The Mining GFC is a memory now. Or is it? The US dollar took off:

The yen and euro sank:

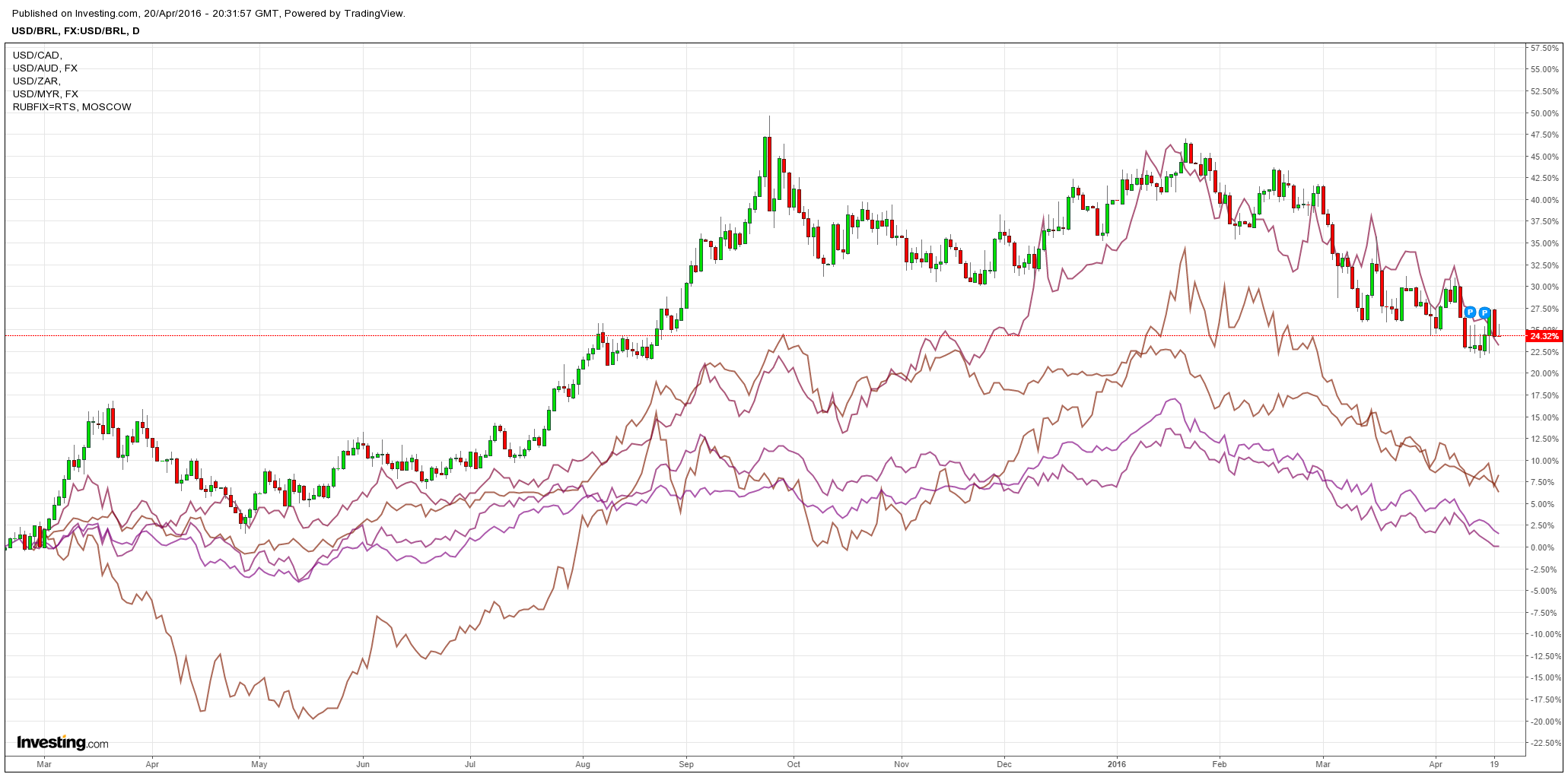

Commodity currencies were mixed as the Aussie fell but anything oil exposed jumped:

Advertisement

As did oil:

And base metals:

Advertisement

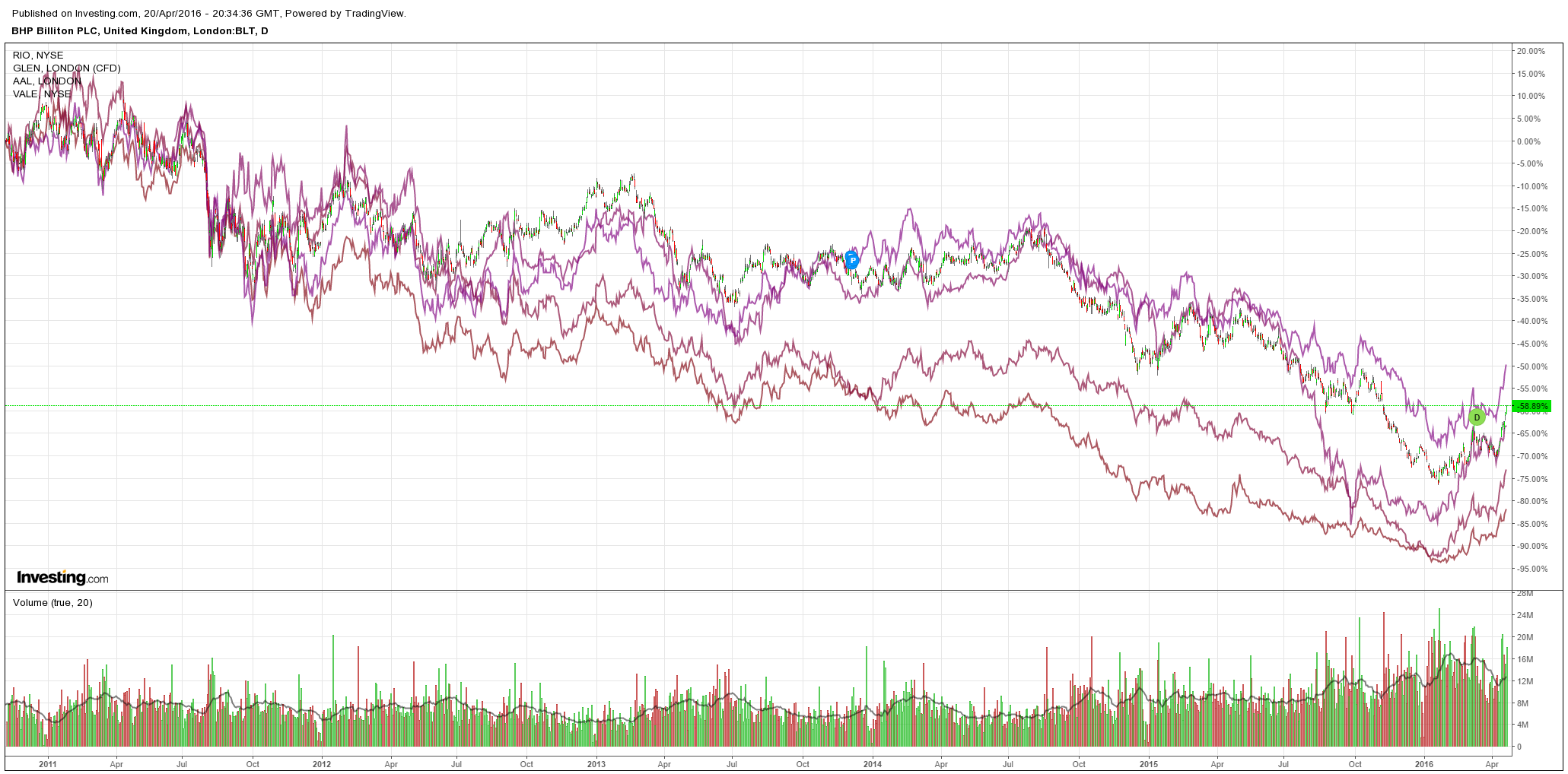

And miners:

And high yield debt:

And stocks:

Advertisement

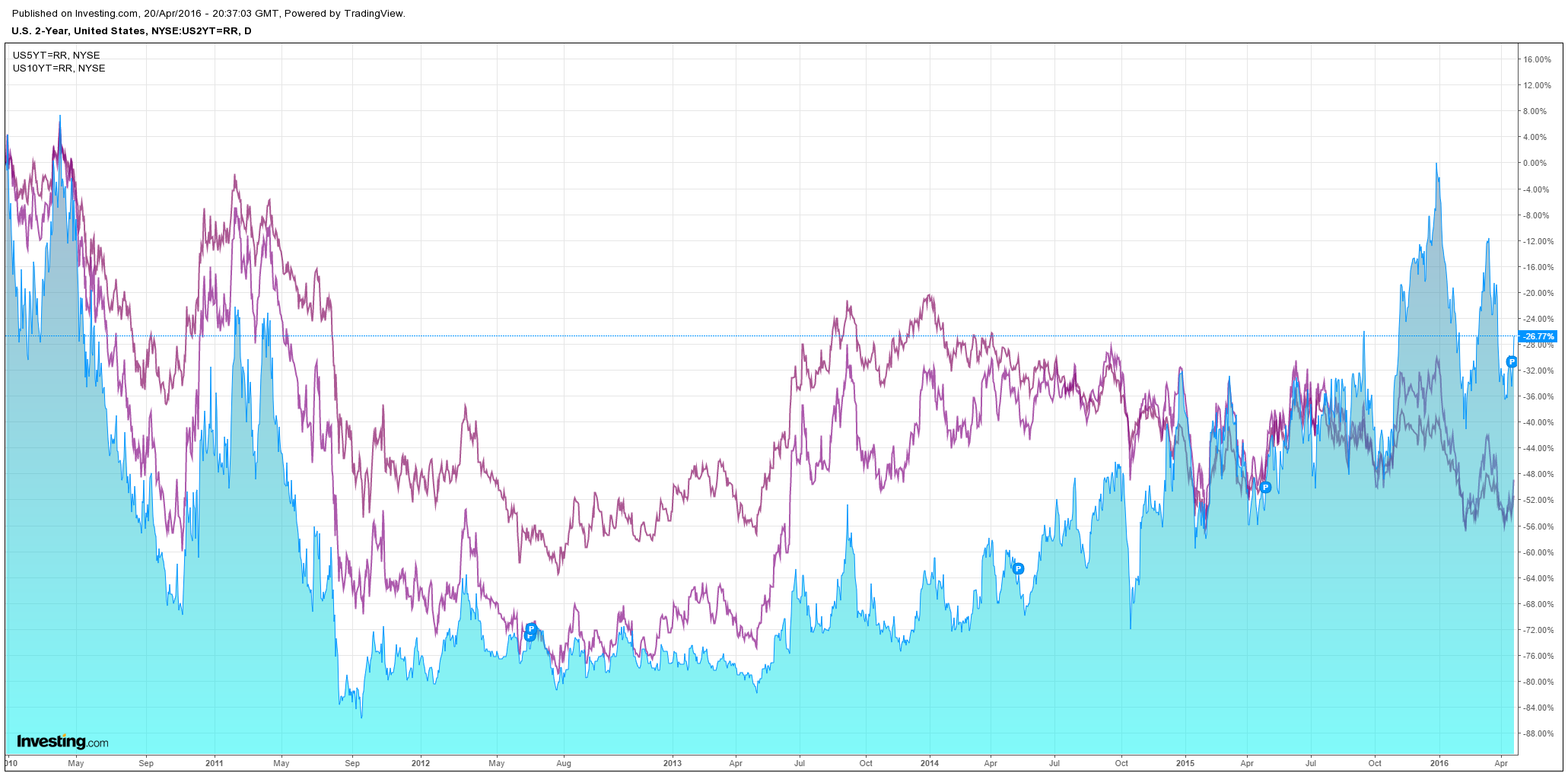

And bond yields:

But wait, is that right? Did I just say that the Mining GFC is a distant memory as the US dollar and bond yields both powered up? Yes, I did. That doesn’t add up does it? Given the Mining GFC is caused by a firming US economy, bond yields and dollar then didn’t it just get worse? Yes, it did!

In short the Mining GFC is not over. For now it is being held in check by the missing second driver, which is fading strength in China, its yields and yuan.

Advertisement

The first driver is about to get fired up again, though, as Goldman says:

The Bank of Japan (BOJ) is due to hold its next monetary policy meeting (MPM) on April 26-27. To date, our base-case scenario has been for additional easing at the June MPM, and we had regarded possible easing at the April MPM as a risk scenario (see our February 17 Japan Views). However, we now make easing in April our base-case scenario, given the rising risk that business confidence has been dented by recent financial market instability and the Kumamoto earthquakes, and in view of BOJ governor Haruhiko Kuroda’s recent proactive statements on possible additional easing in response to the sharp deceleration in inflation in April.

At its end-January MPM, the BOJ decided to introduce a negative interest rate to head off the risk that rising financial market volatility could dampen business confidence and delay the shift away from a deflationary mindset. We think the BOJ would have originally been looking to keep monetary policy unchanged at the April MPM while it assessed the effect of the negative interest rate, given that it generally takes at least six months for policy effects to become apparent.

However, market volatility did not let up, and the yen continued to appreciate and share prices continued to be unstable despite the introduction of the negative rate. On top of that, the Kumamoto earthquakes in mid-April have caused significant supply chain disruption in the manufacturing sector, particularly in transportation equipment, heightening concerns that business confidence could deteriorate further. In addition, the failure at the end of last week of the major oil producing nations to reach a deal to freeze oil production casts further doubt on the BOJ’s consumer price outlook, and the latest G-20 meeting confirmed a major gap between Japan and the US on appropriate currency levels, reducing considerably the likelihood of currency market intervention.

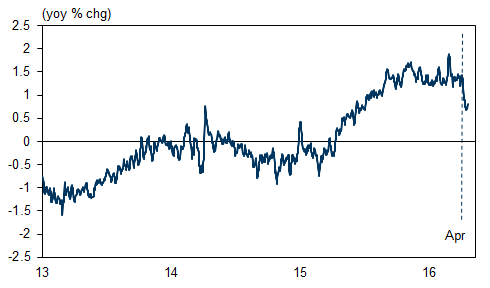

We also note that the daily price index (Nowcast), frequently cited by Governor Kuroda as evidence of bullish corporate price setting, has slowed sharply in April (see Exhibit 1). We have forecast that inflation would stall particular from the start of in the new fiscal year as the cost-push factor due to past weak yen fades away, but the slowdown has been slightly more rapid than we had expected. We now see a stronger likelihood that March nationwide core CPI (yoy), due out the same day as the April MPM, could be negative.

Governor Kuroda’s recent proactive comments regarding the possibility of additional easing have also been attracting market attention. In an interview published in the April 18 Wall Street Journal, Mr. Kuroda said, “If excessive appreciation continues, that could affect not just actual inflation, but even the trend in inflation through its impact on business confidence, business activity, and even through inflation expectations. Although our monetary policy is not targeted to the exchange rate, we continue to carefully monitor exchange-rate movements. And as I always emphasize, if necessary to achieve 2% inflation target at the earliest possible time, we would not hesitate to take further easing measures”.

Taking these words at face value, we believe the BOJ would likely need to act in the face of the recent market situation, the continuing deterioration of business confidence and inflation expectations, and the rapidly decelerating aforementioned daily price index. Based on the above, we think the probability of the BOJ opting for additional easing at its April MPM has risen sharply of late.

The main issue for the BOJ, in our view, will be the means of applying additional easing (Exhibit 2). From an exchange rate perspective, the most effective means would be to widen the negative interest rate.However, financial institutions have not reacted positively to negative interest rate and we think there is a general unease among the population with respect to the policy, so we think the BOJ is unlikely to take rates deeper into negative territory at this stage.

Another option would be to increase quantitative easing by again stepping up JGB purchases (currently at the rate of 80 trillion yen per year), but the marginal effect would be minimal as the decline in the yield curve is already more than sufficient, and we think additional expansion would even risk giving the impression that the BOJ is closer to the limit of purchasing JGBs at the current pace.

By a process of elimination, we think the BOJ is most likely to ease mainly via the qualitative measure, with increasing ETF purchasing the central pillar, with a view to improving business confidence. We think the market is already factoring in an increase in annual purchasing from ¥3.3 tn to ¥5-6 tn, and we thus think the BOJ may look to slightly more than double its current figure to around ¥7 tn.

We also see a possibility that the BOJ may combine the expansion of ETF purchases with a cut in the interest rate of its loan support scheme. A cut in the interest rate at which financial institutions can borrow from the BOJ under the scheme from 0% currently to -0.1% would be good news for financial institutions, which have seen earnings depressed by the negative rate on current account balance. Not only would this offset some of the negative impact about the negative interest rate policy, but it might also ease the upward pressure on the yen if the market starts to factor in a possible deeper move into negative territory for interest rates on current account balance in the future.

In addition to the aforementioned lending support scheme, the BOJ also has in place a fund supplying scheme to support financial institutions in areas affected by the Great East Japan Earthquake of March 2011. Under the scheme, which was set up just after that earthquake, the BOJ supplies funds to financial institutions in affected areas, helping those institutions provide funding for restoration and rebuilding work. The interest rate on financing via the scheme is currently +0.1%, the ceiling for total lending is ¥1 tn, and the deadline for new applications is April 30, 2017. We see a possibility that the BOJ may expand the scope of the scheme to cover areas affected by the Kumamoto earthquakes, and that it may cut the interest rate to -0.1% (in line with that of the loan support scheme), increase the maximum lending amount, and extend the application deadline (we note, however, that uptake under the scheme by financial institutions in areas affected by the Great East Japan Earthquake peaked at ¥511.2 bn in April 2012, well short of the ¥1 tn ceiling).

Moar! The Mining GFC is in animated suspension while we float through on moar but as the commodity reflation firms up another Fed rate hike will loom and other central bank cuts will keep upwards pressure on the US dollar.

Advertisement

At the same time, the commodity reflation will bring more dirt back to market.

Yet when China’s boomlet passes, as it must, we’ll find ourselves precisely where we were, with too much dirt, a bloated USD, a falling yuan, broken EMs and another Mining GFC convulsion will begin.

Great commodity crashes are an immensely destructive process.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific's leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.