last year. Interest rates were lowered. Fiscal spending picked up. Restrictions in the property market were eased. These steps, with a lag, have resulted in a strengthening of economic numbers since 3Q15. The question is how long this strength lasts, and how far ahead of that “turn” markets will react.

While the good news is that policy easing helped to stabilize growth, the bad news is that Chetan Ahya, our Chief Asia Economist, views this pick-up as temporary, and recently flagged greater risks that the slowdown arrives even sooner than August.

First, China is no longer doing the spending or easing that was in the pipeline six months ago.

Second, the current pick-up also appears associated with an even larger increase in net borrowing.

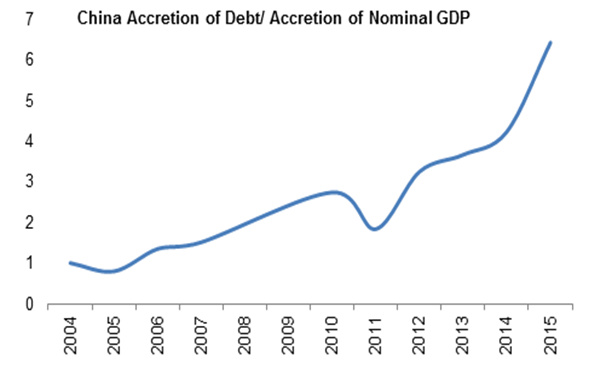

With it now taking 6.5 units of debt to produce 1 unit of GDP, additional gains from the lending channel are limited, in our view. China data already suggest diminishing returns from a flagging stimulus. Our China economic activity indicator (MS-CHEX) is at 3% versus 10% last month, while property sales in top cities have slowed to 15%Y in the first two weeks of May compared to 55%Y in April. If we think China growth softens again over the summer, the question for markets is how far ahead of this prices react. The risks are rising that the time is now.

The Fed’s attempt to inject more risk premium into the front end comes at a most vulnerable moment for EM, boosting the dollar and further limiting prospects of a fragile EM recovery. Fed futures price a full hike through December now, but the risk premium out the curve in the 2yr-5yr sector is still low. Yellen’s two speeches on May 27 and June 6 ahead of the June FOMC become critical in shaping that risk premium. A reiteration of the hawkish minutes will likely lead to front-end steepening and push USD higher and the commodity/EM universe onto the back foot. This is why our US rates strategist Matt Hornbach sees 2s5s steepeners as a good risk hedge.

Against this backdrop it is no surprise that across our research team, we are pessimistic about assets tied to the commodity/EM complex. Our EM & Asia equity strategist, Jonathan Garner, believes that investors should fade the rebound in EM and ‘Old China’ equities. Our EM fixed income strategy team has just gone underweight local rates and sovereign credit, in addition to already being bearish on EMFX. In commodities, our metals team is cautious about prices for 2H (which would also fit standard seasonal patterns) while our energy team believes that fundamentals remain much weaker than oil prices currently suggest. Our European equity strategist, Graham Secker, has turned to the safety of defensives, moving overweight last week. And for US equities, my colleague Adam Parker is increasingly convinced that the rally in low-quality names may be coming to an end, a dynamic that would help our preference for US financials over energy.

Finally, historical seasonal patterns suggest that May-November features a wider range of returns, with a more negative skew and higher vol of vol for many assets. That is yet another reason, if you needed one, to make this a summer you own some volatility into.

Yep. It appears to me that the Fed is set to hike right into China’s H2 weakening and as know that will:

keep the US dollar firm;

force yuan devaluation upon China, and

kill emerging market business models as commodity prices sink, China output gets more competitive and US dollar sourced debt tightens.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.