Thanks Fed! Everything dirt ripped overnight as the US dollar took it in the team and appears headed for 93 cents retest:

Gold roared but did not break out suggesting lingering US dollar strength:

Advertisement

Nor did US short end yields fall further and they are nowhere near the correction we saw during the January crash also suggesting any decent push lower in the US dollar will be bought:

Commodity currencies launched:

Advertisement

Brent broke out:

Base metals surged and copper broke out (iron ore futures also went nuts):

Advertisement

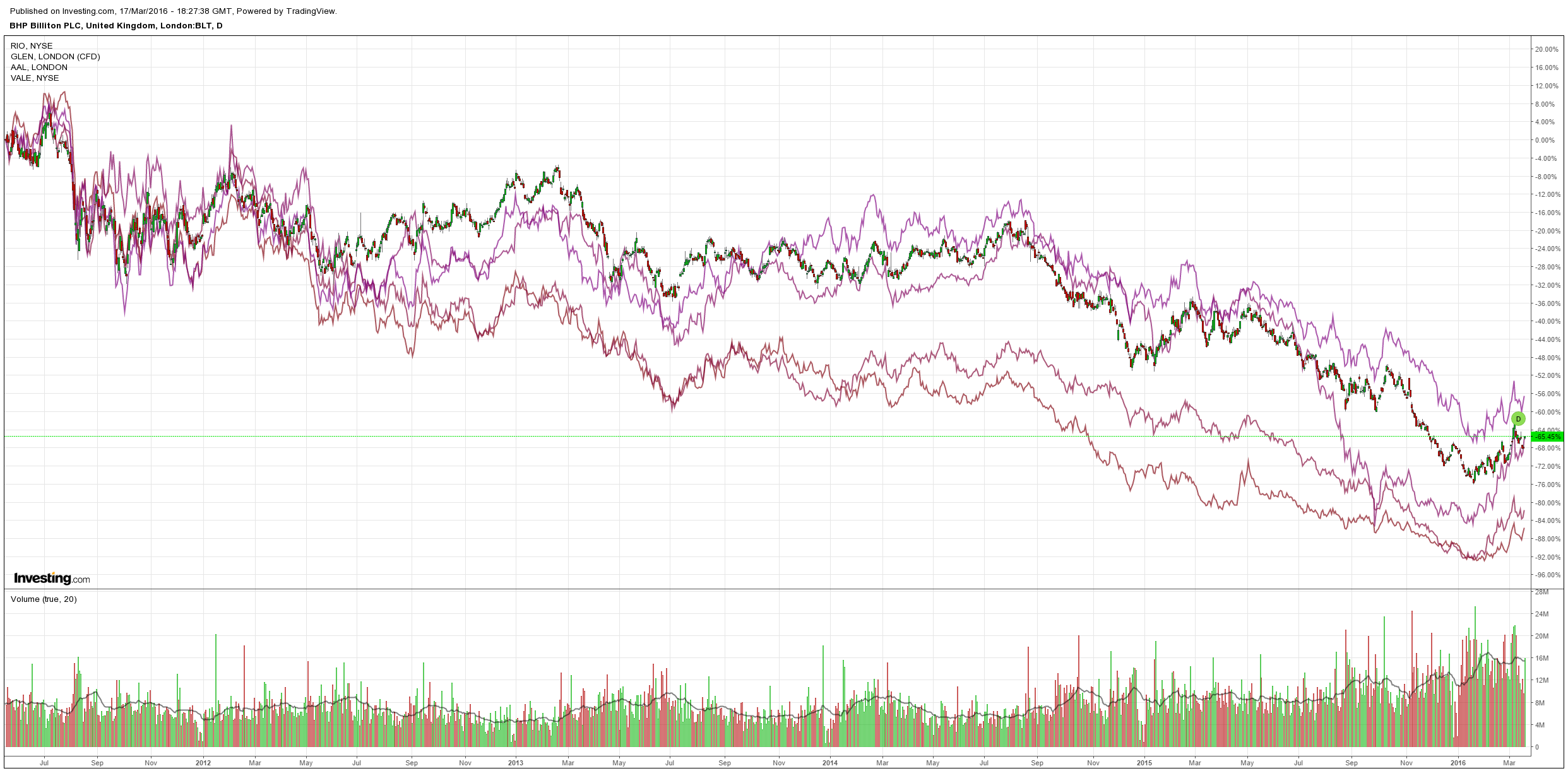

Miners surged again but are not at new highs:

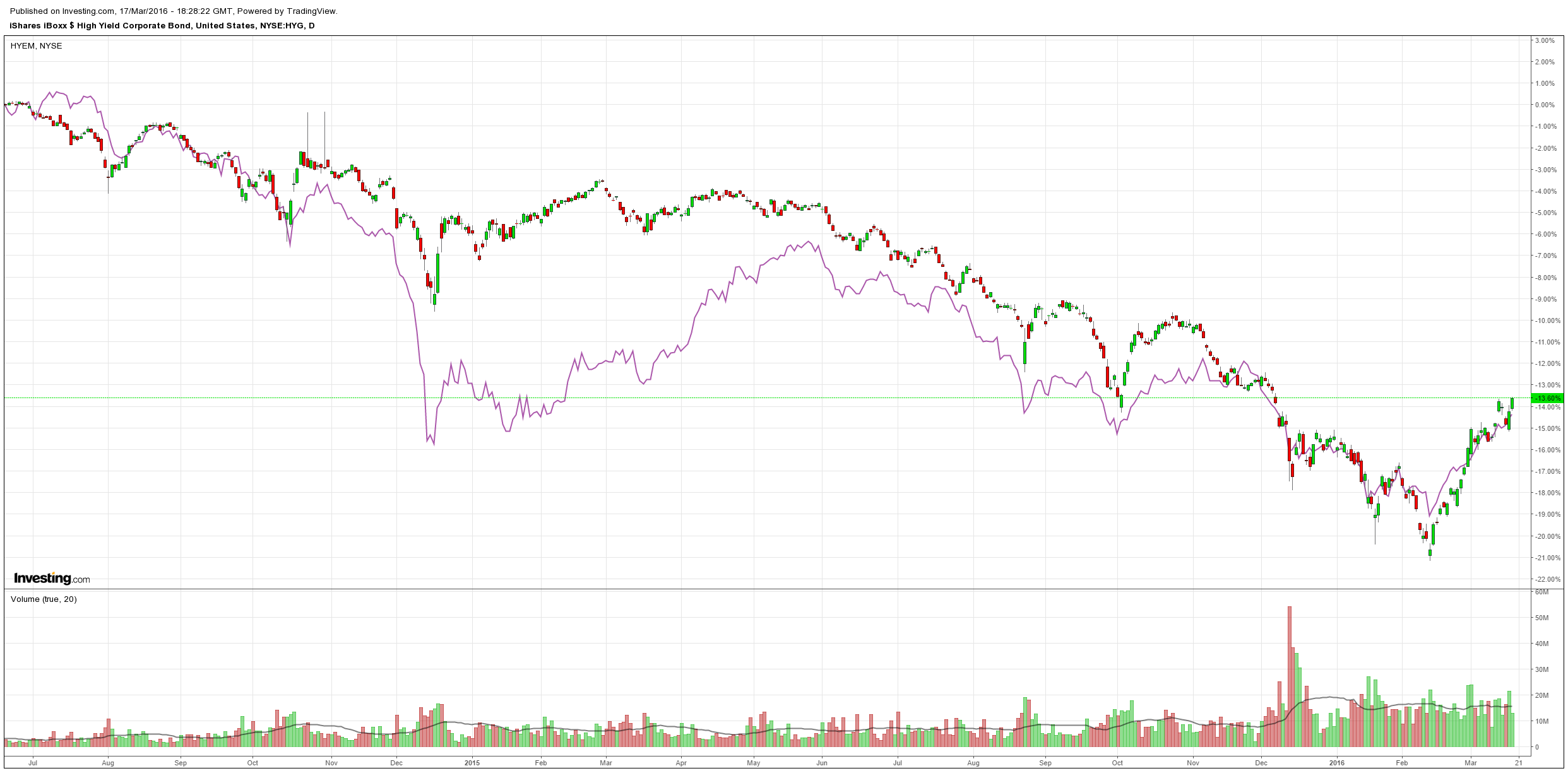

US/EM high yield also surged:

BofAML remains bearish on credit:

Advertisement

We also believe it is telling that bank stocks moved significantly lower after the rate decision. Though the price action in banks makes sense – a lower for longer rate environment and slower economic growth is not a positive scenario for financials – typically the moves in bank equity and high yield spreads are very well correlated (-48%). In our view the challenging bank environment is a canary in the coal mine for high yield. As financial volatility increases, bank earnings decline, and unease about the global economy heightens, banks pull back on risk and lending. Note the latest Fed survey on lending standards as a prime example of declining risk tolerance of loan officers.

Given the apparently weaker consumer (retail sales, nonmanufacturing ISM), the poor Q4 earnings season, and problems abroad, the acknowledgment by Chair Yellen of stresses in financial markets creating tighter financial conditions should have created renewed fears of a growth slowdown in the US, in our view. In fact, the last 2 times the Fed indicated global risks to the domestic economy, while holding rates steady, were at the September meeting and January meeting. And in both cases HYG declined 4.5% and 4% over the next 13 days (Chart 1). Although we don’t know if the same reaction will occur after this meeting, we are convinced that our bearish view on high yield continues to hold merit.

With defaults picking up in the commodity space, incredible stress in some individual non-commodity high yield issuers, a wave of downgrades looming and now the Fed’s revisions to near-term forecasts,we wonder how long asset allocators will continue to ignore both the weak macro as well as poor micro credit environment and feed money into high yield. Chair Yellen told us today that inflation is likely to remain weak and dollar strength will continue to cause headwinds. This latter admission is particularly interesting to us. If a strong dollar persists in 2016 corporate earnings hurt by FX exposure are unlikely to improve meaningfully. Couple this dynamic with ever increasing write offs and impairment charges (even ex-Energy) and the recent rally looks to have limited staying power in our view.

I agree, but the market is still positioned long the US dollar so that’s going to wash out some first. Moreover, oil is the key driver and the argument that we’ll need to see US shale stabilise before it rolls over again is still live. The rally in credit is a part of that given its key role in funding shale’s perpetual capital needs.

For perspective on this rally remember that markets are now roughly where they were when we penned our Xmas special report Australia and the 100 year bustin which we forecast stuff such as this. It’s been an exciting round trip of market then central bank panic but the underlying structure of a weakening China and yuan and strengthening US and dollar remains intact. Until that changes, the Mining GFC rolls on.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific's leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.