Mining GFC correlations are beginning to break. US dollar was weak last night and definitely looks to be retesting its trading range lows:

The yen continued its ramp and euro is threatening:

Commodity currencies roared:

Advertisement

Brent oil hit new highs in its rebound largely on US dollar weakness:

But base metals yawned:

Advertisement

Miners jumped anyway, mostly owing to iron ore:

And US and EM high yield debt rallied a little but not as we’d expect with the big oil jump:

Advertisement

So, where are we now? The key appears to be that stocks also fell and bonds were bid which is a complete reversal of the Mining GFC bear market rally pattern of everything riding oil. JPM may have an answer:

Big picture, one of our key medium-term concerns for equities remains the outlook for US profit margins. We have argued since late ’14 that corporate profit margins appear to be peaking out for this cycle. The latest NIPA data are confirming the deceleration, with our model pointing to much more downside. Weakness is broad-based, with margin compression seen in all subcategories of profits: domestic, foreign, financial and non-financial.

We think this deceleration will continue as productivity remains depressed and the top line is unlikely to accelerate. Profit margins are a particularly useful indicator to assess the stage of the business cycle. In the past 60 years, there has never been a recession starting before the peak in profit margins. However, once margins have peaked, the likelihood of a downturn increases materially.

We believe that the rollover in profit margins will be a constraint for equities, as profits have tended to drive most economic variables, capex and employment in particular. It will also likely have negative implications for corporate activity, especially as M&A, buybacks and dividends are at cycle highs, and US financing conditions are deteriorating.

We believe that the rollover in profit margins will be a constraint for equities, as profits have tended to drive most economic variables, capex and employment in particular. It will also likely have negative implications for corporate activity, especially as M&A, buybacks and dividends are at cycle highs, and US financing conditions are deteriorating.

The US profits outlook is also in a bind with oil. So far equities have benefited from the rebound with the expectations of higher inflation but as oil climbs, yet US shale does not rebound materially, then that tailwind is fast turning margin headwind with no offsetting growth dividend for oil production and investment.

Advertisement

This cannot go on for the US, for Japan or Europe. There will need to be moar stimulus. And HSBC again looks at what’s next:

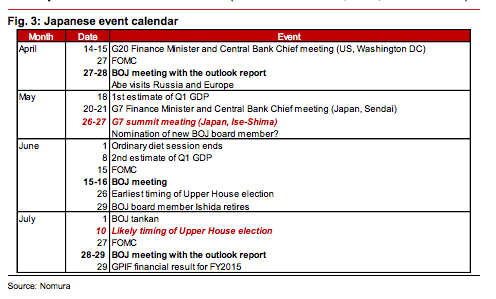

…at this point, the bigger problem for the Bank of Japan may well be the impact of a stronger yen on inflation. Already struggling to reach its 2 percent target by the end of the year, the goal is rapidly moving further out of reach. While inflation excluding fresh food and energy, a core measure, was close to 1% in February, it risks easing again over the coming months amid lackluster demand and lower import costs. Perhaps most worrying for monetary officials, corporate inflation expectations, as measured by the latest Tankan survey, has declined sharply, with companies forecasting inflation well below the BoJ’s target over the next 1, 3 and even 5 years.

What, then, to do? An expansion of the bond purchase program appears unlikely. The central bank runs the risk of running out of JGBs to buy – a former deputy governor of the BoJ last week suggested that at the current pace there wouldn’t enough bonds to purchase by mid-2017. Tightening market liquidity suggests that that point may be even closer.

A further push into negative interest rates also seems less likely – even though BoJ officials maintain that there is still plenty of scope to lower interest rates. But their effectiveness in spurring growth and lifting inflation expectations are questionable. So far, the adoption of negative interest rate policy (NIRP) seems to have had the opposite effects from those intended: the currency is up sharply, the equity market is down, inflation expectations have declined, and consumer confidence has slid. Of course, a lower yield curve, and falling bank lending costs, may over time prove stimulative, but the early verdict is not encouraging.

Something else is thus needed, another bazooka to revive confidence that the BoJ’s inflation target will eventually be met. HSBC’s Japan economist, Izumi Devalier, therefore argues that the central bank may shortly unveil an ambitious equity buying program, raising its annual purchases from 3 to 13 trillion yen. Such a move would be unprecedented outside the short-lived equity market interventions seen in other economies to support share prices (like the HKMA did during the Asian Financial Crisis). It would amount to an extraordinary expansion of the BoJ’s — or any central bank’s — toolset.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific's leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.