Mining GFC doused as commodities roar

The Mining GFC was heavily doused last night. The US dollar was stable:

Euro and yen consolidated:

Commodity currencies rocketed:

Oil is is now tearing the roof off:

Base metals re-coupled with it:

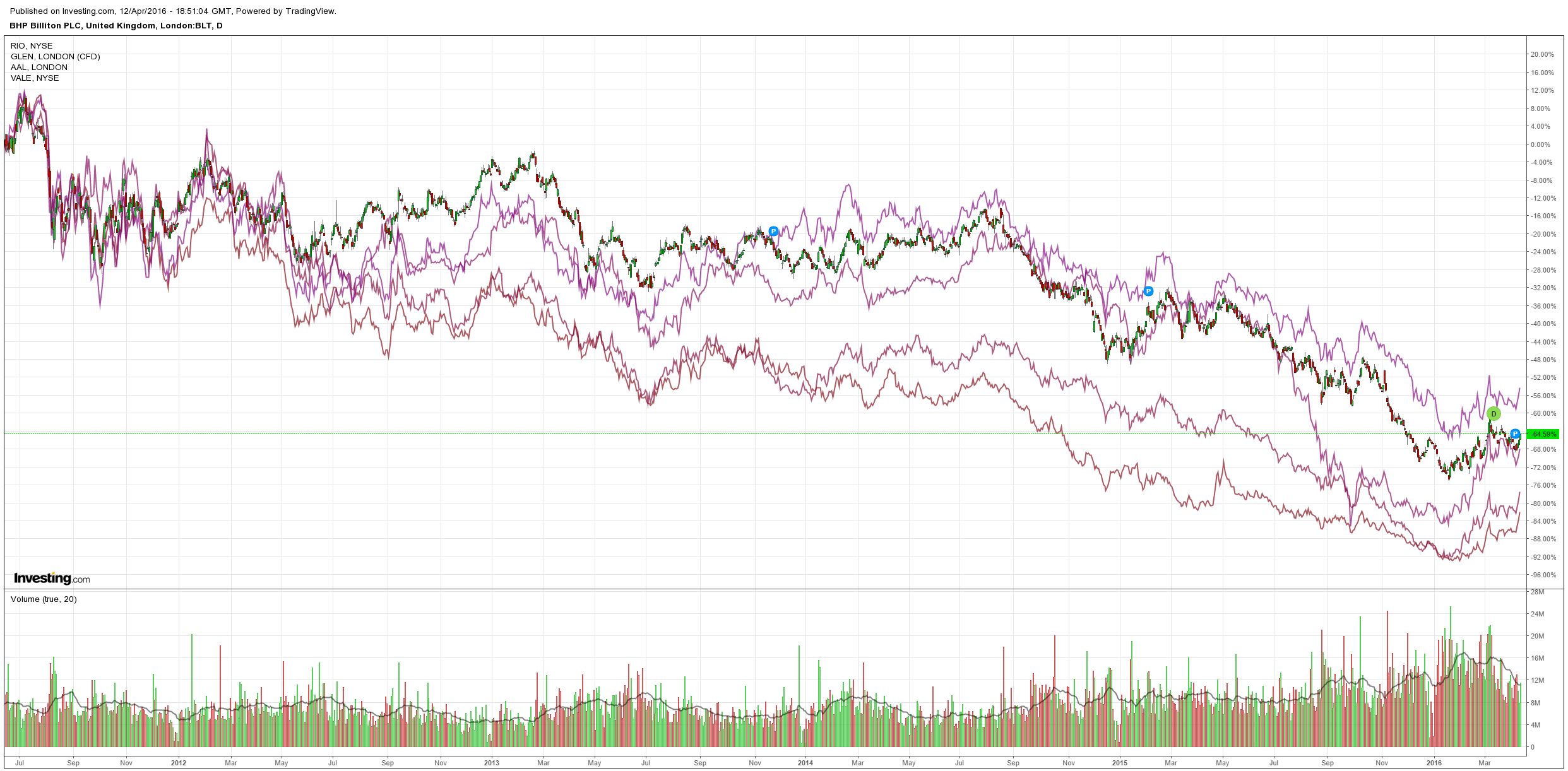

Big miners screamed higher:

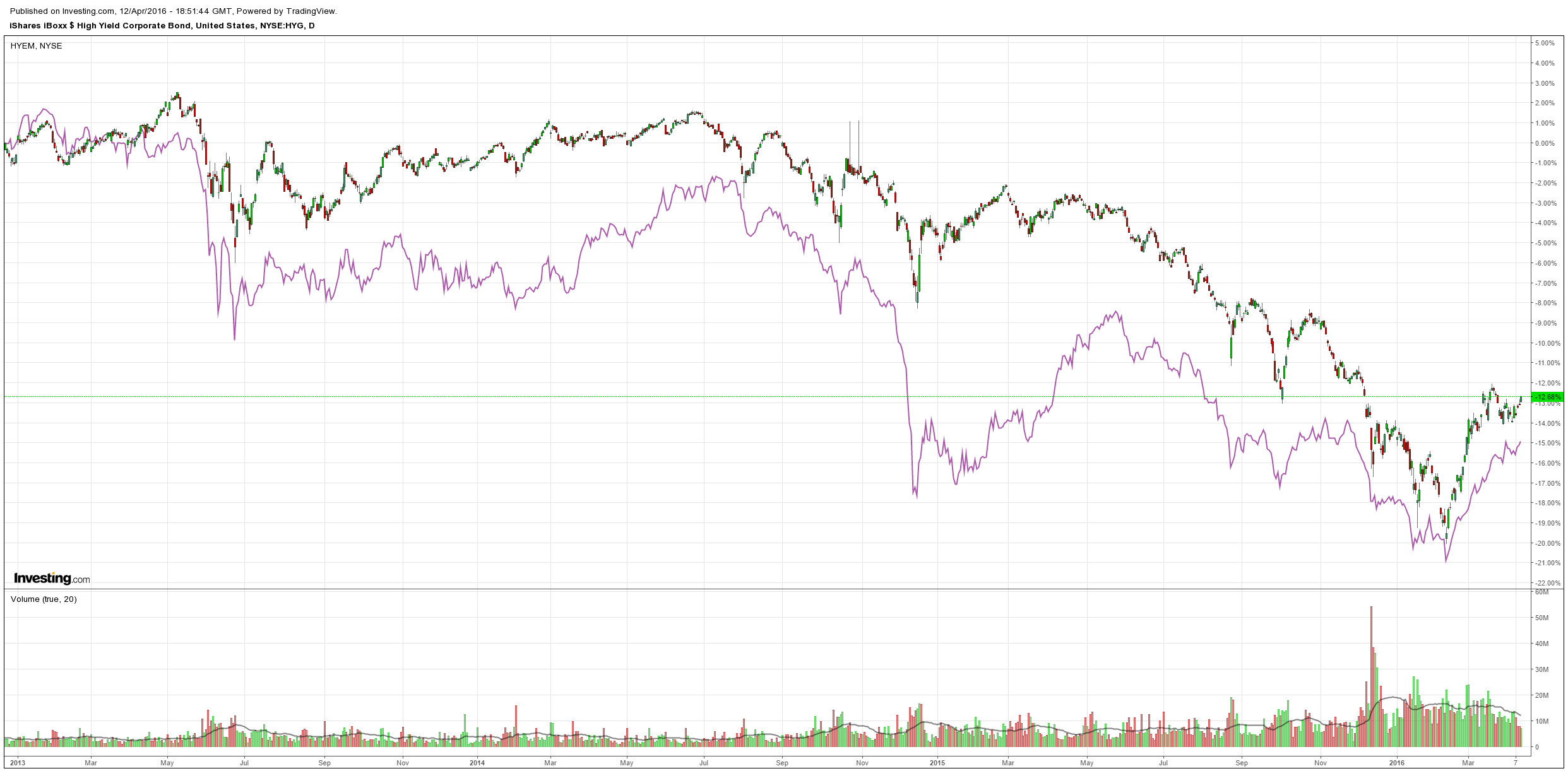

And US as well as EM high yield rebounded but was subdued in context:

We are back to where we were. Oil is free and running on hope with everything else trailing in its wake (stocks jumped, bonds sold). It is an interesting juncture given US shale will begin to warm up at these prices but energy credit markets are still distressed so one of those two is not going to last. We are now looking for that sweet spot where the oil price can meet the cost of funding the marginal cost producer. My estimation is that that is around $45 but if that’s what markets need to see then they’ll overshoot first.

As well, there are lot’s ruminations today that the Mining GFC was deliberately addressed at the G20. Via FTAlphaville from SocGen:

Central bank behaviour is often cited as evidence that the answer is yes; the PBoC has stemmed the RMB slide against the USD and while the ECB cut rates in March, the signal was that deposit rates would go no lower. In the US, the emphasis placed on global risks has reassured markets that the Fed is in no hurry to hike, and the BoJ has (so far) refrained from further easing. The FX market, however, tells a different story with the yen marking new sharp gains last week. Our view is that no “secret” agreement exists and that Japanese authorities will struggle to build a consensus for intervention at current levels.

BofAML has more:

By the end of the weekend it was obvious that the issue of currency manipulation (either via the use of monetary policy or more direct means) had proved a significant topic of discussion with the communique noting that members pledged to “consult closely” on foreign exchange markets. US Treasury Jack Lew expanded on the topic, noting: “…I think the language on exchange rates is very important… it’s important in this communique that there’s a commitment to consult… we’ll keep each other informed and we’ll avoid surprising each other… So I think it’s actually quite important that that language is in this communique. It is also important that all G-20 members honour their commitments to refrain from competitive devaluation, and to not target exchange rates for competitive purposes.Here in Shanghai, we have not only reaffirmed the commitments that we agreed to last year in Turkey, but have gone a step further in agreeing to consult closely on exchange rate policy.” He added to these comments the next day, noting: “Leaving the Shanghai G20 with the risk of competitive devaluation greatly, greatly reduced because of the commitment is significant.”

By the Thursday after the meeting it had become clear which nation these comments were aimed at following the publication of an article in the Nikkei ( http://asia.nikkei.com/Politics-Economy/Economy/G-20-opposition-to-negative-rates-puts-central-bank-on-edge). The paper reported that European economic leaders had “blasted the Bank of Japan’s negative interest rate policy” and quoted Eurogroup head Jeroen Dijsselbloem as saying that debate at the meeting “was also about Japan, to be honest,” noting: “There was some concern that we would get into a situation of competitive devaluations.”

The reaction from Japan was, reportedly, a mixture of exasperation and defensiveness. The Nikkei story quoted an unnamed BoJ official as saying “I don’t really understand the context (for Mr Dijsselbloem’s statement) but I don’t think it quite lines up with reality.” It also noted that others at the bank had responded that leaders in Europe, of all places, had little right to make objections to the use of a negative deposit rate. Finance Minister Taro Aso publicly defended the BoJ’s negative interest rate policy, saying “it has brought down the yield curb and housing loan interest rates, so it is having positive effects” while the LDP’s Masahiko Shibayama, was more combative, telling Reuters “The G20 statement does not place any new restrictions on BoJ policy … I hope the BoJ calmly analyses the impact negative interest rates have had, which should feed into their decision about the next steps to take.”

While Bank of Japan governor Haruhiko Kuroda might have stated that he had “fully gained understanding” from G20 ministers about the BoJ’s thinking with regard to its use of negative rates as a tool to escape deflation, his subsequent comments suggested that the pressure on the bank to refrain from making a further move on its deposit rate had succeeded . On the day after it was published he stated that negative interest rates were not aimed at influencing in the foreign exchange market but assured the market (and, presumably, his G20 colleagues) that he was not considering a more negative rate of interest at that moment in time.

And Citi:

It is probably better to think of G20 as similar to Friedman and Savages s billiards player (link, page 12,13), G20 may not have made a deal but they are behaving as if they did, so we may as well analyze the consequences from that perspective. One question to ask is why they would agree to setting aside currency as a macroeconomic weapon the likely answer is that the winners of the currency war battles may have decided that they were not benefitting enough to offset the negative impact of the ancillary asset market volatility that emerged. Basically they were acknowledging policy ineffectiveness or at least monetary policy ineffectiveness, and the Statement pretty much admitted that.

So we now find ourselves in a situation where G3 has trouble cutting rates. The ECB and BoJ are reluctant because of the strains it is putting on their financial institutions and political unpopularity. The Fed is reluctant for similar reasons and because it seems unlikely that one cut would do great things for the US economy and it would certainly raise a suspicion that negative rates were beckoning. An already unpopular institution would become politically toxic. Bottom line, easing is hard to do. An ECB or BoJ hike is unlikely, needless to say. The Fed has already indicated its reluctance to hike and is very unlikely to hike to defend the currency if anything they seem to be cheering any weakness the USD encounters.

Put this all together and you have an extremely high bar for any G3 central bank cutting rates and an extremely high bar to them raising (and an even higher bar to any of them raising rates in response to currency weakness).

To me this discussion is beside the point. It is effectively putting the jawbone ahead of the reality. The Fed still has plans to tighten. The US economy remains strong enough for it to do so once or twice more this year. The current first quarter growth weakness often cited in “GDP Now” should, in my view, be faded, as Merrill Lynch says:

For the third year in a row, forecasters came into the first quarter looking for 2%-plus GDP growth, only to steadily revise estimates lower. [T]he Atlanta Fed’s GDPNow tracking [has declined] for 1Q in each year. They are far from alone: both we and the consensus have been doing the same thing. This weakness adds to market skepticism about a June Fed hike.

In both 2014 and 2015 we faded the weak 1Q data and argued that the recovery remained on track. Today, we see four reasons to reiterate that call. First, outside of the GDP adding up, the data look fine. Second, some of the weakness is likely due to lingering seasonal adjustment problems. Third, the fundamental backdrop points to moderate growth, not a big slowdown. Fourth, and perhaps most important, with potential growth slipping below 2%, and given the normal variation in the data, we should not be surprised to see near-zero quarters on an annual basis.

And don’t forget, either, that the higher oil goes, the more likely it is that the Fed will pull the trigger again.

Conversely, the European and Japanese economies need more easing and they will innovate for more when they need to. China will enjoy a couple of quarters of better growth and then need more easing too. That is, the forex dynamics of the Mining GFC are based on fundamentals not just a currency war.

If markets are discounting the Fed moving post-tightening before we get there based upon a conspiracy theory then that is the definition of ludicrous. At the risk of being overly sane, my preference remains seeing current market moves as an ongoing cyclical “pain trade” within the larger trend. That is, a bear market rally.