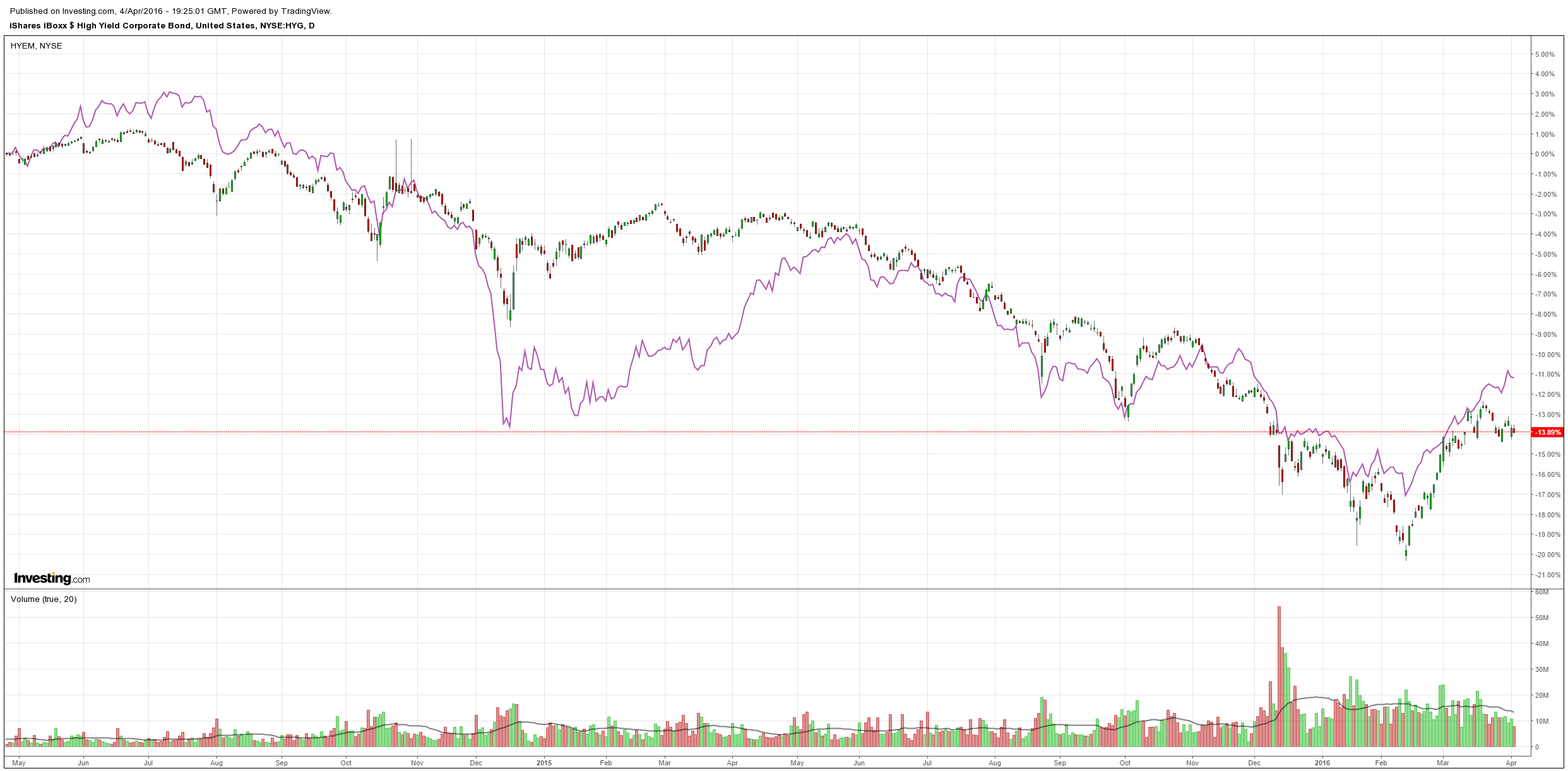

And high yield debt was hit in the US though less so in EMs:

Advertisement

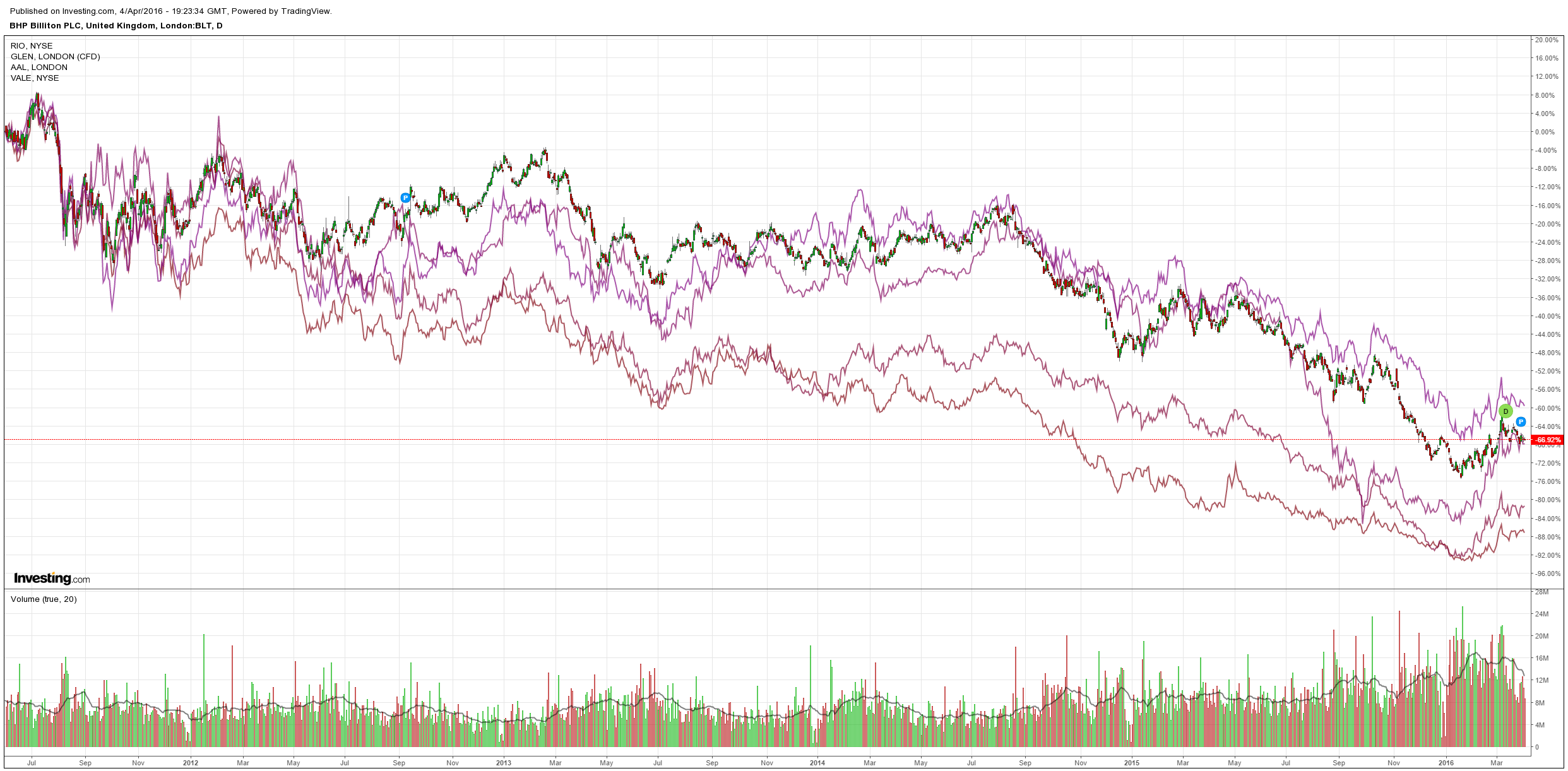

The divergence is no doubt driven by commodity prices falling along with the US dollar. If this continues then Australia will face the RBA’s nightmare scenario in which the terms of trade fall much faster than the currency does.

Thankfully, I can’t see it lasting overly long. One reason for it is a rising euro, which makes no sense at all given its mushrooming political problems around various exit scenarios but nobody ever accused markets of being too focused on the long term, from Credit Suisse:

…we think the ECB’s recent policy measures represent a more meaningful shift in the emphasis of policy: away from a sensitivity to the exchange rate, and towards supporting easy domestic financial conditions.We think the euro area economy and, consequently, the ECB, is now capable of tolerating a stronger currency. Resistance from the ECB to an ongoing appreciation of the euro may not be as forthcoming as many expect.

That’s because the euro area recovery appears to have matured sufficiently that the boost to exports from a weaker currency is no longer necessary to sustain that recovery.

The benefit of the euro’s sharp fall from mid-2014 to early 2015 is illustrated in the two charts below. Figure 2 shows that against a backdrop of extremely weak global trade volumes in the past 18 months, euro area exports performed relatively well. That suggests euro area exporters saw greater market share than would have been the case if the euro had not depreciated.

And that export outperformance delivered a modest stimulus to the euro area economy. Figure 3 shows the contributions to total demand growth (domestic demand plus extraeuro area exports) since the start of the decade. The shift from recession to recovery in the euro area in 2013 was entirely due to domestic demand starting to grow after contracting during the crisis. But, as the chart shows, in 2014 and early 2015 the impulse to aggregate demand growth from this source was limited. Then, a modest additional boost to total demand growth from exports from mid-2014 to mid-2015 allowed the economy to sustain somewhat stronger growth

That stimulus, as well as the fall in oil prices, created the conditions for a strengthening in domestic demand growth through the course of last year.As Figure 3 makes clear, that strengthening took place as the positive effects of the euro’s depreciation began to fade, both in terms of improving market share and export contribution to demand.

As the trade-weighted euro is now around 7% above the lows it reached in early 2015, that stimulus may fade further.

Advertisement

What poppycock. Domestic demand support and currency deflation are the same thing in monetary terms. Moreover, if we see Brexit, Fraxit or Gerxit who cares what the ECB is doing?

I still can’t see why anyone would want to hold euro.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific's leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.