At today’s meeting the Governing Council of the ECB took the following monetary policy decisions:

(1) The interest rate on the main refinancing operations of the Eurosystem will be decreased by 5 basis points to 0.00%, starting from the operation to be settled on 16 March 2016.

(2) The interest rate on the marginal lending facility will be decreased by 5 basis points to 0.25%, with effect from 16 March 2016.

(3) The interest rate on the deposit facility will be decreased by 10 basis points to -0.40%, with effect from 16 March 2016.

(4) The monthly purchases under the asset purchase programme will be expanded to €80 billion starting in April.

(5) Investment grade euro-denominated bonds issued by non-bank corporations established in the euro area will be included in the list of assets that are eligible for regular purchases.

(6) A new series of four targeted longer-term refinancing operations (TLTRO II), each with a maturity of four years, will be launched, starting in June 2016. Borrowing conditions in these operations can be as low as the interest rate on the deposit facility.

The President of the ECB will comment on the considerations underlying these decisions at a press conference starting at 14:30 CET today.

Much of that was ahead of expectations but still the euro rose and the US dollar fell sharply after a spike:

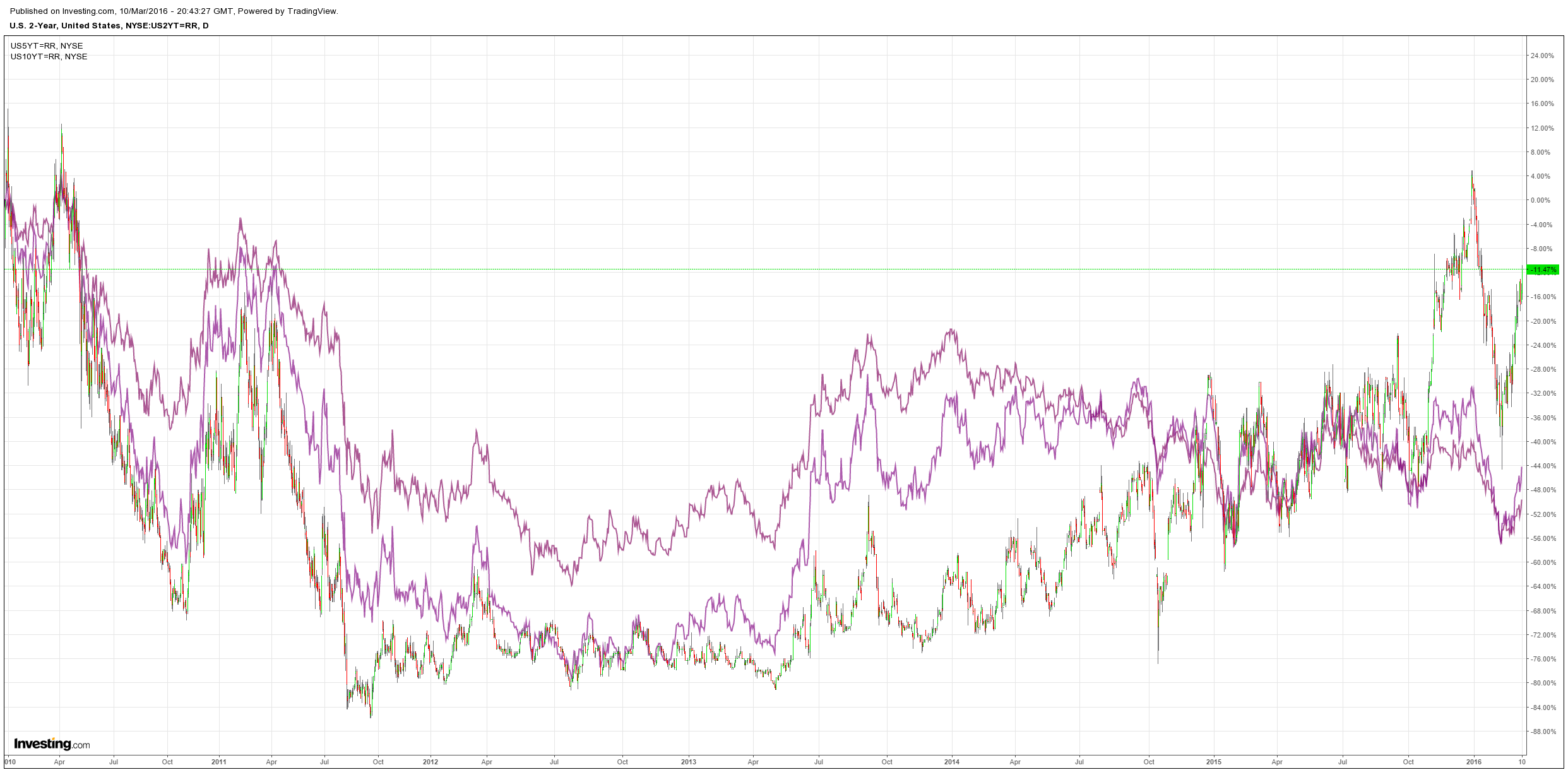

Contradicting that, US yields rose, stocks were sold but finished flat:

Advertisement

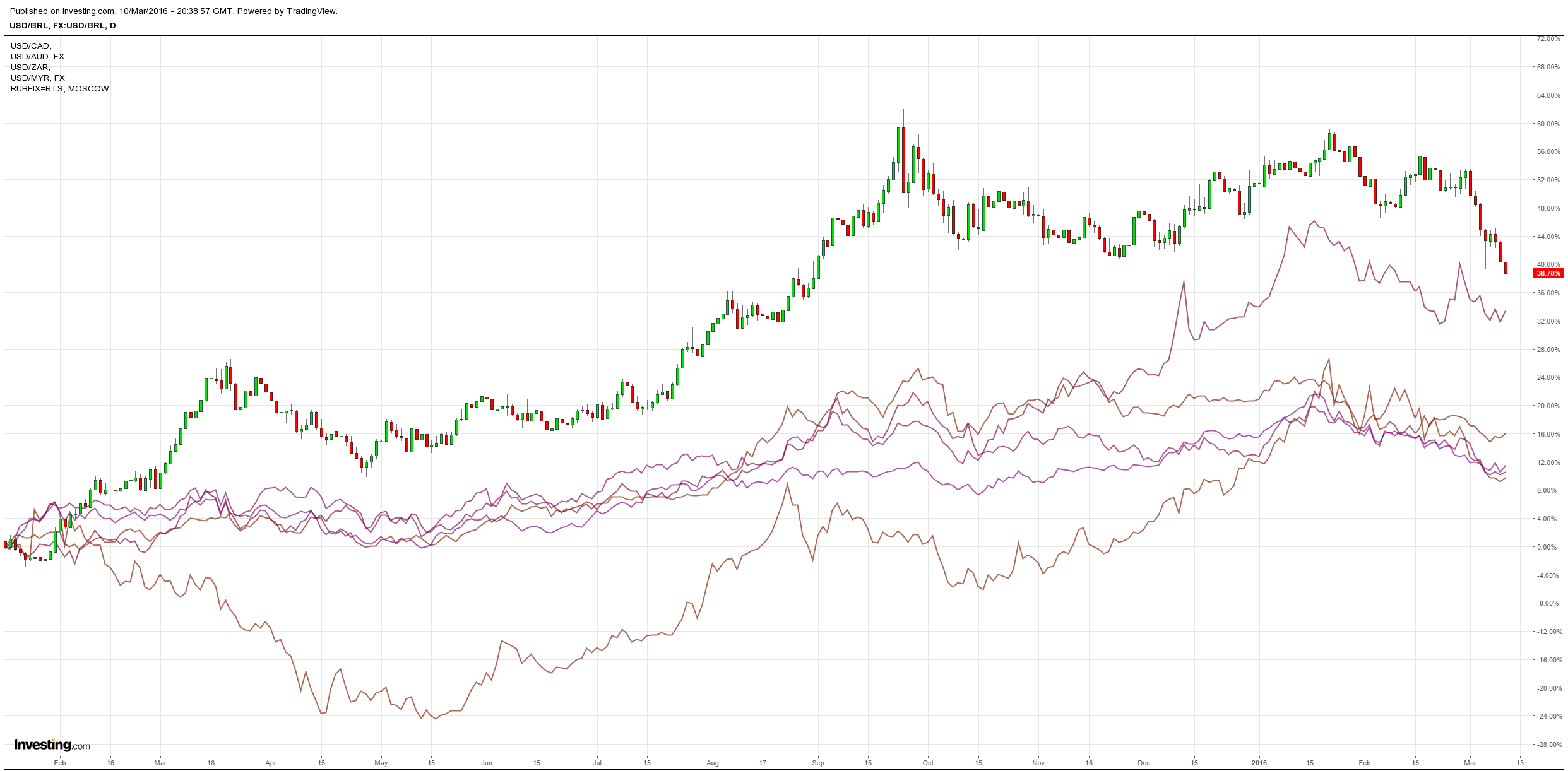

And commodity currencies fell anyway:

As did oil though it remains firm:

Advertisement

And base metals pulled back as well:

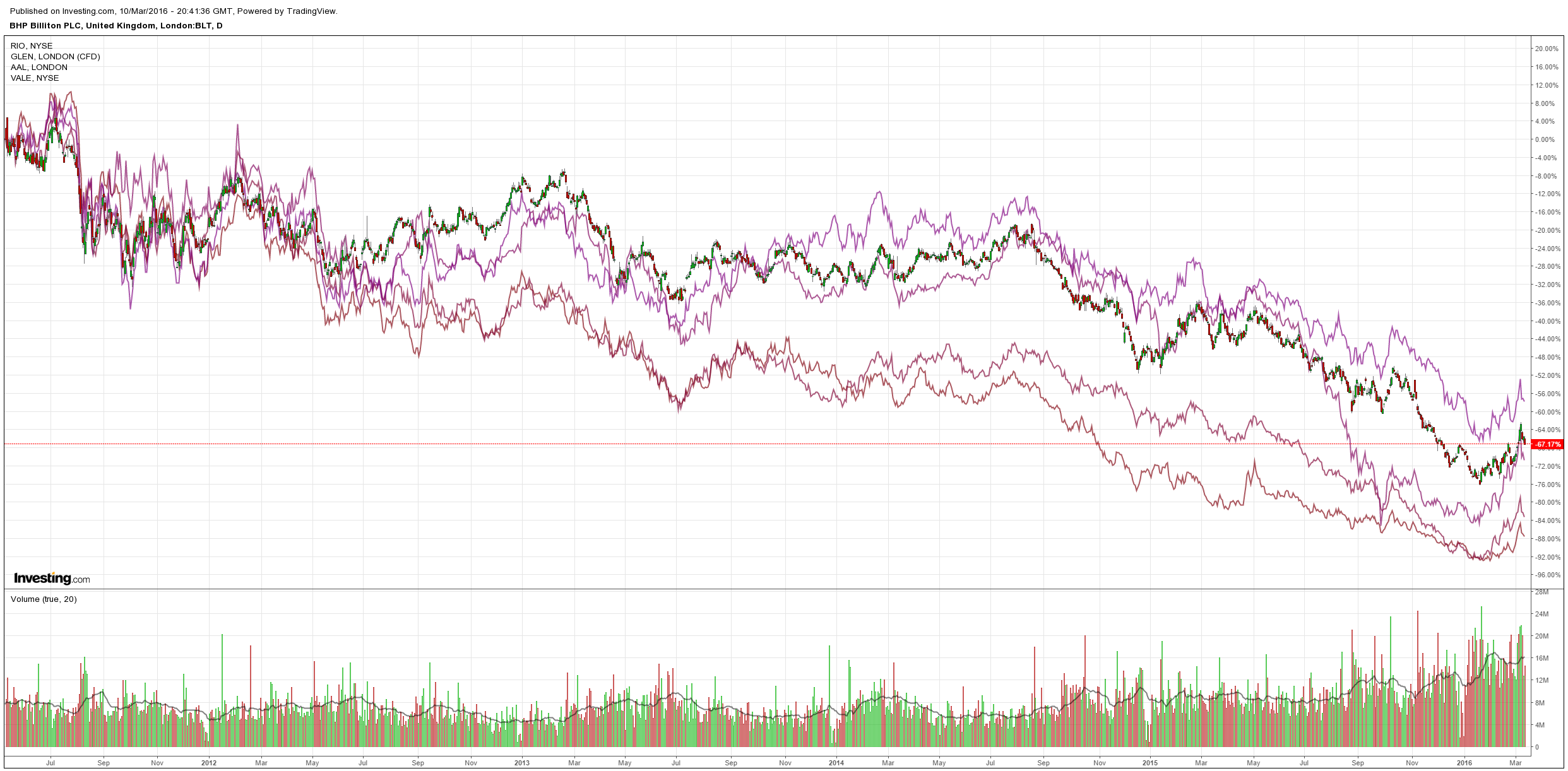

Miners were hammered:

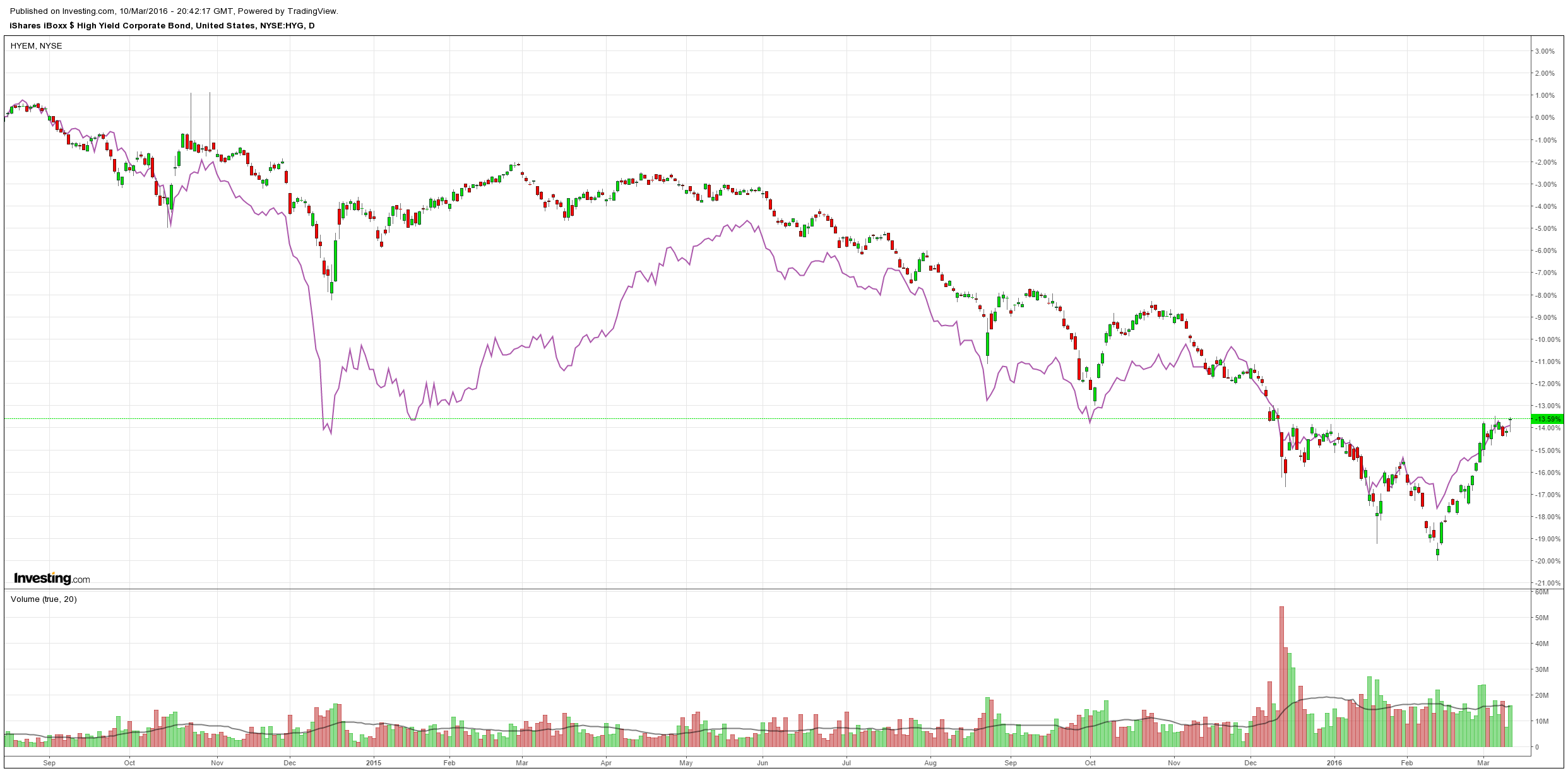

But US high yield broke out:

Advertisement

Quite a few mixed messages there. I would say the following:

the ECB was up against it given sky high expectations;

there is definitely selling in the US dollar as we wait for the Fed;

commodities and shares are trading purely on oil and it appears to have further to rally with the buying in high yield credit firming up again.

Goldman sees an end to the bear market rally:

Advertisement

We make no changes to our asset allocation at this stage as the relief rally has been too fast, in our view. We still do not feel comfortable taking more risk in equities until valuation or growth becomes more attractive. Although we believe the market has been too pessimistic, we think a key driver of the relief has been higher oil prices. With oil at the upper end of our commodities team’s forecast range for 1H 2016, it could drive further volatility as we do not believe oil weakness is necessarily over. We still believe credit remains attractive, particularly in Europe, where further ECB easing and good credit fundamentals remain supportive. Although US high yield has rallied recently, over the near term we remain Neutral US HY within credit. Despite seeing fundamental value in US HY spread levels, downside risk to oil makes us tactically cautious (see Global Markets Daily: Oil and HY redux, March 8, 2016). We remain Underweight bonds given the relatively low level of yields, potential for reflation, and our economists’ expectation that the Fed rate hike cycle continues in June. We retain our relative preference for German Bunds over US Treasuries as policy divergence should play out over the coming months and drive the Treasury-Bund rate differential significantly wider.

Volatility potential in a central bank filled month…should not be too unfamiliar given past moves

The ECB meets this Thursday (March 10), with the BoJ and Fed meeting next week…. Measuring how frequent extreme asset price movements have been in the past, the figure on the left below plots the average number of days over the prior 12 months with return moves (positive or negative) of 3 standard deviations or more by asset class, using rolling 1-year standard deviations. Since 1986, no period besides 2008-09 has had a larger number of relatively extreme asset price movements than we have experienced recently. This has been particularly true for the 10-year government bond and FX markets.

The figure on the right breaks down extreme movements by region by taking averages of 3-SD return days in Europe and the US across equity, 10y bonds, and IG and HY credit. We find that, of late, large asset price movements in Europe have become more prevalent than in the US, which is somewhat unsurprising given the higher volatility of those markets. EUR/USD has seen significant movements around the period of QE (both in the US and Europe) as policy drove near-term rate differentials and currency moves.

Notably, assets moving from a low- to high-vol regime are most likely to have a large number of 3-SD return days, as relatively extreme movements are easier to achieve when trailing vol is low, but these extreme days then contribute to raising realized vol. Thus, a decrease in a large number of 3-SD return days may actually signal a transition has occurred from a low- to a higher-volatility regime. We believe we will remain in a high-volatility regime, with no particular asset being immune, until a combination of policy, oil prices and growth stabilise.

But it seems pretty clear to me that it is not going to end until oil rolls over.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific's leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.