The Mining GFC was hosed Friday night as credit spreads tightened again. The US dollar was very unconvincingly firmer:

But commodity currencies were on a tear with Brazil especially on fire:

Advertisement

Brent oil is still suffering from congestion:

Base metals are too:

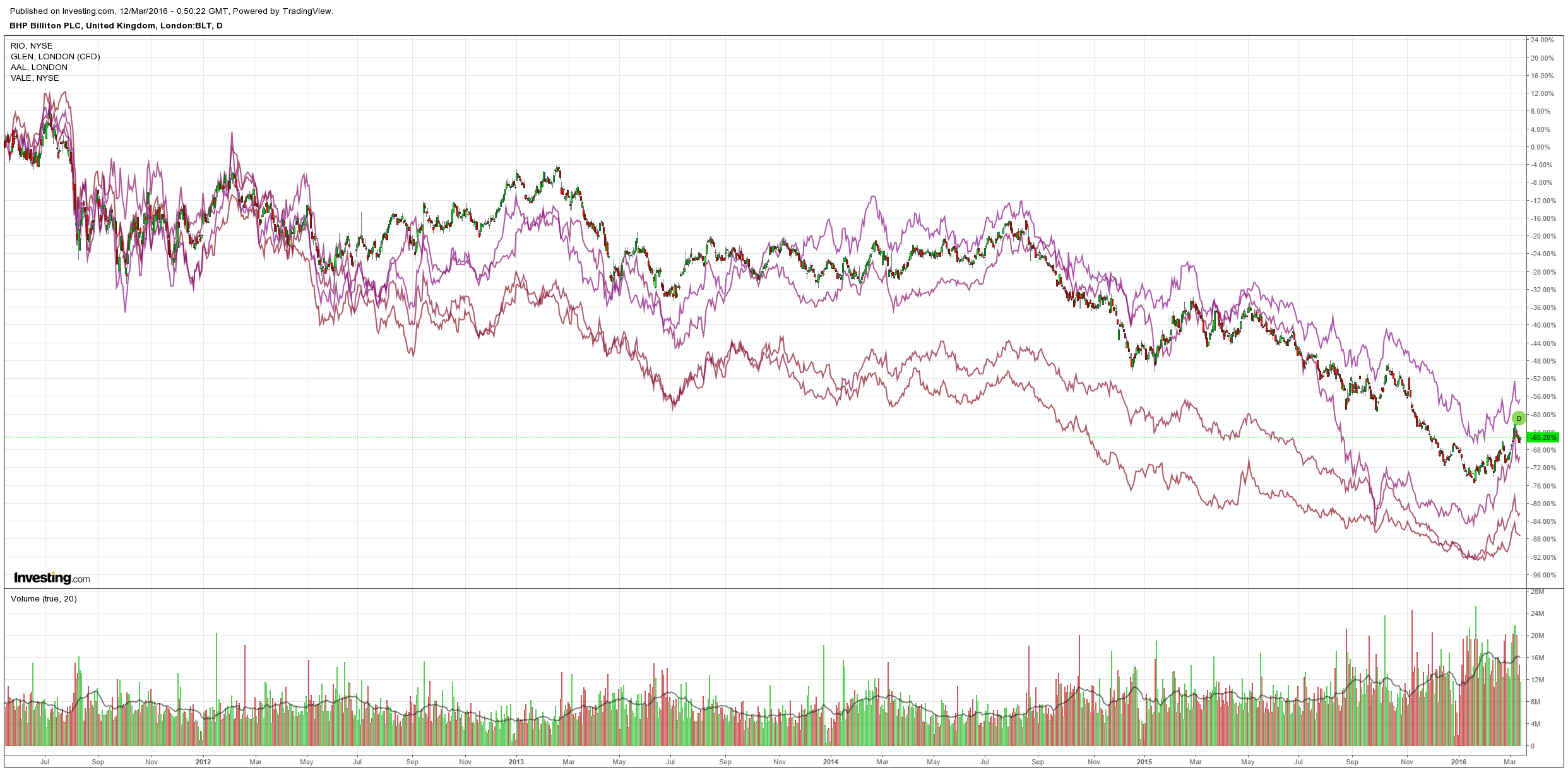

Big miners got a little lift:

Advertisement

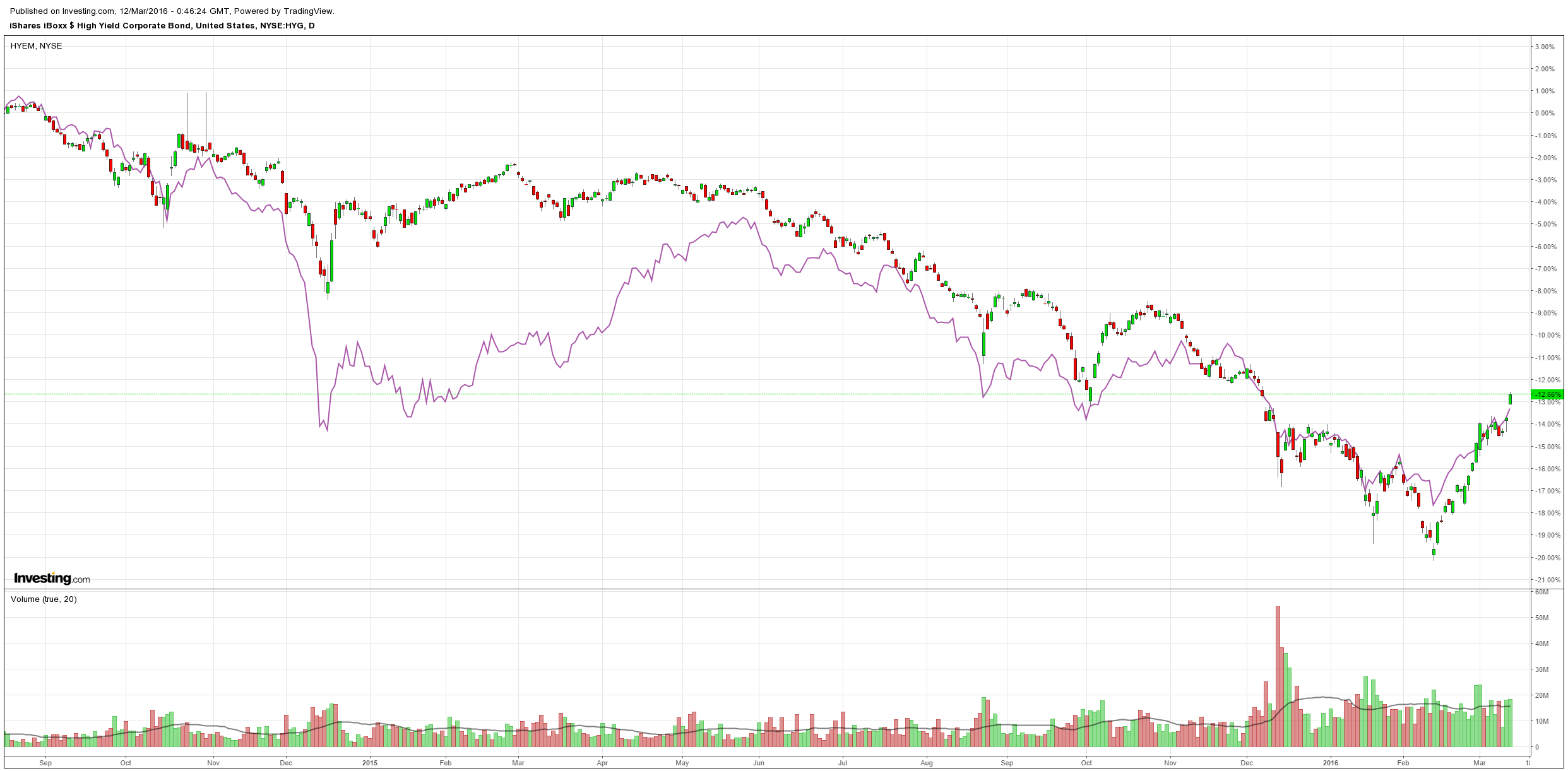

As US/EM high yield ripped higher:

That’s why equities took off again:

The signals are getting more bullish still with Mining GFC whipping boy, Brazil, suddenly going from zero to hero, from the FT:

Advertisement

Meanwhile, Brazilian dollar debt has staged some of the biggest rallies among EM bonds, with yields on its 2017 bond falling by nearly half to 1.7 per cent and those for its 2025 bond dropping by more than 150 basis points to 5.743 per cent.

That despite the fact that Brazil has been downgraded to junk by all three major ratings agencies, or that the country’s once high flying economy is suffering its worst recession in more than a century.

Investors have been willing to overlook all that and more to help the country raise $1.5bn in the global bond market last night. The issue was Brazil’s first sovereign bond sale in 18 months and strong demand – the deal received more than $5bn of orders – allowed bankers to price the bonds at 6.125 per cent, down from the 6.5 per cent that was sought in the initial price guidance.

At the heart of current rally is the growing belief that the end is nearing for President Dilma Rousseff, whose interventionist policies have been blamed for exacerbating the fallout of from the global commodity bust. Ms Rousseff is already facing an impeachment process but last week’s detention and this week’s indictment against Mr da Silva, her mentor and predecessor, is expected to hasten her fall.

With no obvious replacement, analysts have been divided over whether Ms Rousseff’s impeachment is good or bad for Brazil. But investors appear to be increasingly taking the view that a change in government is the only way the country can break its political stalemate and start turning the economy around. The political crisis was one of the factors rating agencies have cited in their recent downgrades.

“What is bad for Dilma now seems to be viewed as good for markets,” observed Neil Shearing, economist at Capital Economics.

However, Mr Shearing warned that investors are probably getting ahead of themselves.

Investors seem to be focusing on the increased chances that the current government might now fall – and overlooking the fact that the country is heading into increasingly choppy political waters…

It’s not clear to us that this is good news for investors…Against this backdrop, the reaction in financial markets looked a little odd…Instead, the best reason to be bullish on Brazilian assets is that they are cheap and that the big falls in global commodity prices are probably behind us. Domestic politics is likely to be a headwind rather than a tailwind over the next year.

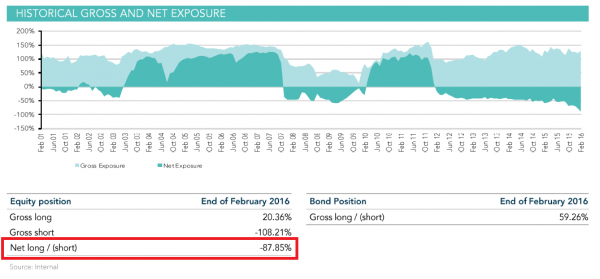

No shit! One of my favourite hedge funds has gone short on the rally:

Your fund made 1.47% net last month mainly on the back of its Japan related positions.

The fund has had a good move from its last drawdown in October of last year, and is probably overdue for a pullback. The first few days of March are bearing this out. However in many ways the drawdown in the fund began in February, as consensus short positions in the market began to rally furiously. Good examples are stocks such as Glencore, which the market was pricing for bankruptcy in January, has now seen its stock price rise 58% year to date. The 10 best performing stocks in the S&P this year, were down last year on average 40%. The reality is no one likes it when loser stocks rally. It makes everyone look bad. Short sellers get crushed, best performing long managers from last year start underperforming the market, and investors wonder why they even bother with active managers!

Sadly, I am all too familiar with markets like these. A significant and surprising move in the market, for example yen strength in February, can cause significant losses in a large macro fund. This macro fund will then seek to reduce risk, and will sell long positions and buy back short positions. This can cause a short counter trend rally, which is painfully, but usually short lived.

My view is that when indices have broken down and are trading as a bear market the best thing to do is to try and reduce the long book as much as possible. There is a strong temptation to find “safe” long positions to own that will reduce the net short position of your fund. I have found this to be the worst possible thing to do as almost every other market participant is trying to crowd into these same safe positions. When the inevitable redemptions come, long positions get sold and short positions get covered, and your “safe” longs end up causing as much damage as your short book.

For that reason over the last year as the bear market has become more and more apparent, I have been continually adding to the short book and selling the long book. I have also been moving the fund to less consensual bearish ideas, such as long yen and short Japanese and European exporters. This strategy has paid dividends in February, which was a very tough month for many other short sellers. The big rally in the yen, helped our currency book, bond book (our JGBs have had a significant move) and short Japanese stocks positions.

I have always felt that having these type of non-consensual trades on are very important as they give you time to observe the market before making a change to the strategy. The equity and commodity markets are sending signals that perhaps the bear market in commodities and the related bear market in emerging markets is over. This however seems very unlikely to me, as many of the indicators for commodity supply are still flashing red, and the issue of excessive capacity has not really been adequately addressed. Big moves in commodity prices could be suggestive of government policies finally becoming effective in creating inflation and above trend growth. However what we are also seeing is a strong yen and falling bond yields, which is not consistent with accelerating growth or inflation.

More likely the yen rally in February has been extremely painful for a number of large macro funds, and has caused these funds to cut risk from the long and short book, which given consensual positioning in markets is causing a great deal more pain. If history is a guide, I would assume that we are nearly through this mean reversion trade.

Your fund remains short equities, long bonds.

Advertisement

That looks spot on to me. However, this is all being driven by oil and it still looks very firm. I’ve been writing for a while that the oil market appears to be running another stress test for US shale and could run as high as it needs to to see it stabilise before falling again. That is also the significance of the ongoing high yield debt recovery given it controls US shale output through funding its perpetual capital needs. The market is sniffing out the marginal cost of production in the new oil order and until it finds it I suspect the bear market rally remains biased upwards.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific's leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.