The Mining GFC is simmering on the back-burner as markets chew threw their recent excesses. The US dollar was flat overnight:

Commodity currencies were largely weak:

Brent oil was flat:

Advertisement

Base metals were mixed:

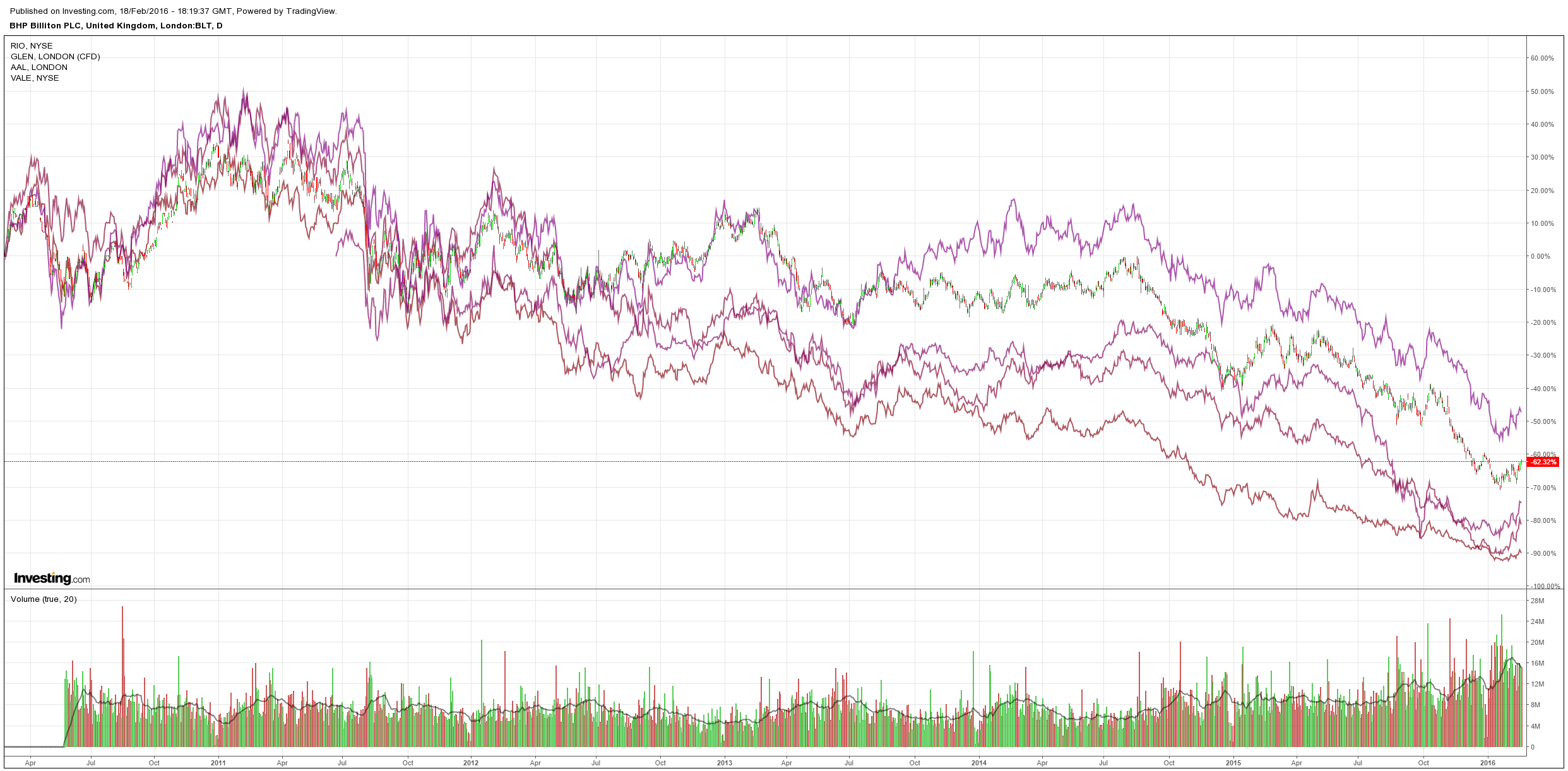

Big miners eased back after the big breakout:

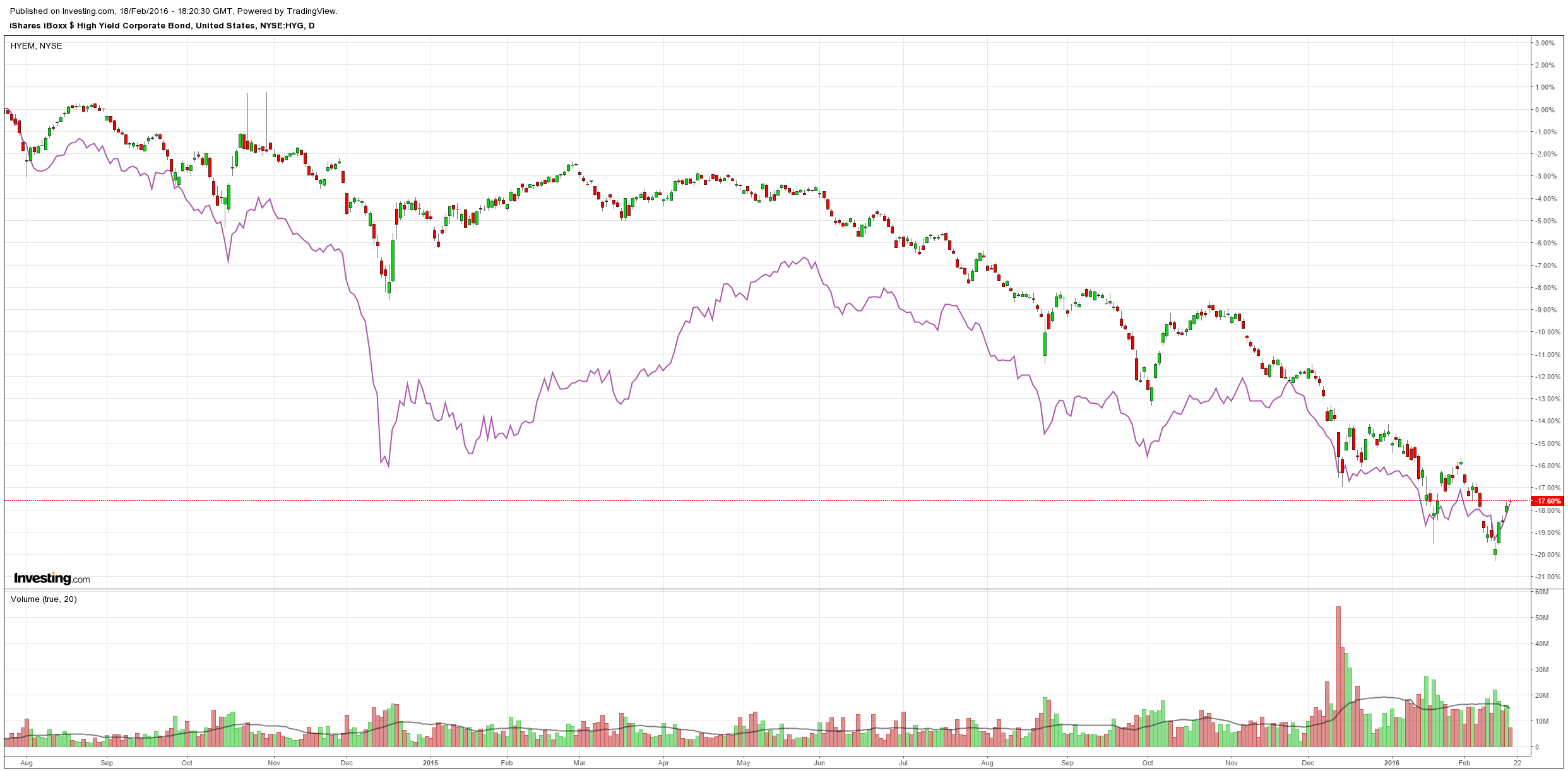

And US as well as EM high yield debt was bought but at a slowing pace:

Advertisement

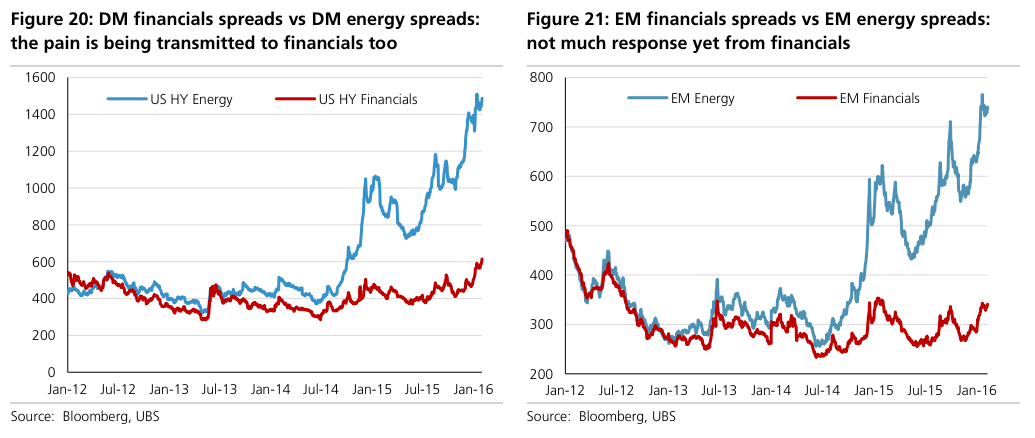

Today’s add-on comes from UBS which nails the core of the problem going forward in my view:

You know that the sovereign is really under pressure when weakness in nonfinancial corporates begins to infect financials. That’s when systemic risks to the economy rise and the government cheque book must come out, especially in a complex like EM, with several publicly owned banks.

This hasn’t happened yet. Financials spreads are widening but not nearly to the same degree as are energy spreads or financials in DM…

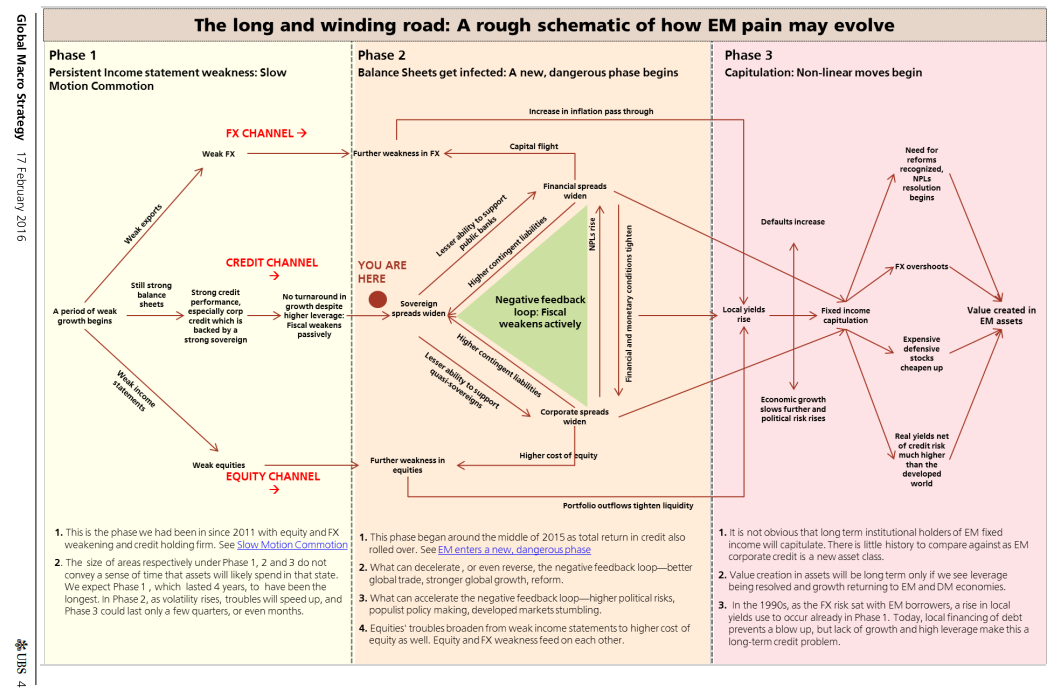

1. High government ownership in key sectors such as oil and gas, and financials will likely keep EM corporate credit from weakening as dramatically as that seen in US HY near term.

2. However, weak earnings, negative credit impulse, and tightening primary markets will likely hit EM corporates with a lag. Corporate fundamentals will hurt the sovereign that is backstopping them just as the sovereign’s fiscal credentials are already being questioned, leading to higher spreads and higher local yields. This should mean that the problems of one sector infect the broader economy in EM much more than it has in the US.

3. A widening of sovereign spreads and higher local yields should broaden the pain across the corporate spectrum, hurting stocks including those in strong sectors through a higher cost of equity. The link between credit spreads and equities is much stronger in EM than in DM, notwithstanding recent price action in the developed world.

4. A widening of EM financial spreads will be a key sign of contagion from corporates to the sovereign. This was the case in Europe too, except it is difficult to see an effective backstop like the ECB or Fed in EM. A negative loop between financials, sovereigns and corporates may be set in motion. This can eventually lead to fixed income capitulation, and value creation.

5. In 2016, we expect EM corporate credits to widen further by around 70- 100 bps, underperforming both EM sovereigns and US HY. This is consistent with EM equities dropping 10-12%.

I totally agree except with the equities forecast. The kind of contagion described here is a full blown -40% fall and end of cycle event.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.