Mining GFC smashes into quantitive failure

Not a pleasant night for the Mining GFC observer. The US dollar was firm:

Commodity currencies were pounded, including the Aussie:

Brent oil softened:

Base metals were crushed, copper especially:

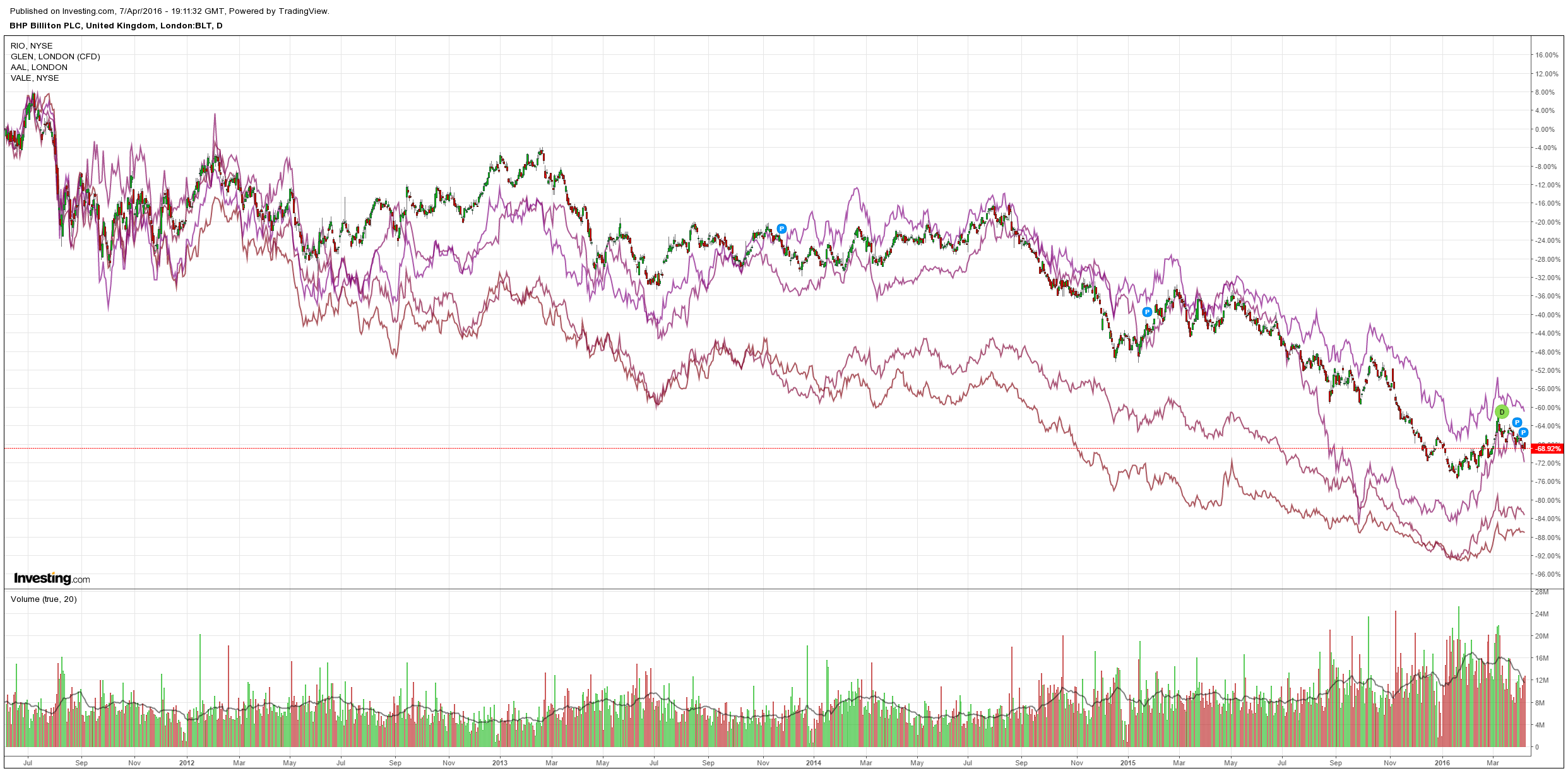

Big miners were hit:

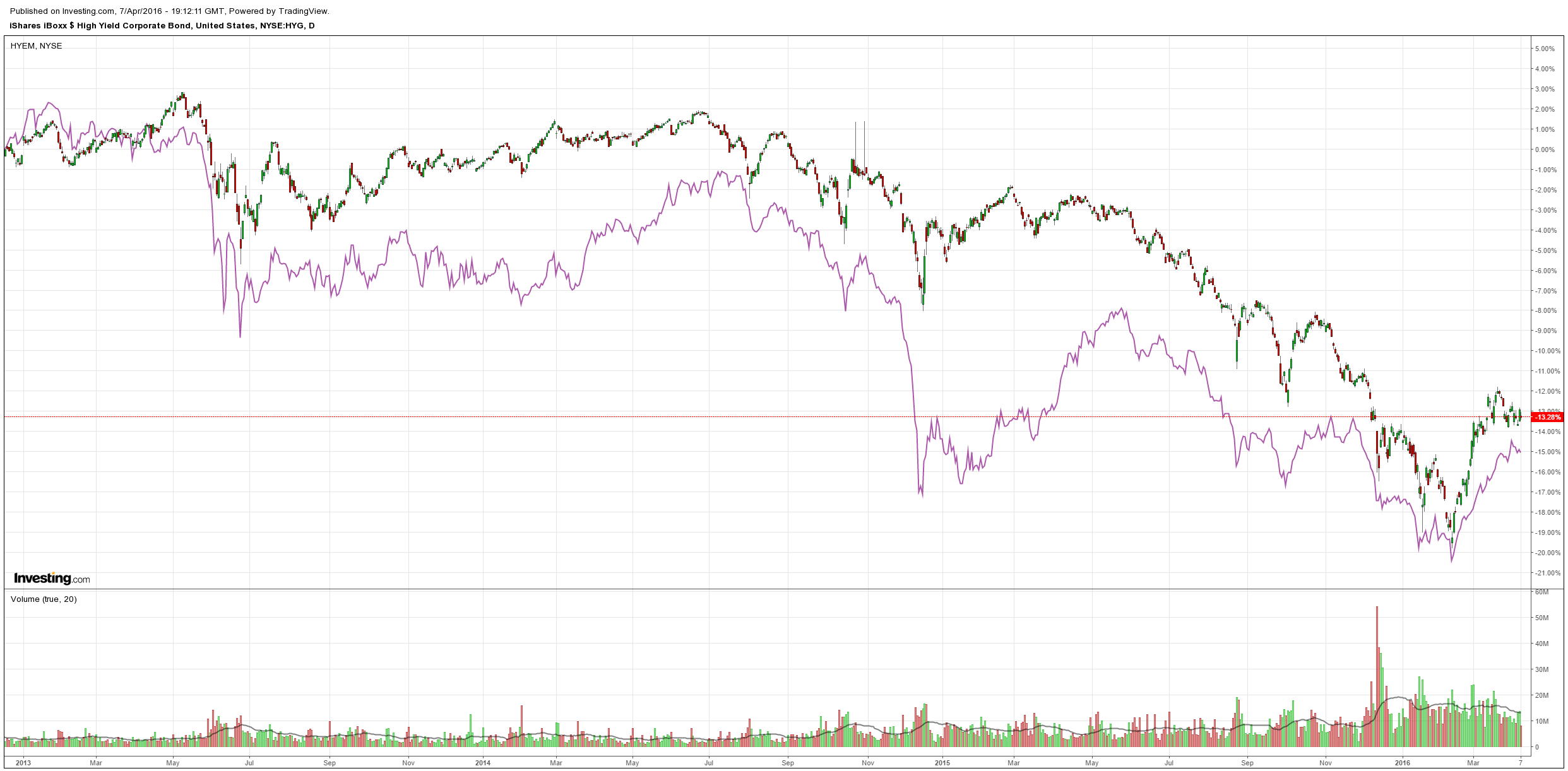

And US/EM high yield sold:

Stocks were hit hard too and bonds rallied big. But the evening’s focus was on the yen and euro, both of which are strong, especially the former:

The Mining GFC is driven by a firming US economy and dollar and softening Chinese economy and yuan. In recent months we’ve seen both the Fed and PBOC work hard to short-circuit this dynamic in forex. However, two casualties of that are now the yen and euro which are rising despite their own very extensive easing programs. Given both are export economies (insanely so in the case of Europe) markets are now concerned that growth will be hit in both.

Moreover, both the ECB and BOJ central bank easing programs now look close to exhaustion, raising the prospect of quantitative failure. From Credit Suisse on the ECB:

Here below, we update our views on negative rates and our consequential short European Banks equity and sub debt thesis. In a nutshell, we think that not only no bank is ever designed to survive in an environment of deeply negative rates for a prolonged period of time, but their business model is further impaired by negatively sloping interest rate curves. In a twisted unwelcome side-effect following ECB meeting, curves are ever closer to inversion in Europe. They recently became inverted in Japan, for the first time since 1994.

Drivers below, in no particular order:

1. Deeply negative interest rates for a prolonged period of time.

Banks’ business model is at risk. If deeply negative interest rates is the way forward, it doesn’t matter consolidation or bad banks talks or country-specific policymaking (e.g. Italy or Europe): the business model is impaired, needs a rethink/restructuring, even before FinTech is taken into account. No bank is ever designed to function in durable negative rates environment. It is a profitability issue, not a balance sheet problem. Banks’ capitalisation then, however healthy it may seem today, may have to be looked at as no more but the number of years of negative profitability it can withstand before a recap is eventually needed. A fragile banking sector is the Achilles heel of the equity market overall, paving the way for gap risks to the downside.

2. Inverted interest rate curves.

Now then, one more element is potentially adding to negative rates in impacting banks’ business: negatively-sloping interest rate curves. The spread between 10y JGBs and overnight rates turned negative in Japan last month. The same spread in Germany is only 20bps steep. Charts attached below. The curve steepness tightly correlates, in broad terms, to how much of a spread profit is left for banks when lending to good large businesses in Europe. No creditworthy business in Europe will accept borrowing for the longer term at much higher costs than that, especially when factoring in a weak-inflation environment. Incidentally, such business is better off borrowing for shorter terms, at more inverted curves, for then rolling-over such debt at a time when it has better visibility on how things evolve in the real economy and if the inflation outlook deteriorates from here or not.

3. In deflationary economy, demand for loans is anaemic.

By subsidising T-LTROs to the private business sector, Draghi was masterful in avoiding immediate damage to the banking sector. Banks’ agonising core business model was given a breathing space, in the name of helping the real economy. Surely a smart and well-thought system of incentives. However, as Keynes once wrote, quoting the old English proverb, “You can lead a horse to water but you can’t make him drink”. The lack of positive real expected returns dampens new investments in hiring plans, plant & machinery, and related borrowing and credit formation with it. Thus, making Draghi’s move just another artefact of financial leverage, not a game changer.

4. No more safety net in the near term for markets.

If anything, Draghi has now gone closer to full exhaustion of his arsenal of policy tools. Last year, we estimated for Central Banks to be 70% done; we may now argue for their arsenal to be more than 80% exhausted. Their lack of policy space from here is evident. The failed repression of volatility post ECB and the reaction of the EURUSD are there to testify it. Current policies can be expanded, new tools can be devised, but their marginal effectiveness is clearly free-falling. Next time around, a troubled equity market will have less of a safety net in the build-up of expectations into the subsequent ECB meeting.

And Bank of New York Mellon on the BOJ:

Clearly, the JPY’s retreat would help (a fact highlighted by Shinzo Abe’s swipe at the G20 this week (or a much smaller subset) when talking to the WSJ: “we must definitely avoid competitive devaluation”); but even if we were to assume that USD/JPY will soon return to the ‘steady state’ (117-123) range in which USD/JPY resided last year (via intervention or otherwise), what Japan now needs is more ‘boost’ than ‘pain relief’. Yet this is where the unending trials of Abenomics have met with a fresh dilemma. Monetary policy may well have run its course and it is far from clear what it could achieve that the post 2012 monetary blitz could not – particularly given the constraint of the aforementioned steady-state range for USD/JPY. And understandably, the negative interest rate policy has its detractors, not least on the BoJ Board; yet, as we learnt from the Bank’s last minutes, the sense is that a sudden repeal of the policy would do more harm than good and so the policy line – per Kuroda’s comments a week ago – is that we must be patient given ‘inherent lags’. So attention has shifted in part to fiscal policy as a result; but here too, the choices are no less unpalatable.

Sources informed Reuters recently that aside from front-loading some spending from the forthcoming financial year’s budget (confirmed by Aso last week), the government will also consider compiling a fresh fiscal stimulus package (we should know around May 26-27). However, there can be no question that such spending could be of a comparable scale to the projects which graced Abenomic’s launch or of any meaningful scale at all for that matter given that recent deficit projections for 2020 have been creeping higher. We have been here before, very recently, and it might reasonably be asked whether the Japanese public are able to see fiscal stimulus without noting the future tax liabilities attached to it (Ricardian Equivalence). Yet there is clearly no basis for a halfway house policy response: the Cabinet either agrees to the need for fiscal rectitude in keeping with Abe’s plans for reform, or they attempt to jump start the flagging recovery with meaningful intent. The dilemma is highlighted by recent headlines: Cabinet Secretary Suga has decried talk of a fresh budget whilst Abe’s noted adviser Koichi Hamada has described the planned consumption tax increase to 10% next April as a “black cloud” hanging over the economy.

Take a moment to consider just how bad this could get Downunder:

- if the ECB and BOJ cannot get monetary traction, quantitative failure will crush Japanese and European banks – two huge sources of offshore funding for Australian banks – and the Downunder funding squeeze will worsen, or

- if the ECB and BOJ succeed in getting monetary traction then the Mining GFC roars back as the USD and CNY jump, crushing commodity prices and Australia’s terms of trade.

In the obvious worst case, which is not as distant as any of us would like, we would witness both simultaneously as global growth sinks.