Yes, it’s all about oil again, this time to the good. The night threatened bad but turned around with an oil rally on rebounding US demand. The dollar was up:

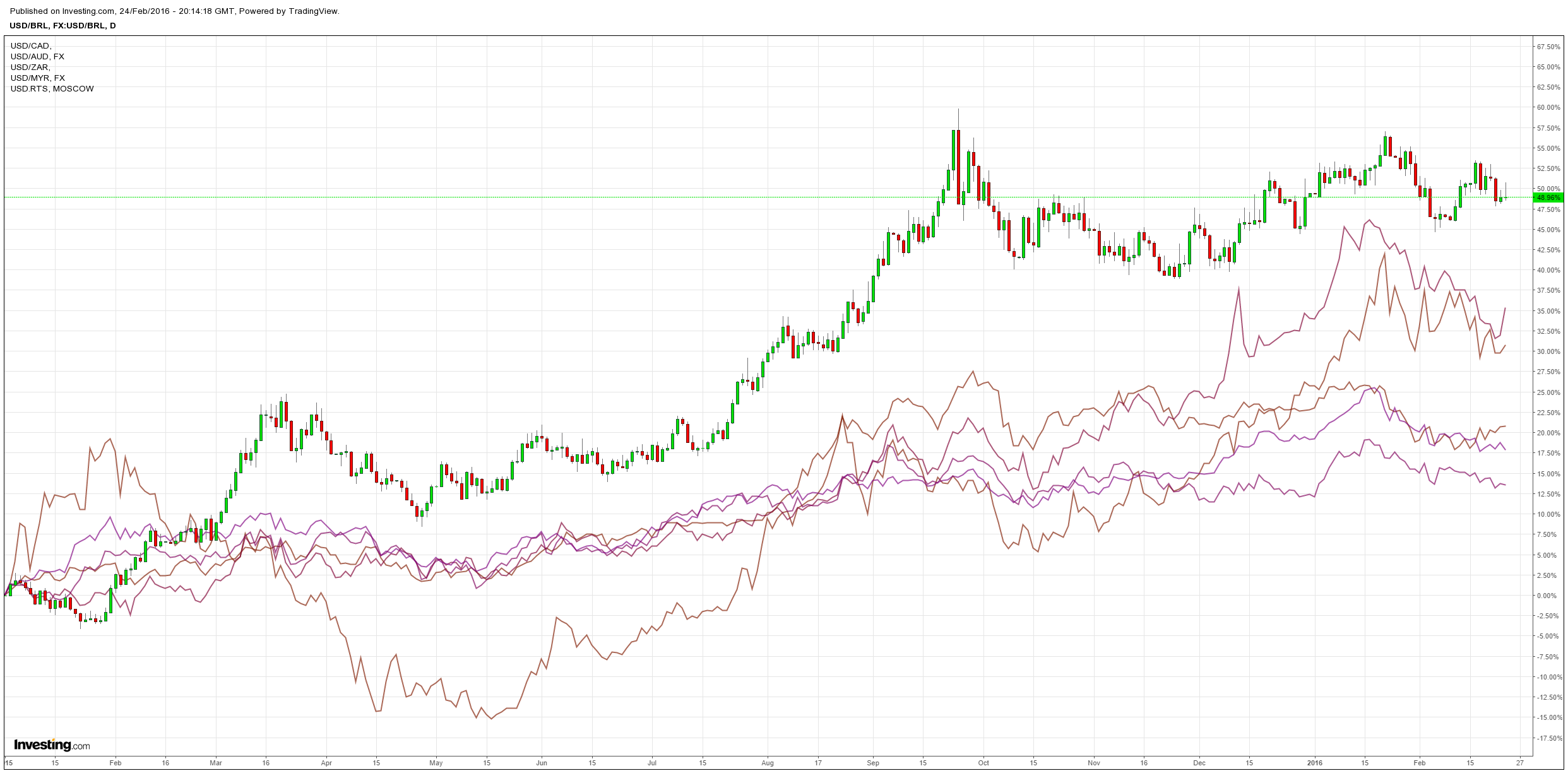

Commodity currencies down though not the Aussie:

Oil up:

Advertisement

Base metals flat:

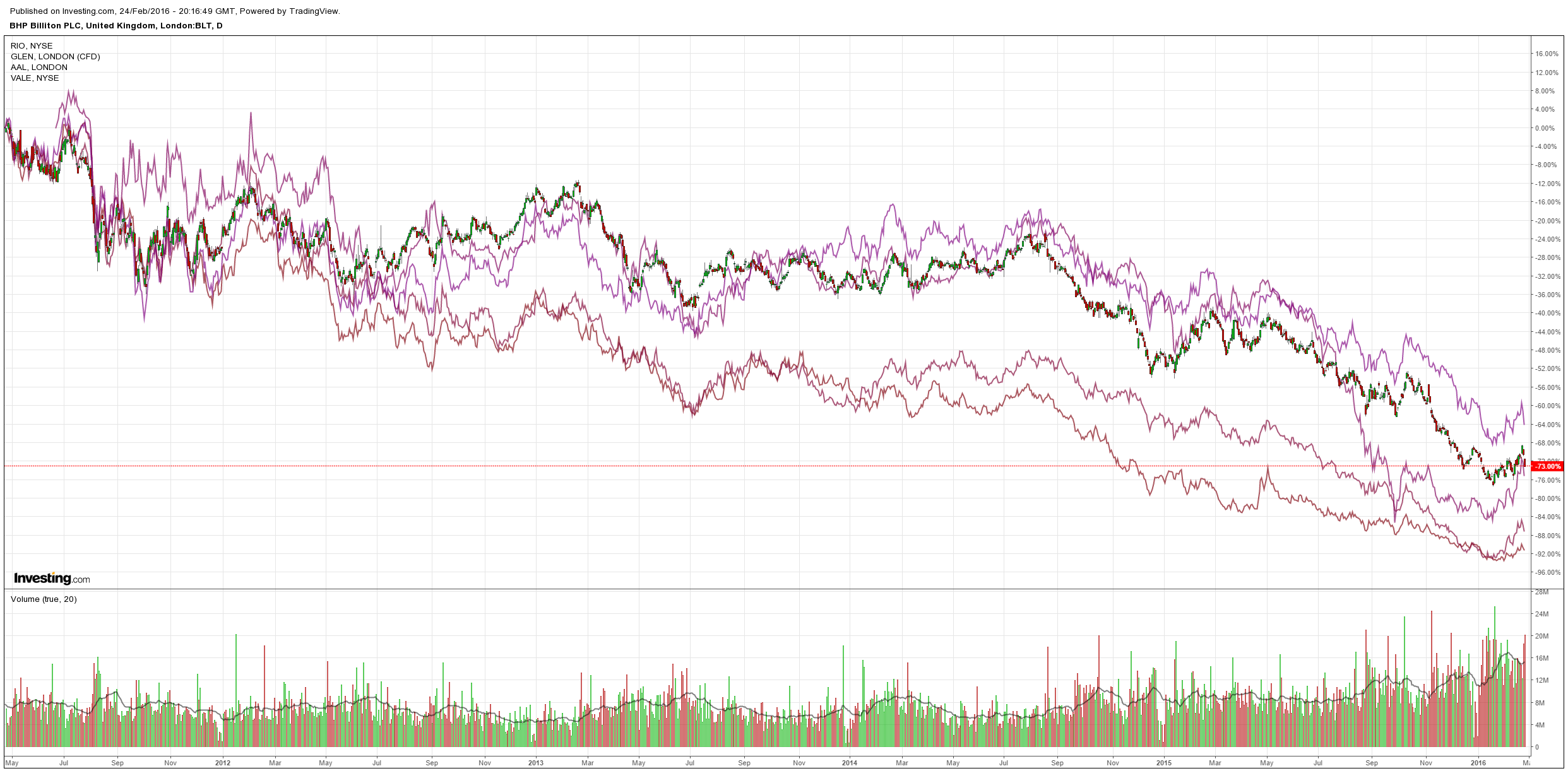

But miners were crushed:

And high yield sold then rebounded to flat:

Advertisement

Bonus material today is from Goldman Sachs which sees more downside ahead:

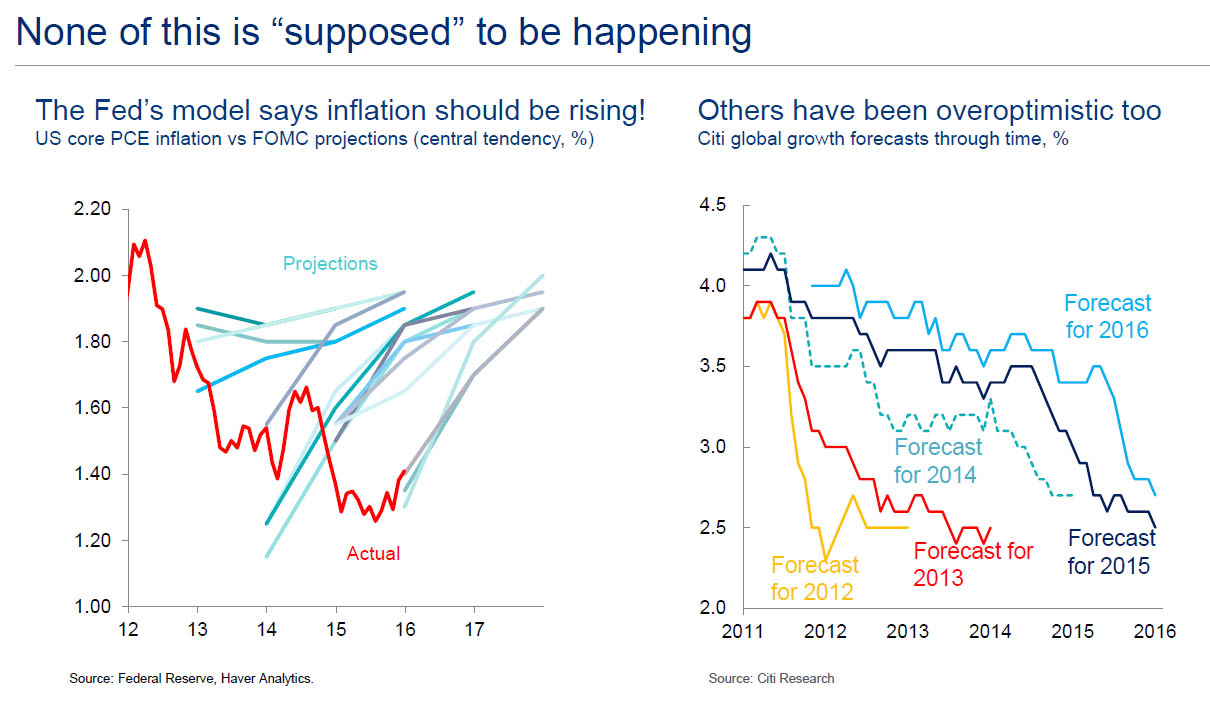

Over the past couple of weeks, it would appear that many of the worries that beset the markets through January have faded. But we think it is risky to read too much into price action currently. Volatility remains very high and much of the moves may reflect positioning rather than a genuine change of view about fundamentals. Remember that at the heart of the correction there has been a growing concern about growth and, with it, the risks of deflation.

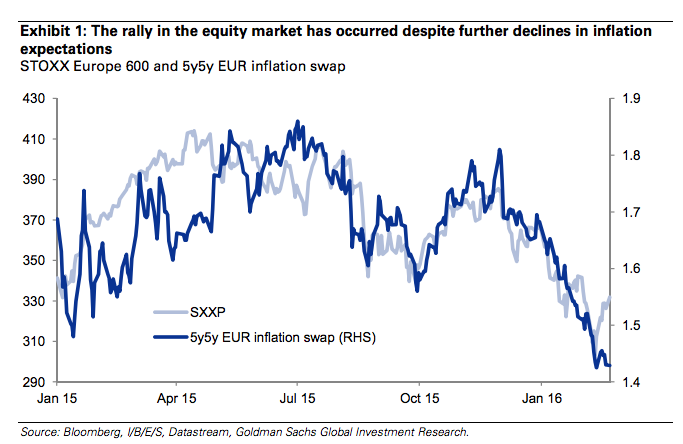

The rally in the equity market has occurred despite further declines in inflation expectations (and bond yields). In Europe 5 year-5 year forward inflation swaps (which Mr. Draghi has emphasized in the past) have recently hit an all-time low.

Even in the US the market is pricing core CPI inflation to turn negative in 1-years’ time, an outcome that did not occur even in 2008-2009; the 5-year/5-year inflation breakeven rate is only at 1.45% – well below the Fed’s target. Ironically the stabilization in oil prices and EM assets that has been at the core of recent short covering and recovery in risk appetite was probably explained initially more by the fear of weaker data than confidence in a genuine economic recovery. Concerns about a broadening out of the manufacturing downturn in January to the broader economy, together with falling inflation expectations and tightening financial conditions, pushed out the expected timing of interest rate rises. This, in turn, has capped the rise in the US dollar thereby alleviating some pressure on commodity prices and EM currencies.

Another critical ingredient of the rebound in risk assets has been the strengthening of the CNY since February and the narrowing gaps between CNY and CNH. Some would also point to a more stable price for oil which likely led to some short covering and resulted in mining and oil moving to the top of the best performing sector list year to date. However, this may be premature. Hopes of an OPEC deal explained some of the stability in oil prices, but our commodity team expects oil prices to remain volatile and oscillate between $20/bbl and $40/bbl in the near term.

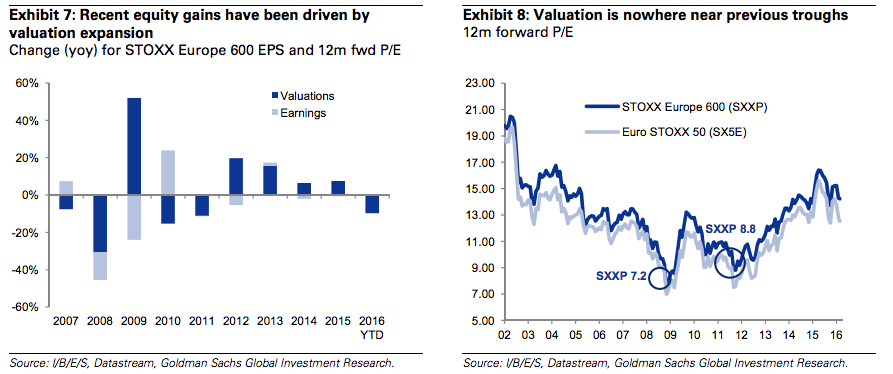

But there has been a roughly 8% rally since the trough – does this mark the start of a sustained recovery in the index?

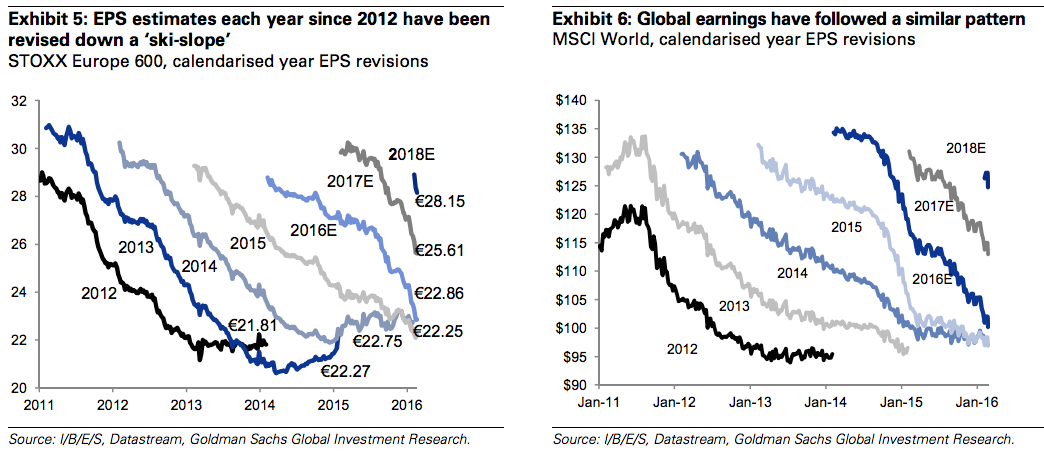

On the valuation front the picture is complicated. Anything that compares equites to bonds makes equities look very cheap. But on the other hand absolute valuations are not yet cheap – prices have fallen but so have earnings expectations.

As a result, most valuation measures have increased in recent years, leaving equities vulnerable to perceived increases in risks. It is for this reason that we think a continued meaningful rise in markets is not likely unless either valuations have fallen further first, or the macro data shows more meaningful signs of improvement and the fears about deflation shift towards fears of missing the leverage to inflation.

For equities to move meaningfully higher from here, we think valuations would need to be cheaper first (around 11x or 12x forward earnings compared with 14x currently). Without this, the market is likely to remain volatile, but tread water until there is a clear shift in inflation expectations.

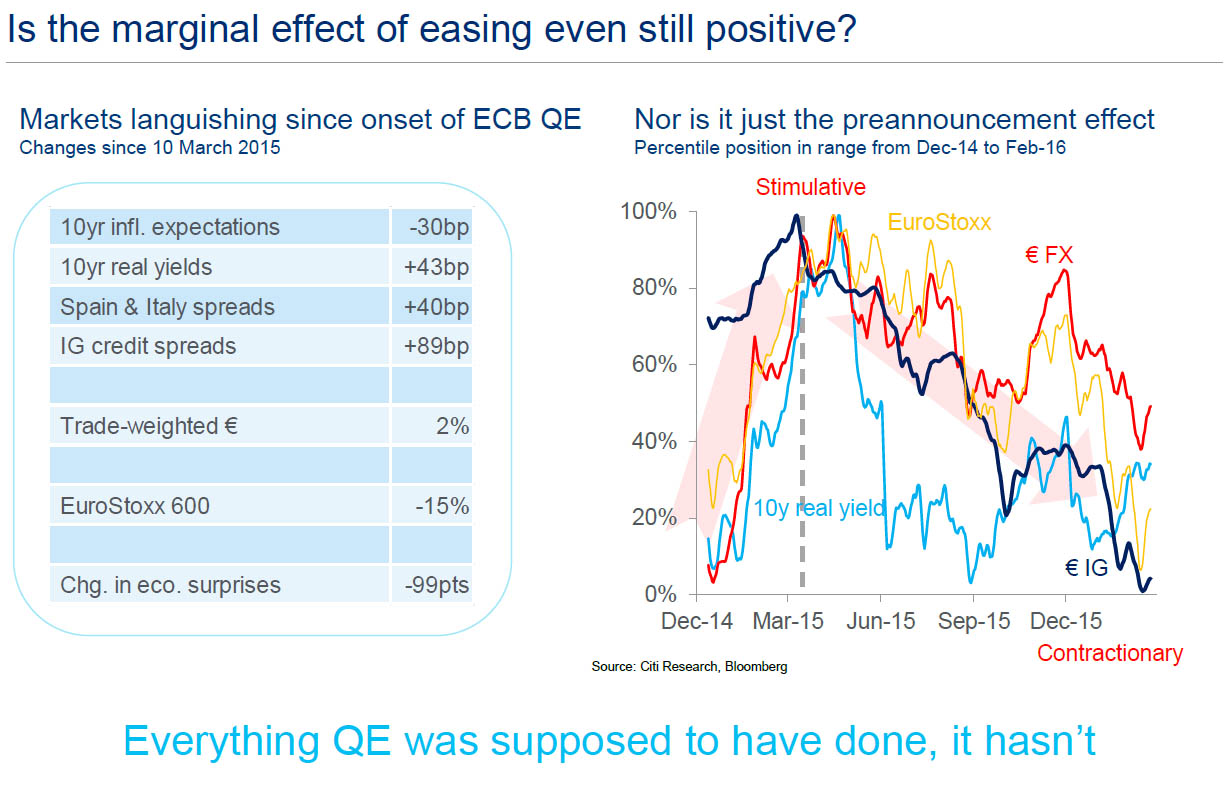

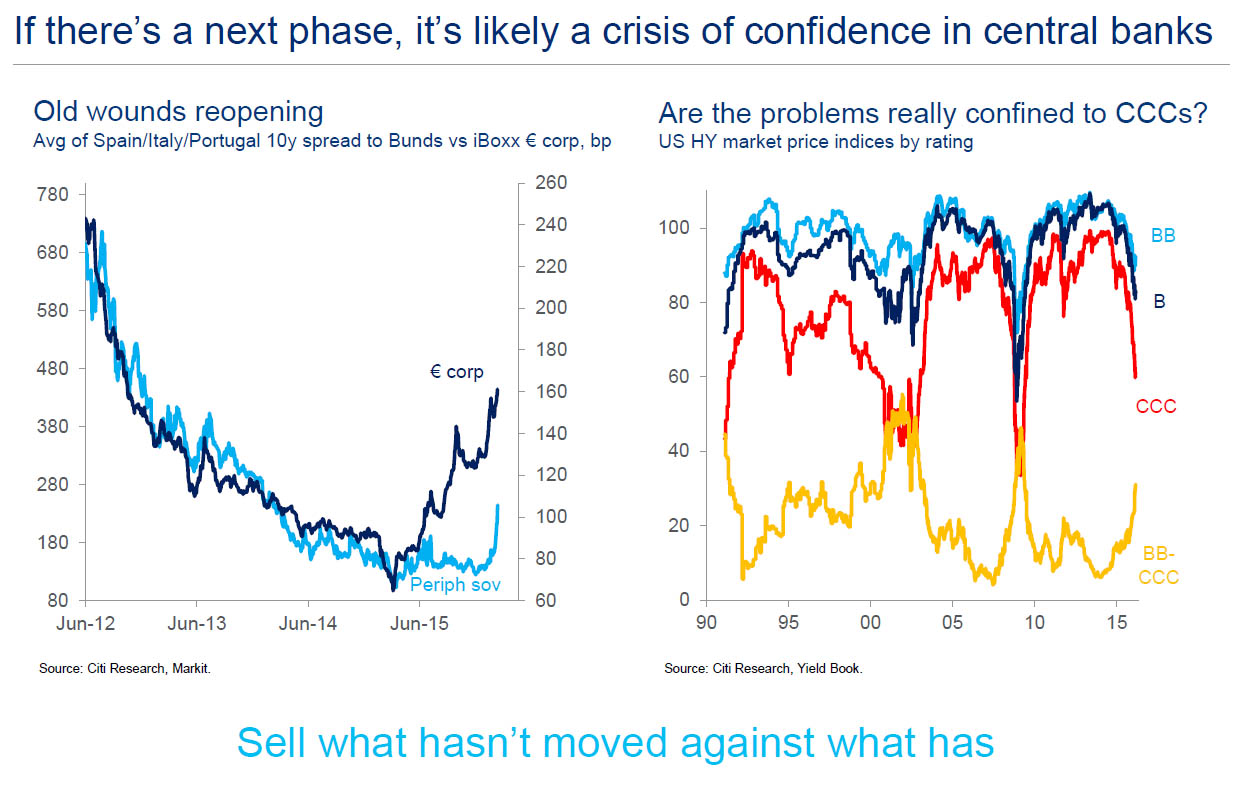

But with the central bank tool box empty, Citi wonders where that lift will come from:

Advertisement

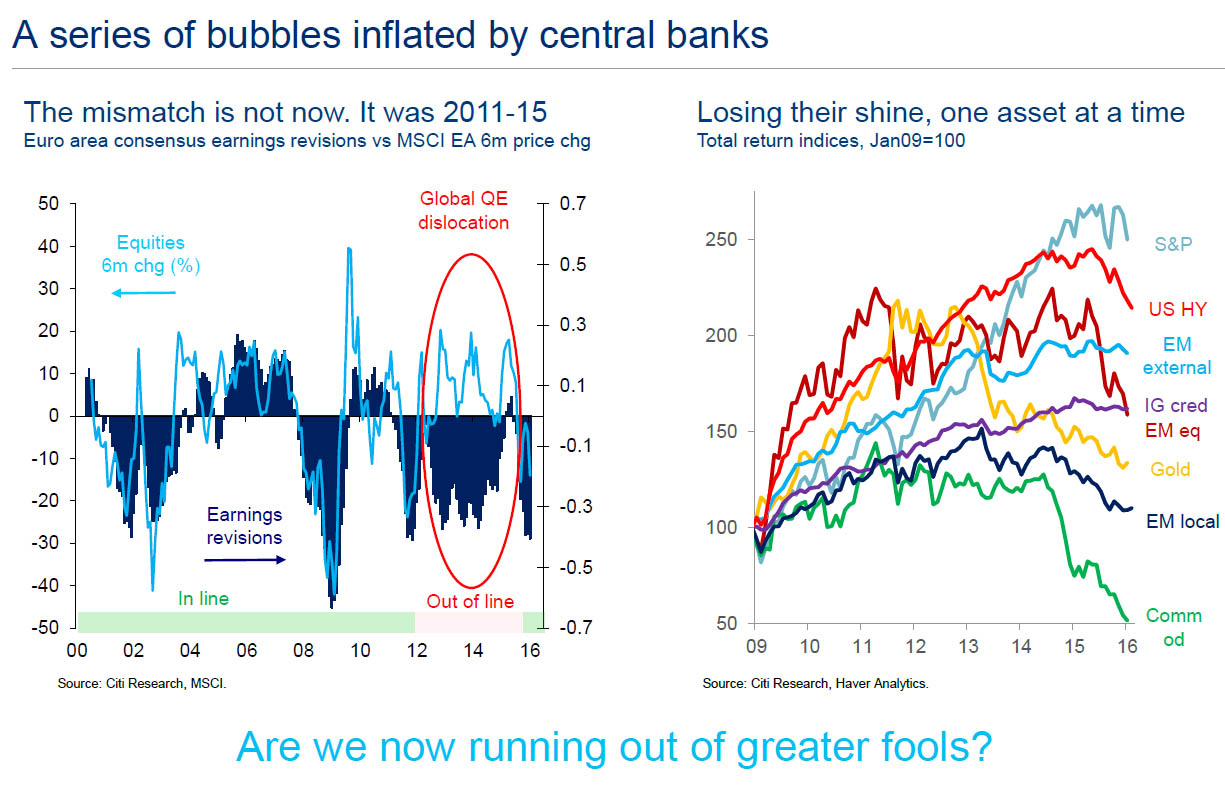

Because CBs can only blow bubbles but that just keeps supply alive creating even less inflation until they burst:

Advertisement

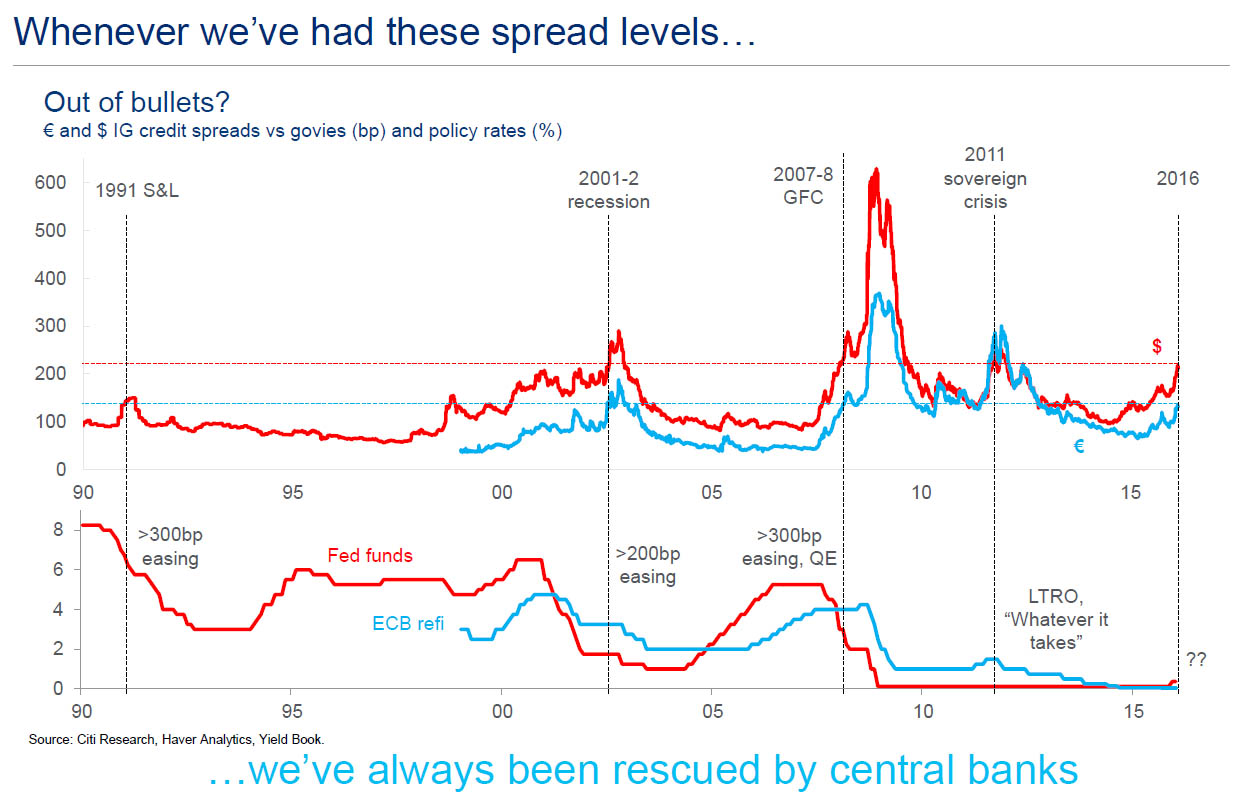

And now they have nowhere to turn:

Which means they are now the problem not solution:

Until they figure out a new path which Martin Wolf again goes down today at the FT:

Advertisement

The world economy is slowing, both structurally and cyclically. How might policy respond? With desperate improvisations, no doubt. Negative interest rates have already moved from the unthinkable to reality (see charts). The next step is likely to include fiscal expansion. Indeed, this is what the OECD, long an enthusiast for fiscal austerity, recommends in its Interim Economic Outlook. But that is unlikely to be the end. With fiscal expansion might go direct monetary support, including the most radical policy of all: the “helicopter drops” of money…

…One alternative then is fiscal policy. The OECD argues, persuasively, that co-ordinated expansion of public investment, combined with appropriate structural reforms, could expand output and even lower the ratio of public debt to gross domestic product. This is particularly plausible nowadays, because the major governments are able to borrow at zero or even negative real interest rates, long term. The austerity obsession, even when borrowing costs are so low, is lunatic (see chart).

If the fiscal authorities are unwilling to behave so sensibly — and the signs, alas, are that they are not — central banks are the only players. They could be given the power to send money, ideally in electronic form, to every adult citizen. Would this add to demand? Absolutely. Under existing monetary arrangements, it would also generate a permanent rise in the reserves of commercial banks at the central bank. The easy way to contain any long-term monetary effects would be to raise reserve requirements. These could then become a desirable feature of our unstable banking systems.

The main point is this. The economic forces that have brought the world economy to zero real interest rates and, increasingly, negative central bank rates are, if anything, now strengthening. This is what the world economy is showing. This is what monetary policy is indicating. Increasingly, this is what asset prices are demonstrating.

Policymakers must prepare for a new “new normal” in which policy becomes more uncomfortable, more unconventional, or both. Can the world escape from the chronic demand weakness? Absolutely, yes. Will it? That demands greater boldness. When one has exhausted the just about possible, what remains, however improbable, must be the answer.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.