European ISIS attacks have reignited the Mining GFC. The US dollar was strong as the unownable euro faded:

Commodity currencies were hit hard:

Oil pitched in, breaking lower though not in trend as yet:

Advertisement

Base metals were weak especially copper:

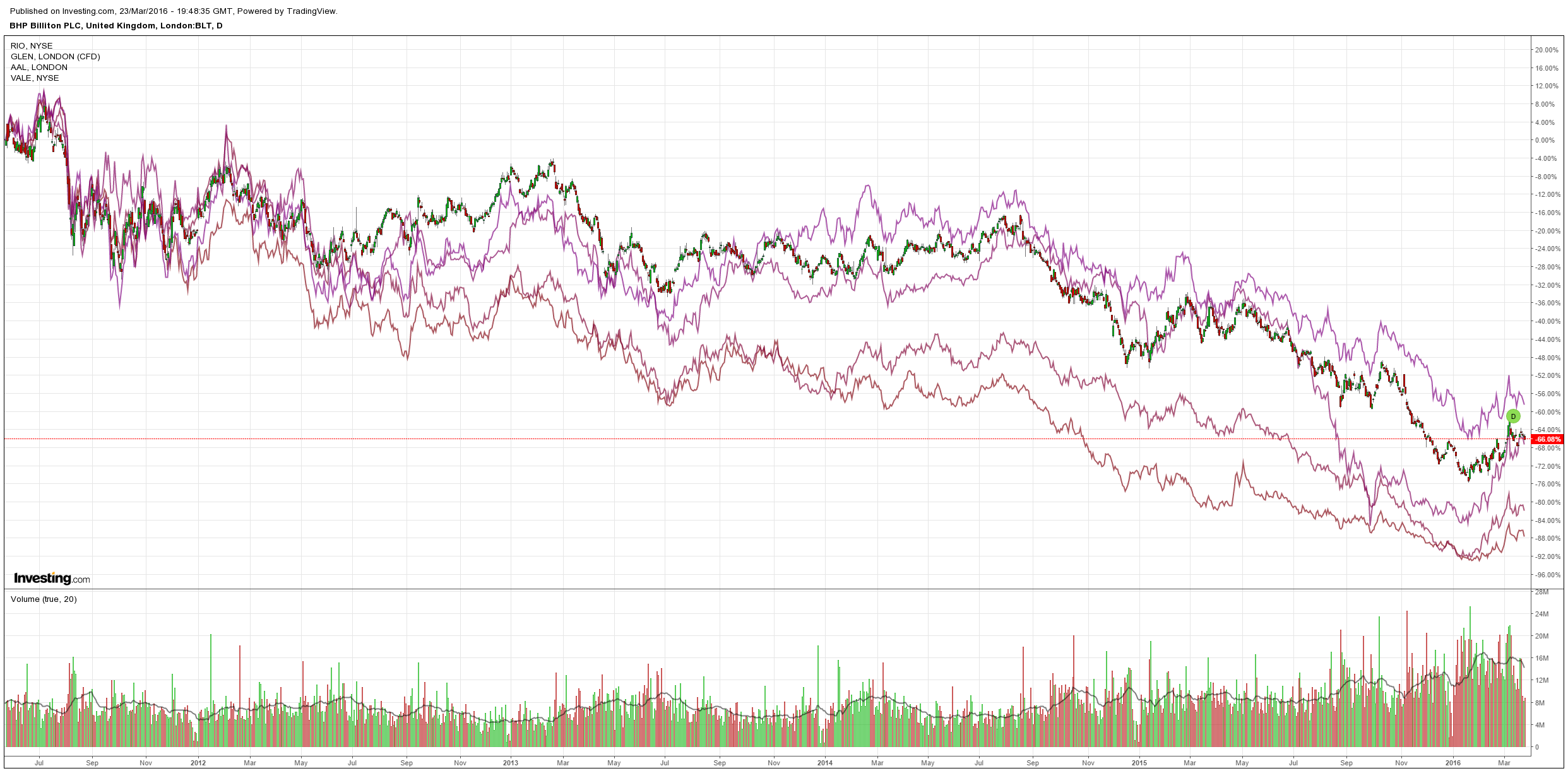

Miners too:

Advertisement

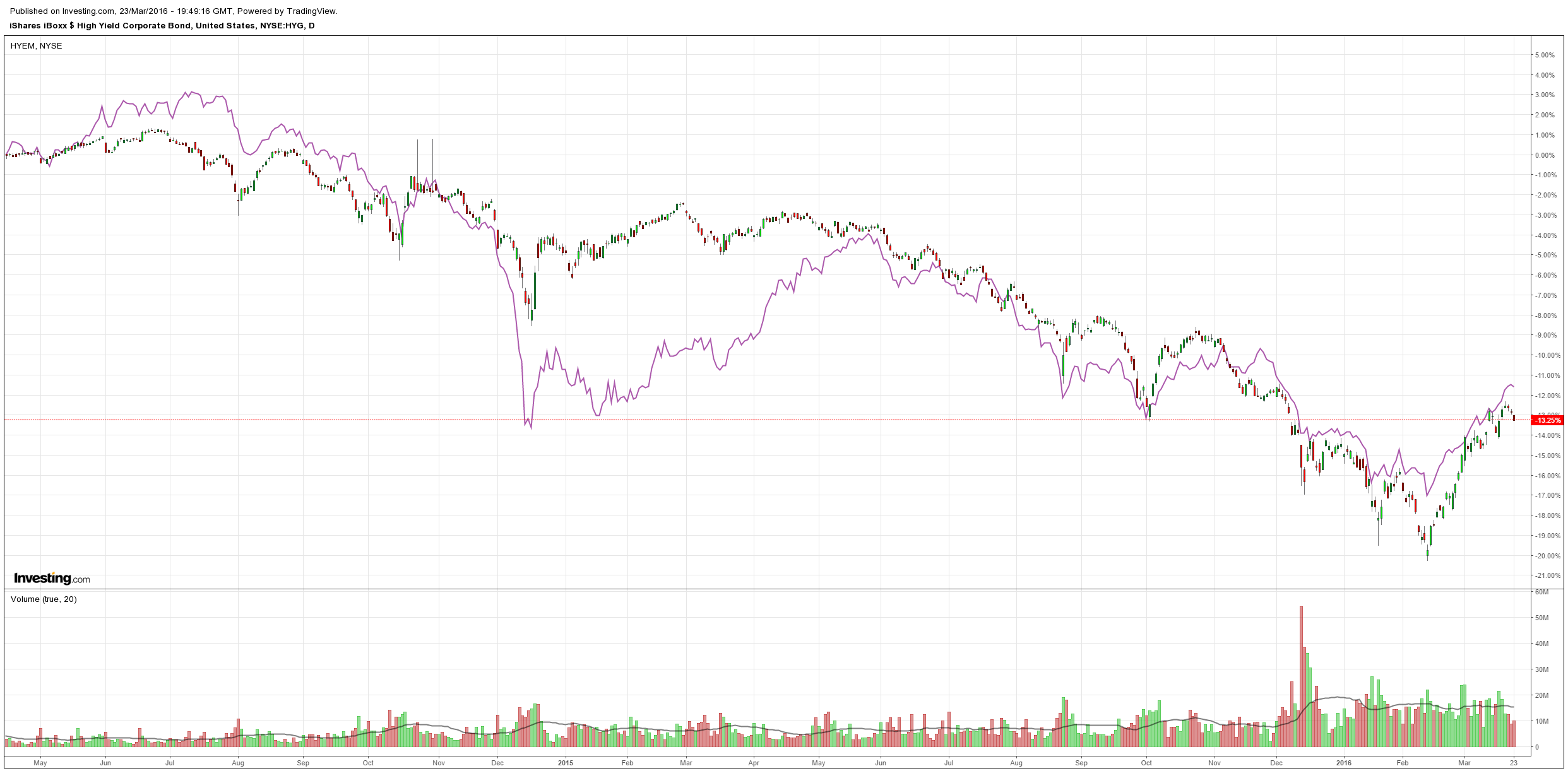

US high yield debt fell again. EM high yield rolled:

We appear much closer to the end of the bear market rally today. UBS joins other major IBs in warning as much:

Advertisement

Last week, we saw the suggested overshooting into expiration and the SPX reached the upper end of our projected late Q1/early Q2 target at 2050, which leaves the short-term picture in the US unchanged as to what we highlighted last week. With the rally of the last few weeks and looking at our daily trend work, the SPX has reached its most overbought position since 2009!! Together with significant non-confirmations in our medium-term momentum work, and trading in the time window of our late Q1/early Q2 top projection, we see the market vulnerable for a significant reversal this week, which we would see as the beginning of a tactical top building process and subsequent correction into deeper Q2. We reiterate our last week’s comment and would not chase the market on current elevated levels.

After being aggressively oversold, we saw the February 11th risk bottom as the basis for a multi-week bear market rally in global equities into the late March/early April timeframe with a price target 2000/2050 in the SPX before starting a new significant tactical down leg into deeper summer. Last week, we said that a final overshooting into expiration is still likely, but particularly in the week after triple witching we very often see important tactical trend reversals in the market.

With last week’s extension, the SPX has reached the upper end of our suggested 2000/2050 late March/early April target range, and with this move the technical in the US has obviously not changed. The February/March rebound was nearly vertical, which is not sustainable. On the indicator side we now have exactly the same setup as in early February but just the other way around.Looking at our daily trend work, we highlighted the US market siting in the most aggressively oversold position since its 2008 panic low and it was one of our key arguments for anticipating a significant and longer lasting rally. With last week’s extension our daily trend work has reached its most overbought position since 2009. Together with our weekly momentum reaching overbought extremes we have a relatively high likelihood of seeing the market move into an important medium-term top followed by a significant setback. Even if our big picture market view (US and global equity markets are in a cyclical bear market that we expect to continue into Q1 2017) proves to be too bearish, with such an indicator setup we should see the US market minimum ahead of a multi-week consolidation pattern, where we should see higher volatility and therefore a significant pullback.

Conclusion: The US market is extremely overbought, and from a cyclical standpoint the SPX is trading in the time window of our late March/early April top projection. In this context, we see the US market vulnerable for a significant reversal this week, which we would see as the beginning of a tactical top building process and subsequent correction into deeper/later Q2. On the upside, the SPX has resistance at 2050 and in case of further overshooting we can see 2075/2080. A re-break below 2024 would be initially negative. A break of 2005 would imply that a more important tactical top is forming. From a cyclical aspect we see an initial pullback into first week April where we expect the SPX to test 2000/1970. We reiterate our last week’s call and would use strength to sell instead of chasing the market on the upside.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific's leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.