The Mining GFC is back as both the commodities bear market and central banks fail. The US dollar was firm heading into the tomorrow’s FOMC meeting:

Commodity currencies were hit hard:

Brent oil rolled:

Advertisement

Base metals too:

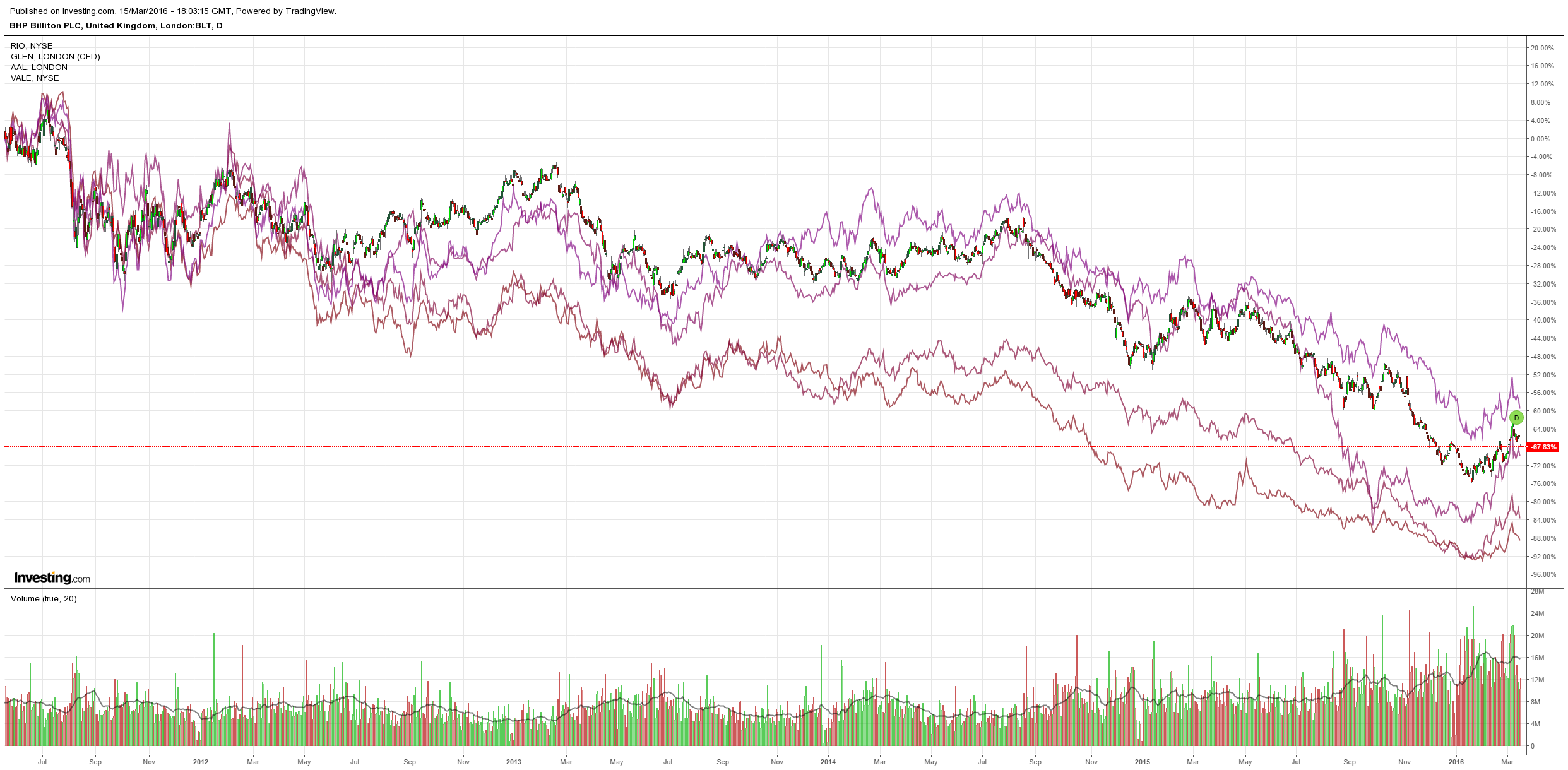

Big miners were thumped:

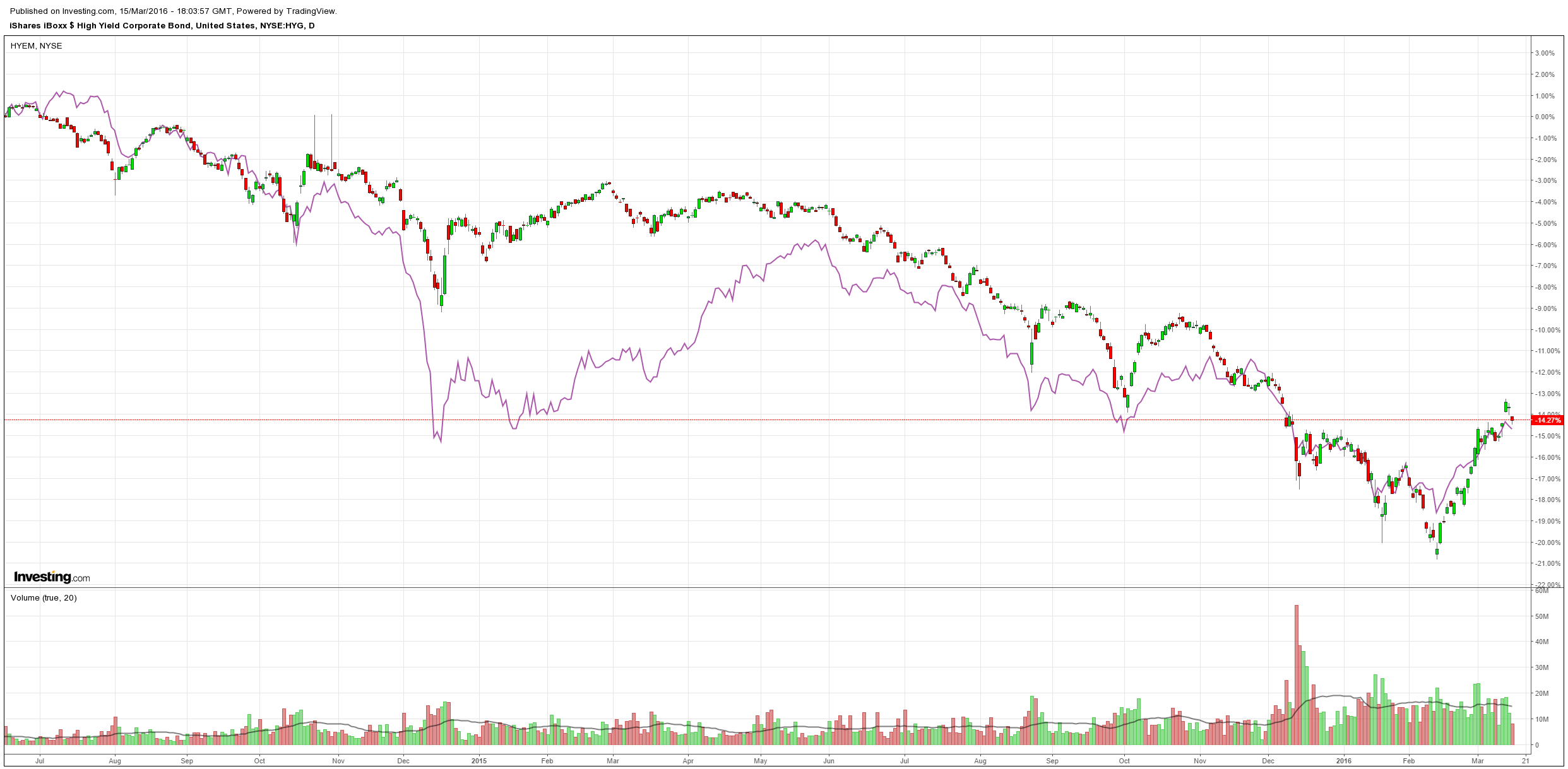

And US/EM high yield gave back much of its break out:

Advertisement

No particular culprit for it. Just the bear market rally getting tired. Though the BOJ did not help, from Reuters:

The Bank of Japan said on Tuesday it would maintain its massive asset buying program at existing levels but offered a bleaker view of the economy, suggesting it may roll out more stimulus as it struggles to reach an elusive inflation target.

However, the central bank appeared to back-pedal on its recent radical shift to negative interest rates, highlighting the dilemma the BOJ faces as it struggles to respond to renewed signs of economic weakness with dwindling policy options.

Six weeks after it shocked global financial markets and alarmed the Japanese public by moving to negative rates, the BOJ dropped a reference in a statement after a policy meeting that it will cut negative rates even more deeply if needed.

The BOJ also widened exemptions to its new negative rate policy to include $90 billion in short-term funds dubbed money-reserve funds (MRFs) after the securities industry warned it could curb investment in the stock market.

“Overall, the impression we get from the BOJ’s latest policy statement is that the central bank is already de-emphasizing negative interest rates as a policy tool, in response to its poor reception by markets and the public,” HSBC said in a research note.

Advertisement

So, negative interest rates make the currency rise and removing them does as well. Smells like quantitative failure alright:

I see little choice for the BOJ other than making its current “massive” asset buying program massiver.

Advertisement

Still, stocks held up in the US, though for a rather unsettling reason, from BofAML:

Last week, during which the S&P 500 climbed 1.1%, BofAML clients were net sellers of US stocks for the seventh consecutive week. Net sales of $3.7bn were the largest since September and led by institutional clients (where net sales by this group were the second-largest in our data history). Hedge funds and private clients were also net sellers, as was the case in each of the prior two weeks, but a different group has led the selling each week. Clients sold stocks across all three size segments, and net sales of mid-caps were notably the largest since June ’09.

Hedge funds have been net sellers on a 4-week average basis since early Feb.

Institutional clients have been net sellers on a 4-week average basis since early Feb.

Private clients have been net sellers of US stocks on a 4-week average basis since early January.

Buybacks by corporate clients accelerated for the third consecutive week to their highest level in six months, which is also above levels at this time last year. This suggests that overall S&P 500 completed buybacks—which are reported with a lag—have likely picked up significantly as well.

Buybacks of Industrials stocks by our corporate clients last week were the largest in our data history, and Materials buybacks were also near record levels. These two sectors, along with Staples, have led the pick-up in overall buybacks in recent weeks.

Yes, that’s right, the only folks buying are the firms themselves, rather than investing in growth. Now that reeks of quantitative failure!

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific's leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.