A little heat returned to the Mining GFC last night as a firming US dollar spooked markets:

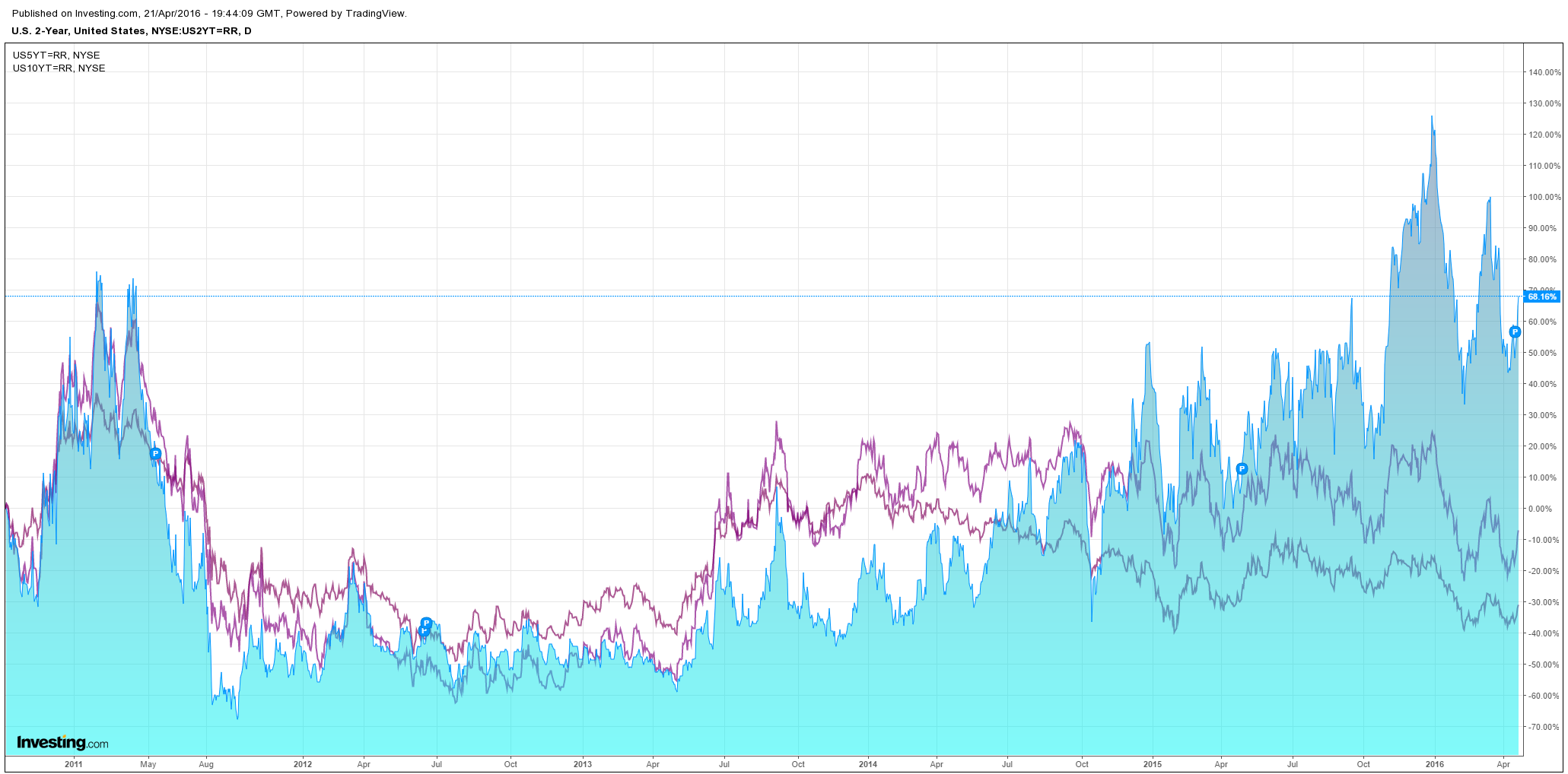

US yields continued to climb as the commodity rally breaths hope into Fed hikes:

Advertisement

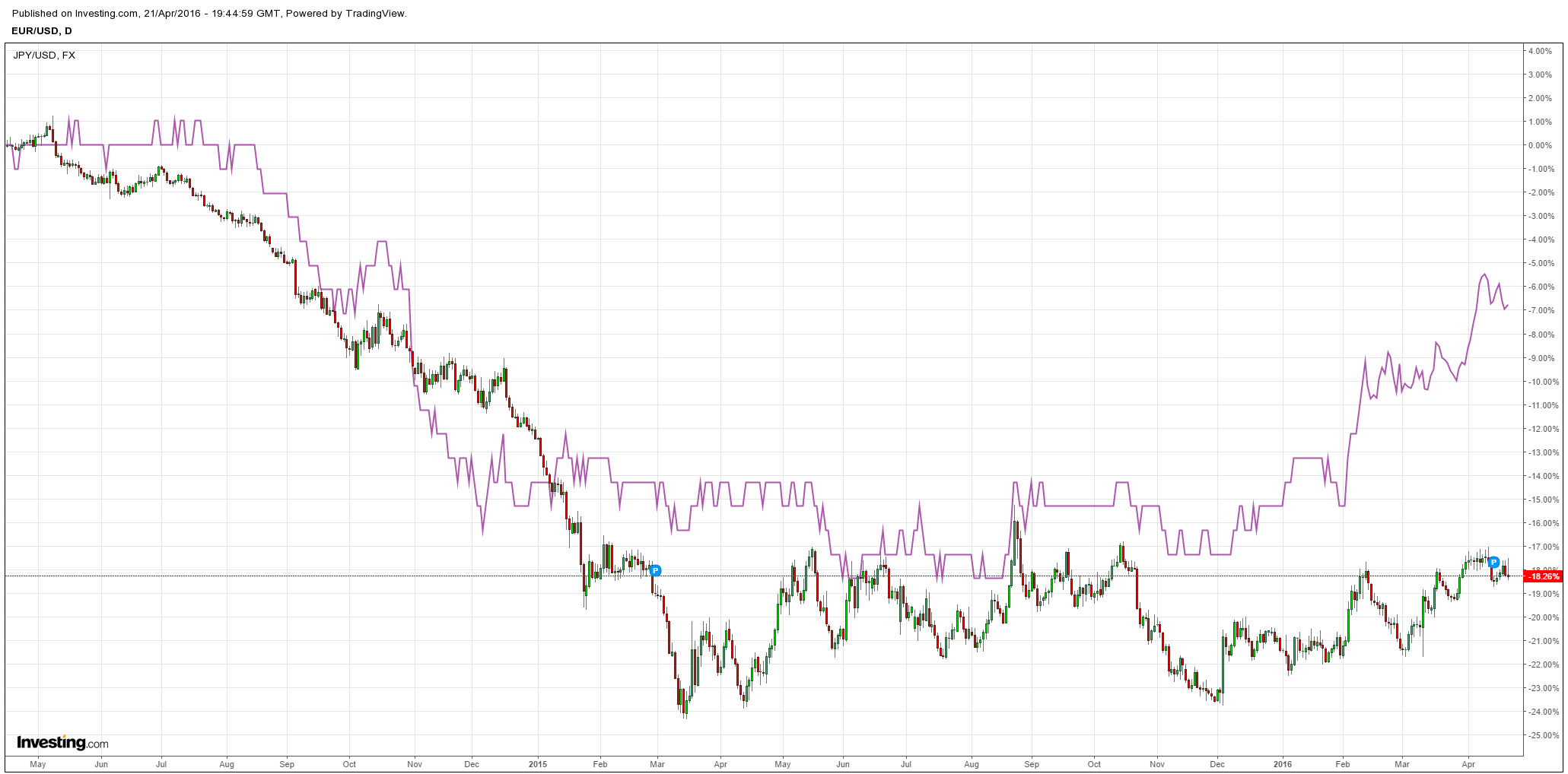

The euro was weak to boot on a dovish Mario Draghi but the yen was up a touch:

Commodity currencies all gave back recent gains:

Advertisement

As Brent pulled back too:

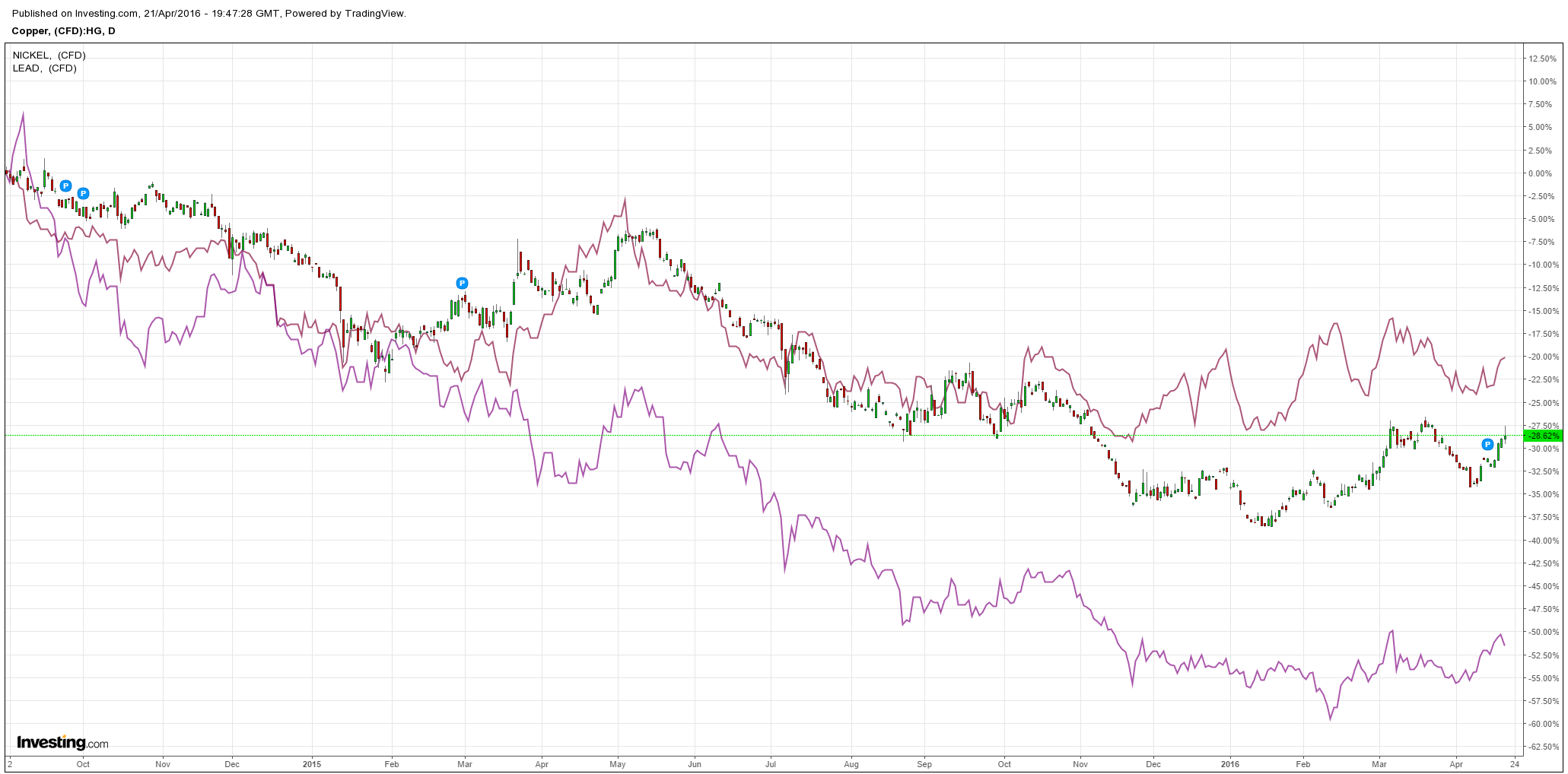

As did base metals:

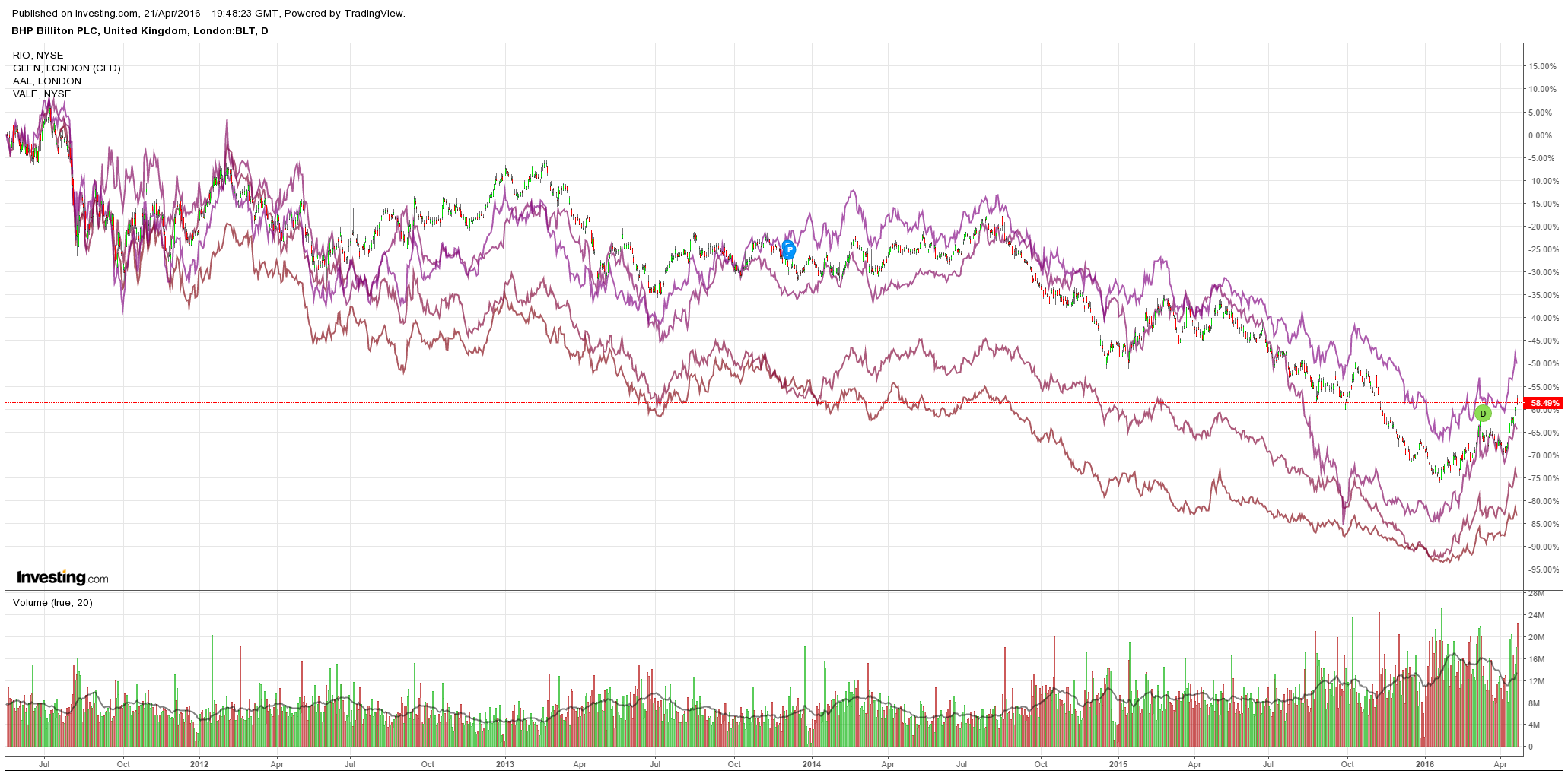

And miners despite wild iron ore:

Advertisement

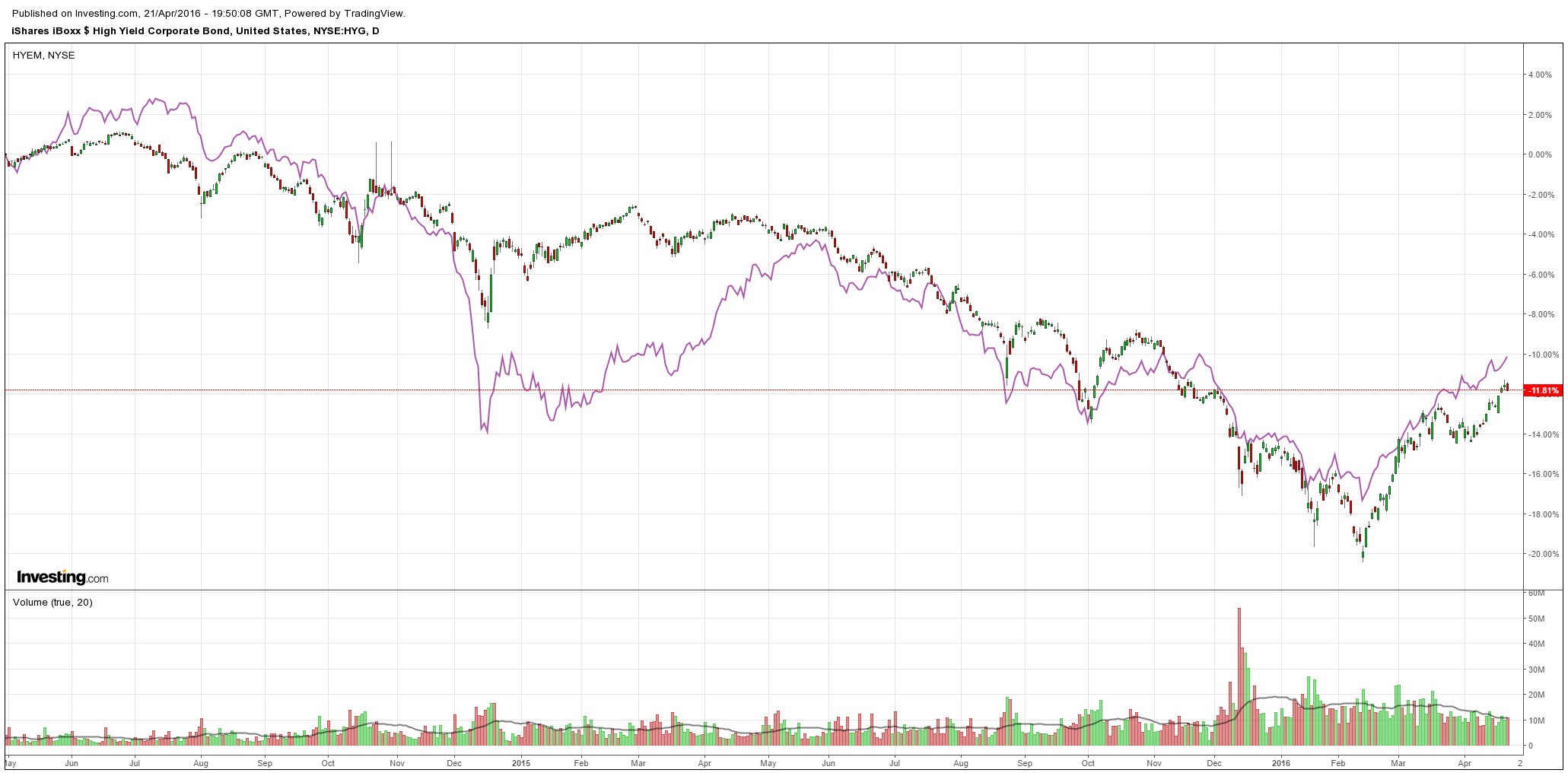

US high yield stalled but EM kept on keeping on:

Not a convincing turn yet.

Advertisement

In wider news, Bernstein offers an insight into why the Chinese end of the Mining GFC is not going away anytime soon:

The survey results confirmed several things we had expected on Chinese households’ attitudes towards money, such as high savings rates, deep penetration of banking products and low household leverage. However,three things stood out to be most surprising to us:

– A lack of financial sophistication: Given our sample is confined to the top-25% households in China, which should have a high degree of financial proficiency. However, the survey reveals a surprisingly low penetration of WMP, trust and capital market products, at 29%, 26% and 10% respectively. This is in deep contrast to the high property ownership at over 75% for the group and highlights the potential room for asset reallocation for the wealthy households in China.

– Consistent savings rates across age: Our cross-sectional analysis revealed several powerful drivers of propensity to save or invest in China, including household asset value, number of young kids and debt burdens, but interestingly age is not one of them. In general we have seen a largely consistent saving/ investment rate at 40% range across age buckets. This raises questions on the idea that the younger generation (at least the wealthy ones) in China is more geared towards consumerism than their parents (and the prospect of China pivoting towards a consumption-led economy).

– The chase for high yield (and high-volatility) products: With the memory of A-share market turmoil still fresh, we thought that risk aversion is the dominant theme in the near term. However, our respondents uniformly plan to increase their exposures to high-yield and high risk products in the near term. WMPs, capital market products and trust are set to gain most popularity in the next 12 months, at the expense of traditional bank deposits and protection assets such as pension and medical insurance. The structural shift of household asset away from bank deposits appears to be non-stoppable and will force traditional financial institutions like banks to adopt new funding strategy and business models.

Undaunted by the recent turmoil in A-share and FX markets,most of the respondents plan to increase their exposures to relatively high-risk products in the near term.

– WMPs, capital market products and trust appear to be gaining popularity most with 13-18% of our respondents planning to start investing in these products in the next 12 month. Insurance, MMFs and capital market products are also attracting more interest from investors.The shift to risky products is at the expense of traditional savings and protection investments, with 14-22% of respondents plan to cut their exposure in deposits, pension and medical insurance (Exhibit 34). This is in line with the continuing household investment’s shift towards non-bank channels away from low-yield bank deposits (Exhibit 35).

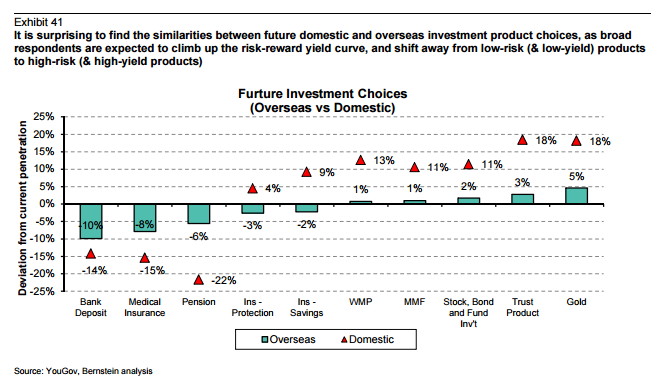

– For investment outside China, the tendency to chase yield and embrace high-risk products is also evident (Exhibit 41), with gold, trust and capital market products gaining most penetration. It is also interesting to see that individuals with lower wealth and higher savings propensity are getting more aggressive in asset reallocation away from traditional safe bank deposits and protection investment. (Exhibit 42, Exhibit 43).

If China is forced to keep cutting rates then its yield-hungry and risk-ignorant masses will keep doing what they do: leaving. And that means a weak yuan.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific's leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.