Mining GFC smoulders on solid US jobs

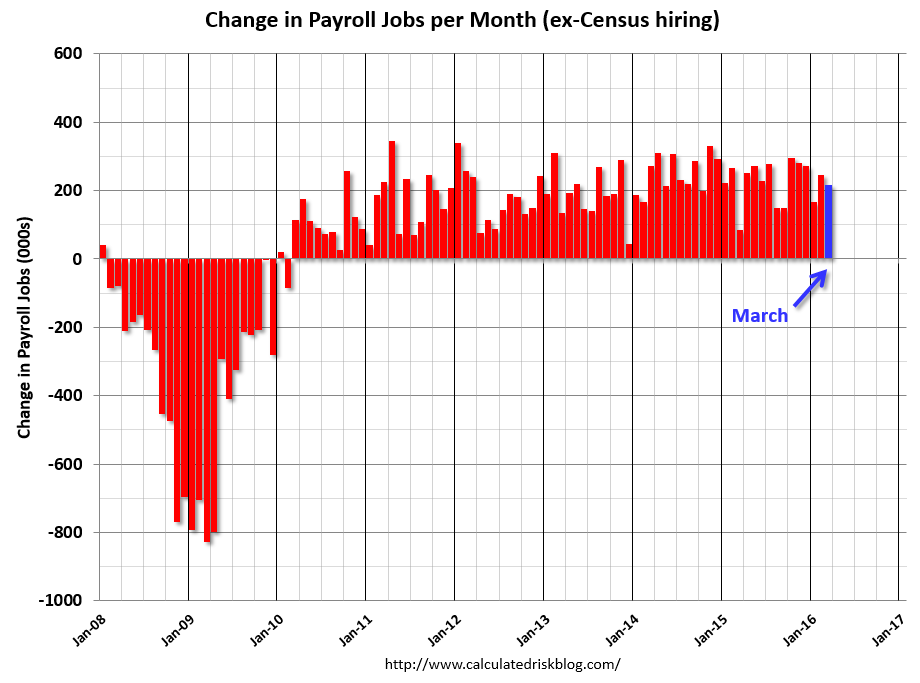

The Mining GFC continues to form the backdrop to markets and global economies as China weakens (albeit with a little bounce) and the US strengthens (albeit with a now cautious Fed). Good US jobs Friday again confirmed the underlying dynamic as 215k marginally beat expectations (charts from Calculated Risk):

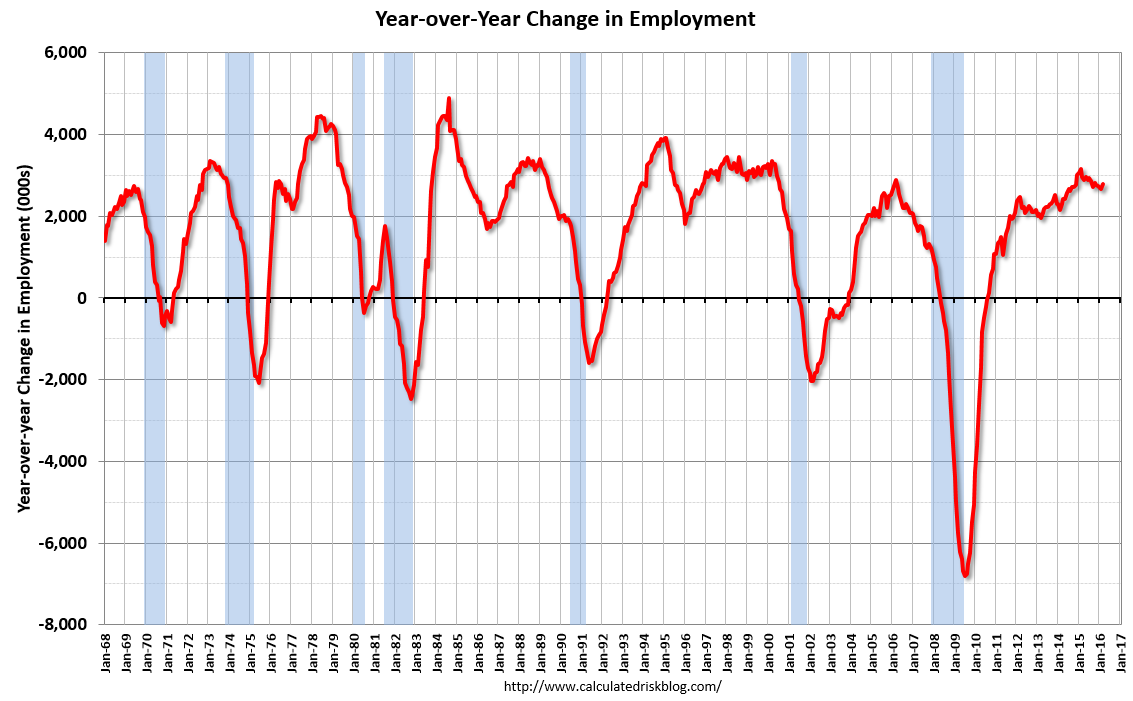

Year on year growth is solid:

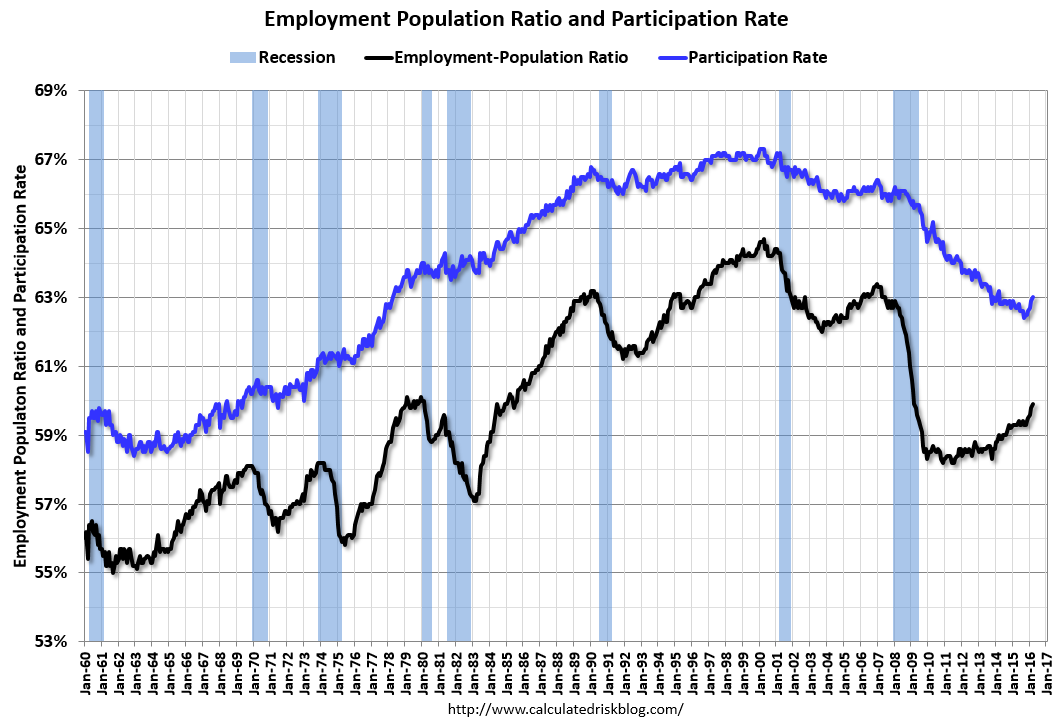

The participation rate has lifted:

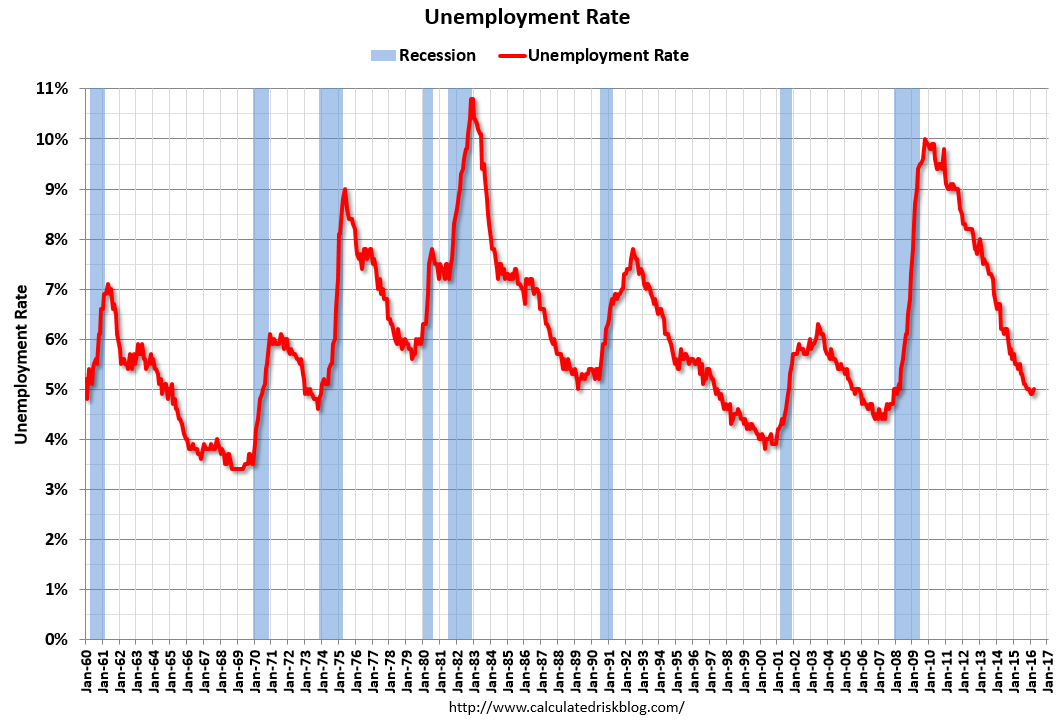

Leading to a rise in the headline unemployment rate:

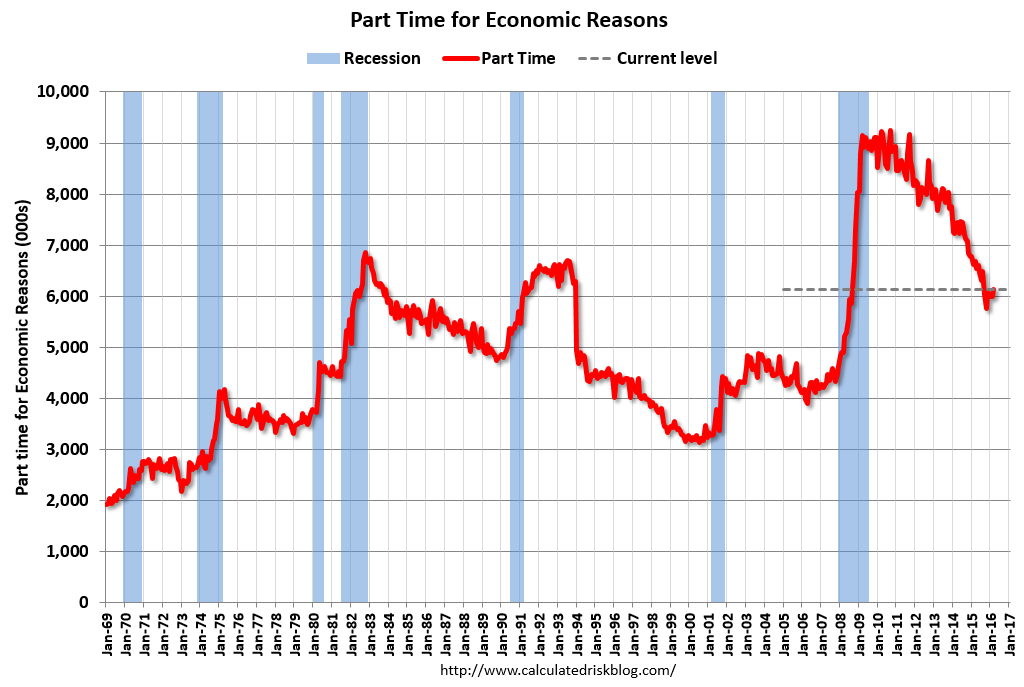

As well as idled part-timers:

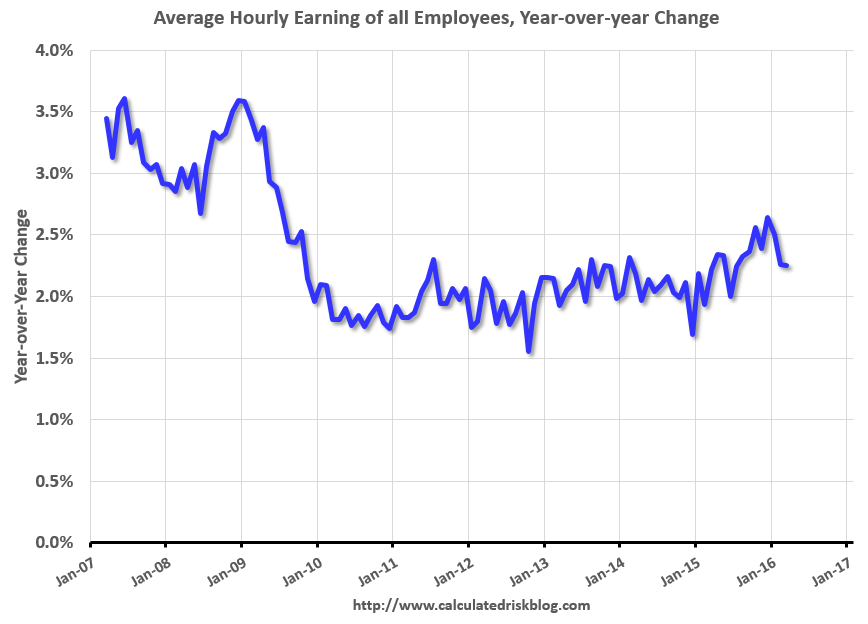

Which has held back salaries (that continue in a gentle uptrend):

Goldman now sees three rate hikes:

BOTTOM LINE: Nonfarm payroll employment rose by a solid +215k in March and the household survey’s measure of employment rose 246k. The unemployment rate rose to 5.0% due to a one-tenth increase in the participation rate. Average hours were unchanged while average hourly earnings rose 0.3%. We have made no changes to our Fed call, and continue to expect the FOMC to raise rates three times in 2016.

MAIN POINTS:

1. Nonfarm payroll employment increased by 215k in March (vs. +205k consensus), a slight deceleration from an upwardly revised +245k in March. Employment gains were relatively broad-based, led by solid gains in service sector jobs (+199k). Warmer than usual March weather may have provided a slight boost to sectors most sensitive to weather: construction (+37k) and leisure and hospitality (+40k) employment were both firm. The other goods-producing sectors of the economy were slightly softer, as manufacturing (-29k) and mining and logging (-12k) continued to shed jobs in March. Government employment rose 20k.

2. Average hourly earnings rose 0.3% in March (vs. +0.2% consensus), raising the year-on-year growth rate to 2.3% from 2.2%. Aggregate weekly payrolls—the product of employment, average hourly earnings, and average weekly hours—rose 0.4% on the month as the average workweek held steady at 34.4 hours while average hourly earnings rose 0.3% (mom).

3. The household survey showed a gain in employment of 246k in March, following an increase of 530k in February. Despite the strong gain in employment, the unemployment rate rose to 5.0% (5.001% unrounded) due to a one-tenth increase in the labor force participation rate to 63.0%. The participation rate has now risen 0.6 percentage points since September. The U6 underemployment rate rose to 9.8% from 9.7% due to the entrance of new job seekers to the labor force.

4. We have made no changes to our Fed call, and continue to expect the FOMC to raise rates three times in 2016. The economy is close to full employment and growth continues to hold up well, financial conditions have eased substantially since earlier this year, and core inflation has firmed. Thus, we ultimately think the committee will move faster than the two-hike pace implied by the latest “dot plot”, despite the dovish signals from the March meeting and Chair Yellen’s remarks this week.

Some folks won’t take “yes” for an answer. This was another Goldilocks employment report with good gains and weak wages inflation. There are only two rate hikes here for this year and none at all if oil rolls over again. Which is, presumably, why the US was not impressed and remained weak:

Commodity currencies were strong:

Oil was very weak as the OPEC non-deal looks ever more shaky:

The base metals rally largely faded too despite the positive Chinese PMI:

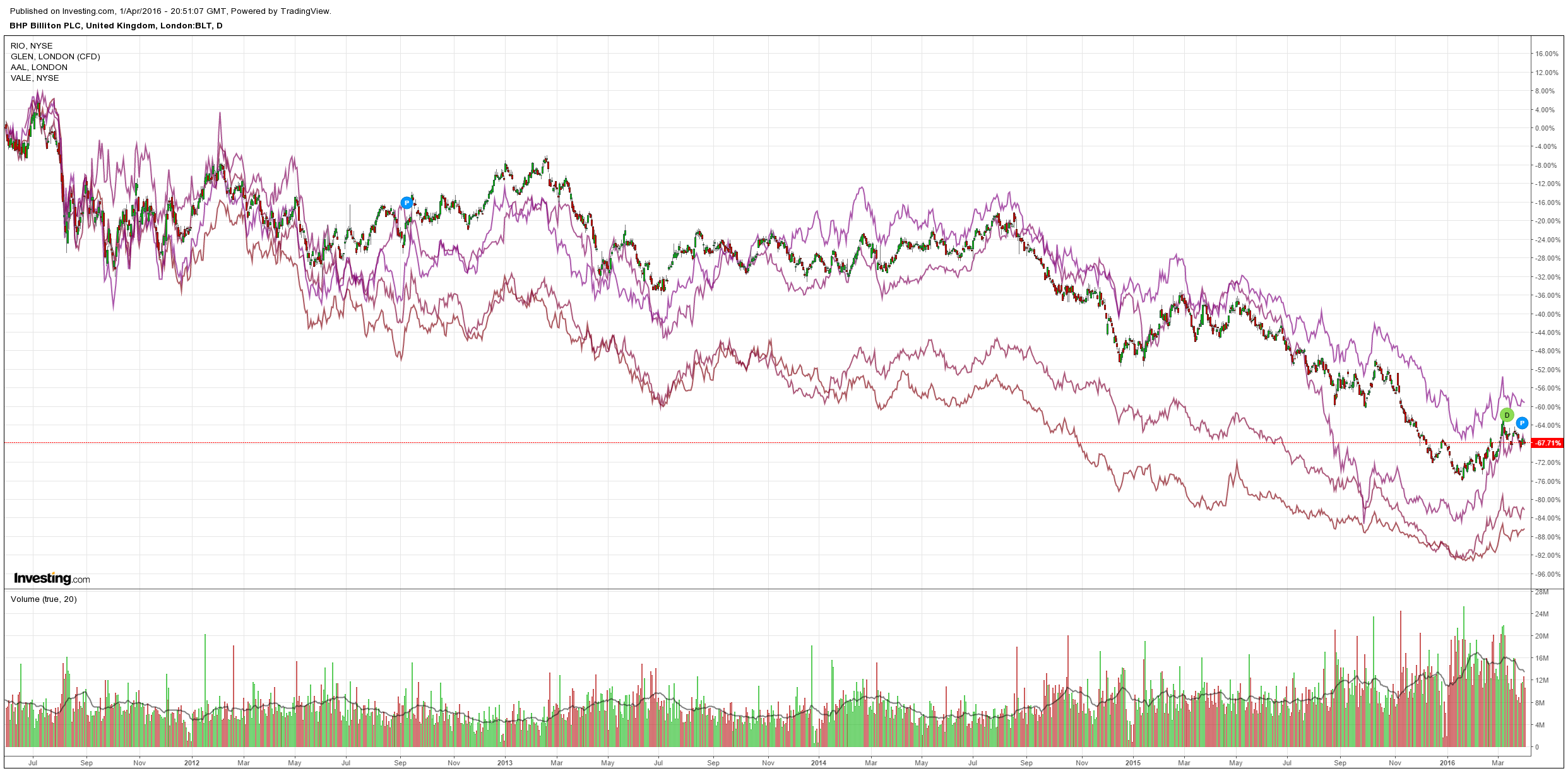

Big miners were flat:

High yield debt was weak:

With Janet Yellen joining the global currency war last week we may yet see more US dollar weakness before a turn. Still, with the US economy soldiering on, Europe in deepening crisis, Japan lost in Abenomics and China enjoying only fleeting firmness, the US dollar remains the ‘cleanest dirty shirt’.