The Fed has lost its first battle against the Mining GFC, last night pushing out rate hikes largely owing to risks in markets. As such the US dollar was pole-axed:

Commodity currencies jumped:

Oil too:

Base metals rose modestly:

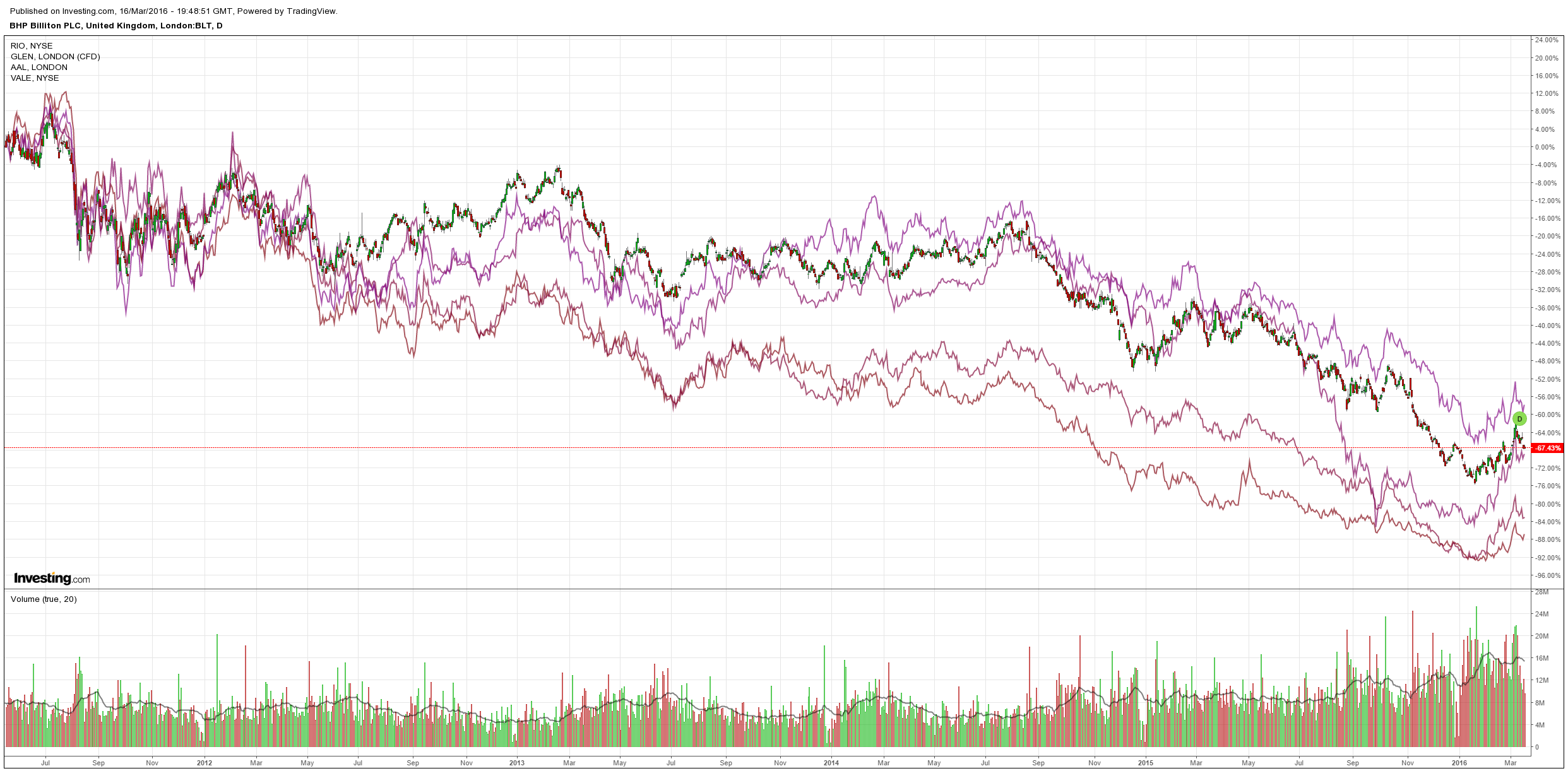

Big miners too:

US/EM high yield debt was selling before the Fed squirted new life into it:

So, who is winning and what does it do to our outlook? My view remains that over-supplied commodity markets will prevail as China continues to weaken and change (especially for Australia’s bulks) so Fed timidity is more a delay in the shakeout process than a change in trend. GMO has it right, I think, from the AFR:

Investors piling back into the US junk bond market are “vulnerable” to suffering further losses and would be better off waiting for prices to correct to a more sensible level, a strategist at asset management giant GMO says.

…The recent headlong rush into junk bond funds “speaks more to the desperation of investors in a low-growth world,” Reganti said, pointing to investors who have been “whipped and driven” by central banks.

“I think [those investors] are vulnerable,” he said.

Mr Reganti believes that rising defaults by non-investment grade issuers in the US oil and gas sector, which are under heavy pressure from the weak oil price, would eventually infect the rest of the junk bond market, sending bond prices lower.

The transmission would be via junk bond fund portfolio managers, who will be forced to sell indiscriminately in order to meet redemptions by investors spooked by defaulting energy companies.

That would spark losses across the high-yield market.

People “always” say that the stress will be contained within one particular sector, Mr Reganti said, but “inevitably contagion spreads”.

“There is a substantial opportunity to build wealth sometime in the next six months, year or two years if you have enough dry powder to buy credit when it reaches valuations that do make sense”.

So long as investors pile back into high yield then US shale oil can hold on and even rebound. But in over-supplied commodity markets that will only result in lower prices and more losses.