Commodity currencies were weak anyway though not the Aussie:

Brent oil fell sharply then rebounded and stocks tracked it perfectly:

Advertisement

Most base metals fell:

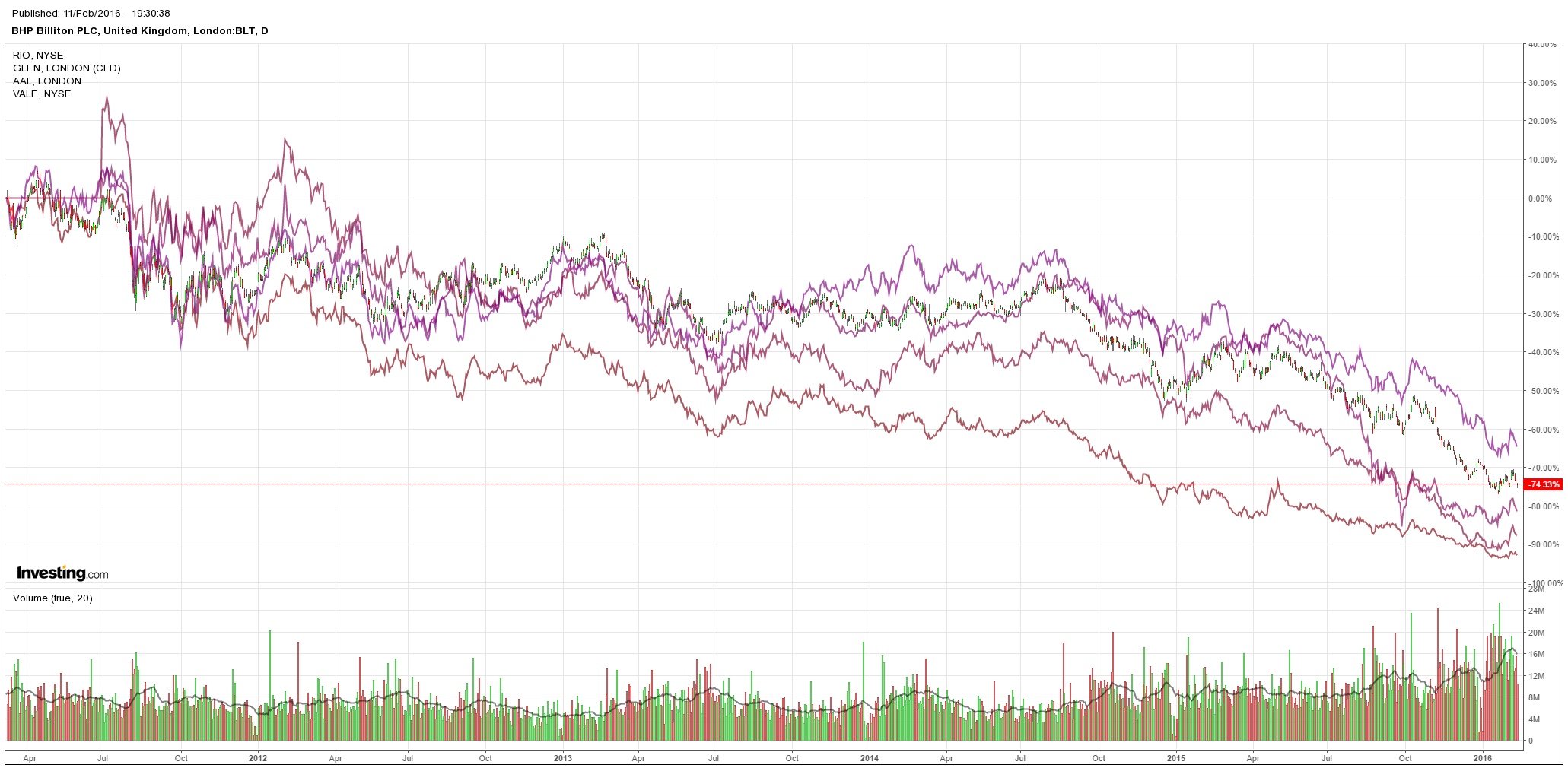

Miners were crushed again:

US and EM high yield debt tanked to new lows:

Advertisement

But the biggest mover on the night was gold, roaring 5%:

Advertisement

One reason is a weaker US dollar and growing expectations of no more US rate hikes if not stimulus. US bonds are rapidly pricing out all future hikes:

But another reason for the gold spike appears to be that markets are genuinely shaken by central bank failure. From Bloomberg:

Advertisement

Central banks are running into diminishing returns from their use of easy monetary policies, seven years after first championing quantitative easing to save the world from depression.

The new reality is clear across global financial markets: The Standard & Poor’s 500 Index reached a 22-month low in the U.S. Tuesday, and Japan’s benchmark equity index careened on toward levels unseen since 2014, while the yield on the country’s 10-year bonds dipped below zero for the first time. Stocks also slid in Europe, where memories of the region’s debt crisis are being stirred by rising bond yields in Portugal and a slide in Greek banks.

All that despite the Bank of Japan’s surprise shift to negative interest rates, the European Central Bank’s signal it will deploy new stimulus next month and speculation the Federal Reserve will slow its campaign to raise interest rates. Underscoring the lack of policy potency is that the yen and euro are both climbing even as policy eases.

“The markets are wondering, well, we’ve had these non-conventional monetary policy experiments for the last six or seven years and they haven’t caused a sustainable boost to global growth, so what will the latest moves do,” said Shane Oliver, head of investment strategy at Sydney-based AMP Capital Investors Ltd. “It’s a reasonable question to ask given the events of the last few weeks.”

We know that Japanese NIRP has backfired spectacularly as stocks fall and the currency rockets, but that didn’t stop the Swedish Riksbank from cutting deeper into the negative last night. ADM Investor Services sums that up:

The Swedish rate decision was seen as being finely balanced, and then the Riksbank cut more than expected (-15 bps to -0.50%), clearly anticipating (or at least this is how it will be seen) an aggressive March ECB move, this looks to be rather desperate, clearly designed to offset rise in SEK vs. USD, and weaken SEK vfs. EUR. But the real story of today is USD/JPY – a colossal pain trade which may just trigger a genuine capitulation trade, as some in markets may wonder what is it that the central banks know that they are not telling us, given such an “aggressive” easing move. The answer is probably nothing, but it is a reminder that more easing now may no long be seen as ‘moar stimulus’, but rather as a signal that the wheels may be falling off…

Advertisement

JPM assessed how far the loonies might push it:

Switzerland and Denmark have been in the vanguard of the recent move to negative interest rates, with Sweden, the Euro area, and (most recently) Japan following. In both the Swiss and Danish cases, the initial shift to NIRP came alongside efforts to mitigate strength in their currencies. As both central banks sold large amounts of their currency into the market, the reserve balances of their domestic banks grew rapidly. With the prospective costs of NIRP to the domestic banks rising, the amount of reserves they could hold that was exempt from the negative interest rate was raised. There are a number of features of these experiences worth highlighting:

The negative policy rate has been passed through to shortterm market and wholesale interest rates, without any systematic signs of rising volatility in those rates (Figure 3).

The amount of the reserve stock subject to the negative rate has varied significantly, between 40% and 95% in the Danish case, while 20-30% has been typical in the Swiss case. But, in all cases money markets have continued to function adequately.

The direct costs imposed on banks by the negative regime have been small when compared to the size of the balance sheet as a whole. In Denmark, we calculate that the peak annualized interest charge has been just 0.00006% of total assets. In Switzerland, the peak charge has been 0.03% of total assets.

Any pressure on bank profitability from NIRP does not appear to have expressed itself in tightening in credit availability in the instances considered here: the dominant trend toward easier credit conditions has remained in place.

There have been few meaningful signs that banks or others have hoarded physical cash in order to avoid the negative interest charge (Figures 4 and 5).

This last observation is important. One way of explaining it is that there are significant fixed costs involved in banks holding large amounts of cash in preference to reserves. The systems to decide the reserves-cash split, to warehouse, transport and insure the cash, need to be put in place, and likely have a significant element of set-up cost. It would appear that central banks have been able to keep the costs of negative interest rates below that set-up cost, in particular by introducing exemptions to them as policy rates have fallen. As a result, banks have not felt it worth their while to put in place the systems to hold more cash.

…As already noted, it is in Switzerland that these costs have been highest at 0.03% of total assets. Given that this cost did not trigger significant increases in cash holding in Switzerland, it may be helpful to use that as a benchmark elsewhere… (there are caveats in the usual place, including the fact that “the Swiss exemptions from negative rates were crafted so that the costs fell disproportionately on foreign banks operating in Switzerland” and it all depends on perceptions about how long negative rates will stay in place)

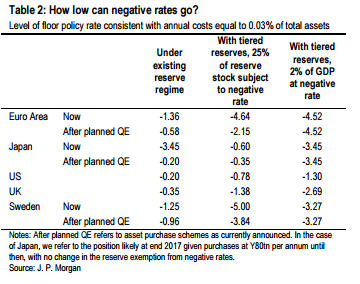

Table 2 below calculates levels of negative rates that would be consistent with their direct cost to banks not exceeding 0.03% of banks total assets. On the basis of the reserve regimes that are currently in place, this exercise suggests rates could plausibly be reduced to -1% or below in the Euro area, Japan, and Sweden. In the US and UK, there is less scope to move rates below zero while respecting the cost constraint. This reflects the fact that the reserve stock is already large relative to bank assets in these countries, and the vast majority of the reserve stock would be subject to the negative rate under the current regime.

In the Euro area, Japan and Sweden, the stock of reserves is being boosted by ongoing QE programs. As the stock of reserve grows, all else equal, the cost to the banks of the negative rate policy rises. Hence the table also shows where policy rates could be reduced to while respecting the 0.03% cost constraint given the QE programs as already announced. On this basis, the scope for negative rates becomes more constrained.

Of course there is no reason to expect that reserve regimes would be static as central banks implement negative rates. Hence the table also reports calculations given the two variants of tiered-reserve regimes discussed earlier. And as the table demonstrates, implementing a tiered reserve regime can conceivably open up significantly more scope to implement negative rates. With reserves worth 2% of GDP subject to the negative deposit rate , we calculate that the policy rate could be moved below -1% in the US, below -2% in the UK, and below -3% elsewhere while still keeping the direct costs of the regime below these seen in Switzerland.

…Having put in place a three tiered deposit system and facing a significant inflation undershoot, we expect the Bank of Japan to move further into NIRP this year. We look for rates to fall to -0.5% alongside additional QQE.

With inflation continuing to run well below its objective, and with significant downside risks to both growth and inflation, we expect the ECB will take the deposit rate down to -0.70% and will introduce tiering of reserve charging along the way.

With IOER at +0.5% and the Fed maintaining concerns about US money markets, the US is not close to considering NIRP. However, if recession risks were realized, the need for substantial additional policy would likely push the Fed towards NIRP.

Janet Yellen confessed they too are considering NIRP:

Let’s hope they have the sense to say no when it comes to that. As William White said yesterday it’s a mad experiment. Judging by the Japenese experience to date, if the US does it too then gold is going to the moon, banks and share markets are going down and currencies will descend into outright war.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific's leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.