The Mining GFC erupted again last night. The US dollar was soft:

But commodity currencies softer:

Oil tanked:

But base metals held up:

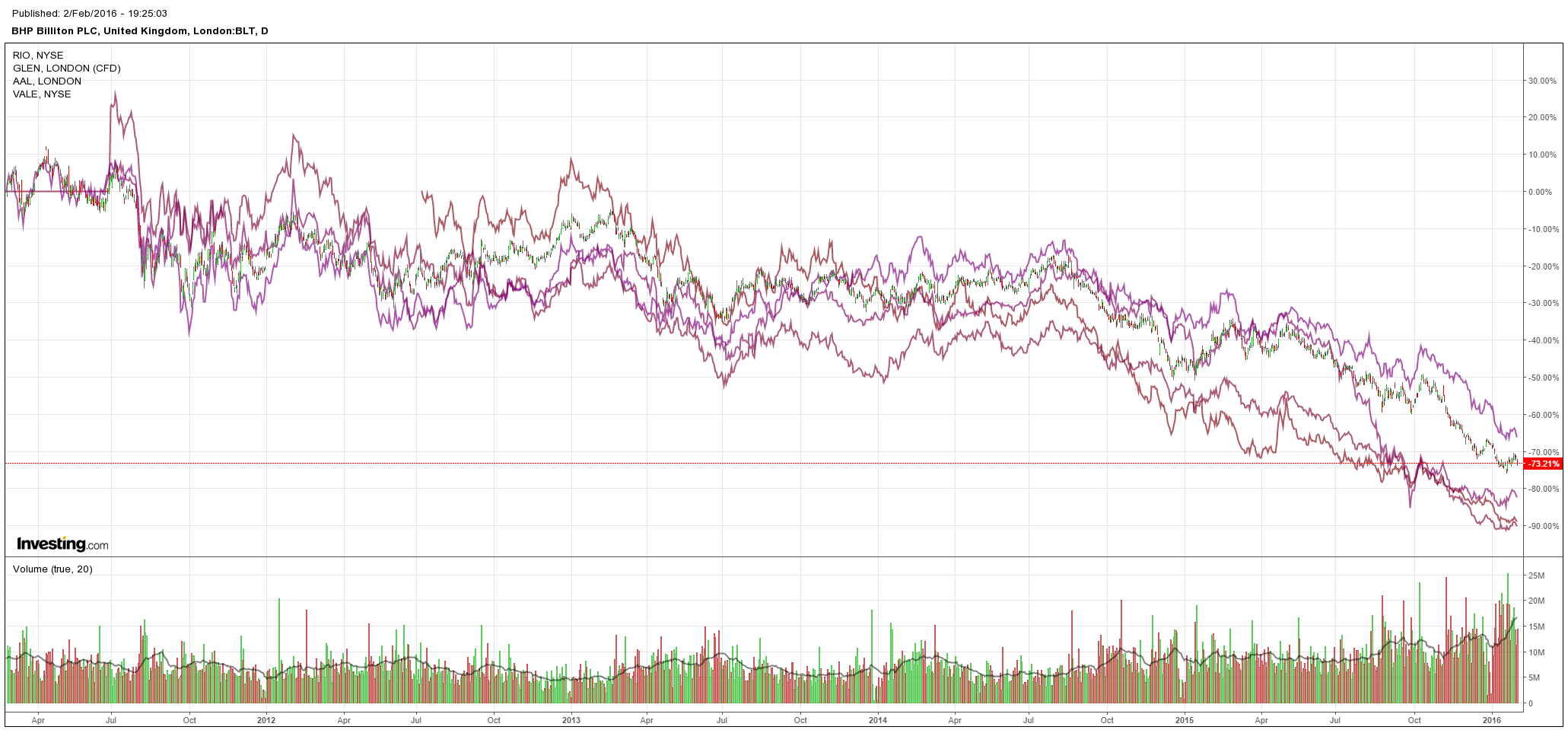

Miners were still monstered:

And US and emerging market (EM) high yield debt (HY) was flogged:

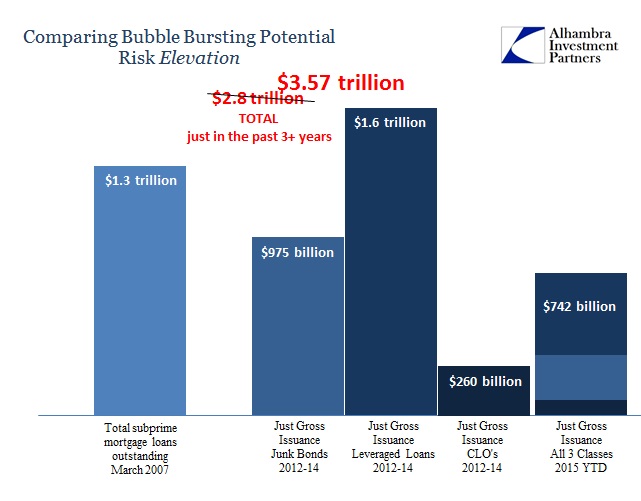

Rounding us out today, here is an interesting chart from Alhambra comparing the amount of US HY yield debt at risk right now versus yesteryear’s US sub-prime mortgage market :

This can be misleading given the US sub-prime mortgage market was the base in an inverted zigurat of debt which collapsed when it broke. Moreover, those assets were all based within the banking system so when it went so did the system.

I don’t think it is the same this time though there’s still massive potential contagion here via the powerful impact that a commodity and HY debt shakeout in the US will have as it spreads throughout EMs of similar dependence and grade.

It is not so much the banking system that is at risk as it is the gigantic global funds management complex that owns all of these bonds. But banks may still be in the firing line, from Gavekal partner, Louis Gave, via the AFR:

Gave argues the market’s behaviour in the past few weeks suggests investors could be starting to worry about banks’ exposure to commodity-related derivatives.

“This unfortunate precedent raises the question of whether we could see a 2008-like crisis, with the catalyst this time around being the bankruptcy of commodity companies which cannot fulfil their derivatives promises, instead of the default of mortgage bonds.”

This, he says, could explain the striking underperformance of bank stocks.

“Looking at market behaviour, it is hard to escape the conclusion that someone is getting one heck of a margin call. Back in 2008, the “margin call” was on everything housing-related – this time around, the margin call is likely to be on everything related to commodities.”

“So here we are, with a panic unwinding on derivative commodity positions and the looming fear that a break in the chain would clean out certain banks. And it is such fears that usually cause banks to lend less to each other, thereby pushing up the cost of capital for everyone.”

One way or another, it is big enough to end the global business cycle.