The Mining GFC eased again on the oil bid Friday night but other movements in markets show that it’s underpinning drivers have not been fixed at all. Recall that the Mining GFC has two engines in a weakening Chinese economy and yuan and a strengthening US economy and dollar. Markets were a little bedazzled by Chinese leadership at the G20, from Bloomberg:

China’s central bank tweaked the description of its monetary policy stance to reflect a recent ramp-up in liquidity injections and moves to guide money market rates lower, with Governor Zhou Xiaochuan highlighting the scope for further actions if needed.

“China still has some monetary policy space and multiple policy instruments to address possible downside risks,” Zhou said at a conference in Shanghai, speaking hours before meeting his counterparts from the Group of 20 developed and emerging markets. His co-host, Finance Minister Lou Jiwei, said China will expand its fiscal deficit to support structural reforms to the economy.

With few other G-20 members offering much in the way of stimulus pledges — and Germany outright rejecting any — the remarks from Chinese officials helped boostAsian stocks, industrial metals and higher-yielding currencies. Premier Li Keqiang, in a video message to the group, said China can “handle the complex situation at home and abroad.”

The People’s Bank of China also on Friday published a statement defining current policy as “prudent with a slight easing bias.” The PBOC had previously used language pledging to maintain a prudent policy while maintaining “reasonable, ample” liquidity.

The latest comments confirm “the underlying reality that the central bank is doing its bit to cushion growth and keep the wheels churning,” said Frederic Neumann, co-head of Asian economic research at HSBC Holdings Plc. “Today’s statement is thus a deliberate signal to FX traders the world over not to fret too much over the PBOC’s firepower.”

Is it? A renewed easing bias at the central bank looks more like a red rag to a bear given any further rate cuts only intensify pressure on the yuan whatever the PBOC says. Fiscal support is more constructive for the currency but that has already proved itself inadequate to the task of preventing an ongoing glide slope in Chinese growth. I see nothing here to prevent ongoing Chinese capital flight as the dust settles with its corollary of downside pressure on commodities.

Worse for the Mining GFC, the US produced some solid data on incomes and inflation, from Calculated Risk:

Advertisement

Personal income increased $79.6 billion, or 0.5 percent … in January, according to the Bureau of Economic Analysis. Personal consumption expenditures (PCE) increased $63.0 billion, or 0.5 percent.

…Real PCE — PCE adjusted to remove price changes — increased 0.4 percent in January, compared with an increase of 0.2 percent in December. … The price index for PCE increased 0.1 percent in January, in contrast to a decrease of 0.1 percent in December. The PCE price index, excluding food and energy, increased 0.3 percent, compared with an increase of 0.1 percent.

The January PCE price index increased 1.3 percent from January a year ago. The January PCE price index, excluding food and energy, increased 1.7 percent from January a year ago.

OIS markets reacted strongly by pricing in a second US rate hike for 2016 and the US dollar took off:

Advertisement

So, in essence, the major drivers of the Mining GFC both strengthened Friday but markets reacted tactically to the different drivers rather than the overall picture. Commodity currencies fell as the US dollar rose:

But oil rallied again in defiance of the dollar:

Advertisement

And so did base metals chasing Chinese stimulus rhetoric higher:

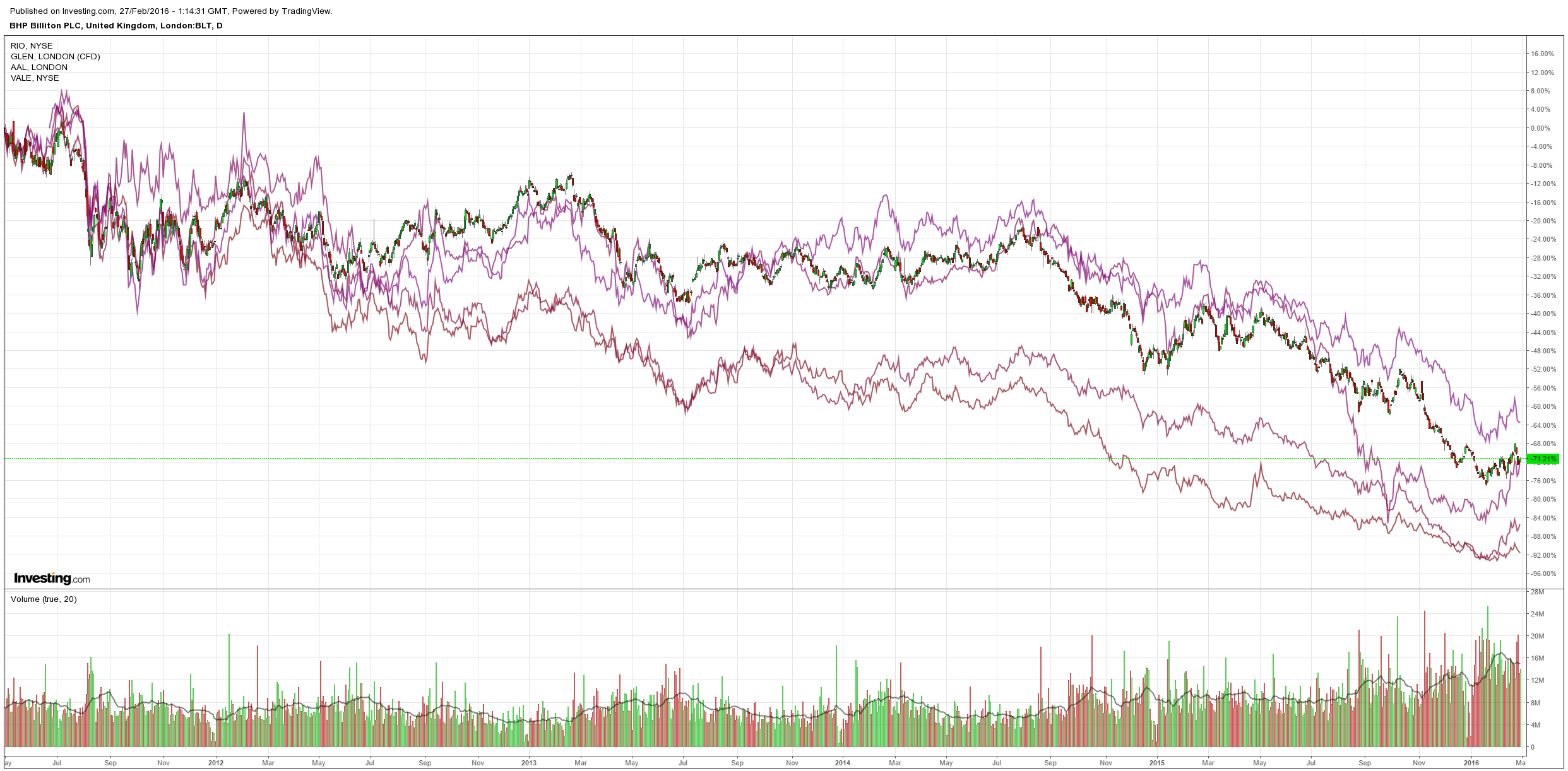

Miners were mixed but biased upwards also on China:

Advertisement

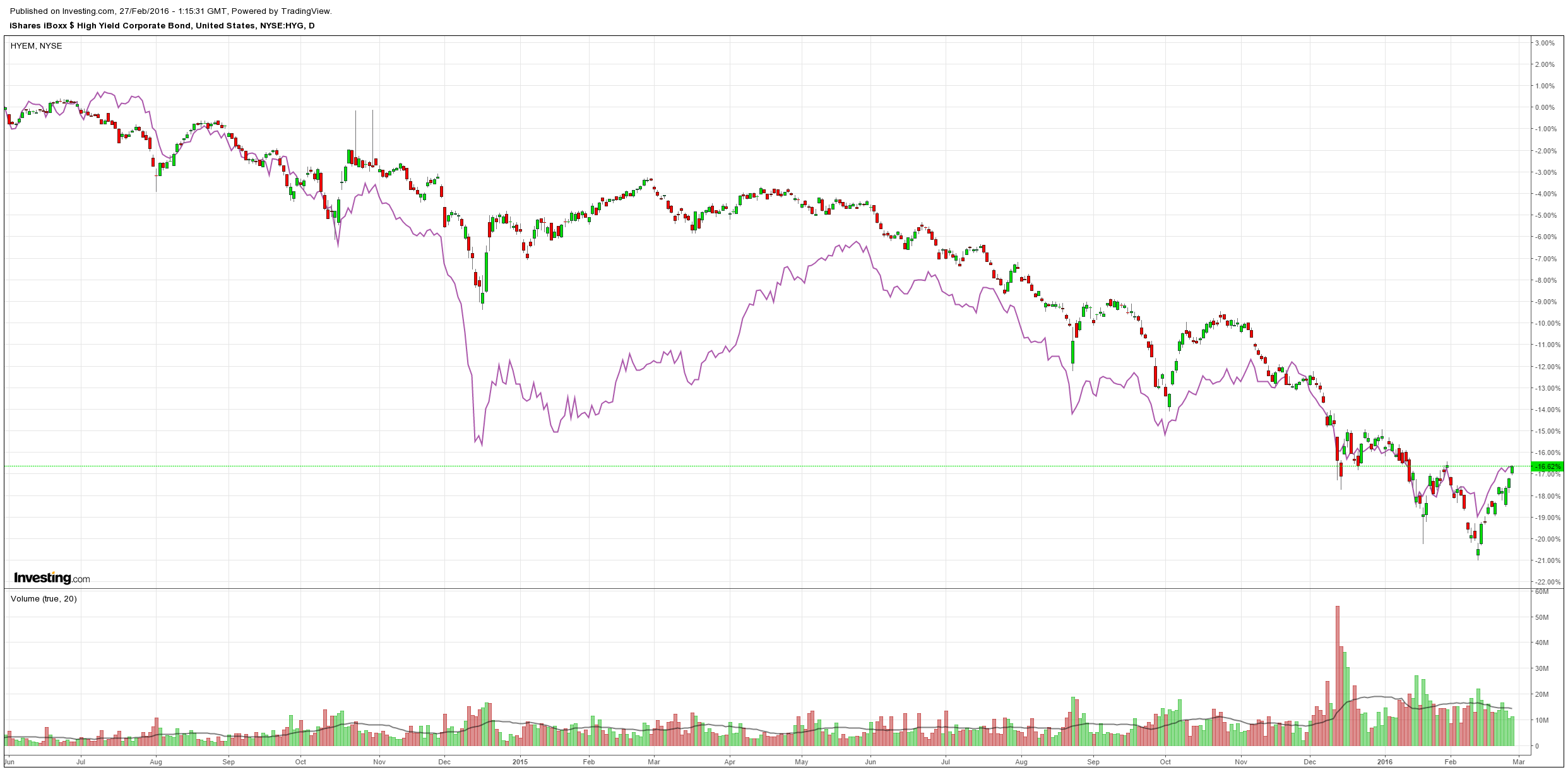

And US/EM high yield was strongly bid on oil:

In short, markets let go of recent Mining GFC growth and forex correlations but I do not expect that to last.

One reason is that G20 failed to deliver any solution, from Bloomberg:

Advertisement

Finance chiefs from the Group of 20 agreed to consult closely on foreign exchange markets and reiterated past pledges to refrain from competitive devaluations.

The G-20 members agreed to use monetary, fiscal and structural tools to boost growth, according to a final communique released in Shanghai on Saturday. Underscoring concerns over the limitations of central bank-led stimulus, “monetary policy alone cannot lead to balanced growth,” the document said.

…”Investor hopes of coordinated policy actions proved to be pure fantasy,” said David Loevinger, a former China specialist at the U.S. Treasury and now an analyst at fund manager TCW Group Inc. in Los Angeles. “It’s every country for themselves.”

…On exchange rates, the G-20 reaffirmed that “we will refrain from competitive devaluation and we will not target our exchange rate for competitive purposes.”

The group also said “we will consult closely on exchange markets” — language that follows surprise moves by China and Japan that led to drops in their currencies. China in August devalued the yuan, then in December shifted its peg to one against a currency basket and in January jolted markets with unexpectedly low reference rates for the yuan. Japan last month stoked volatility in the yen with an unexpected adoption of negative interest rates.

Officials added a potential “Brexit” to its long worry list in the communique…The “large and increasing number of refugees in some regions” was also flagged high. European officials are struggling to solve the worst migration crisis since World War II, with Slovenia and Croatia this week cutting the number of refugees they’ll let across their borders, potentially bottling up migrants arriving in Greece in what that country’s government warned could create a humanitarian disaster.

Even with that catalog of concern, G-20 officials argued recent market swings didn’t reflect global growth momentum.

“While recognizing these challenges, we nevertheless judge that the magnitude of recent market volatility has not reflected the underlying fundamentals of the global economy,” the communique said. “We expect activity to continue to expand at a moderate pace in most advanced economies, and growth in key emerging market economies remains strong.”

That is as close to a worst case document for markets as you can get. Reaffirming the lie that nobody with devalue while they all do, waffling about reform, no commitment to fiscal stimulus and complete denial that there is a crisis at all.

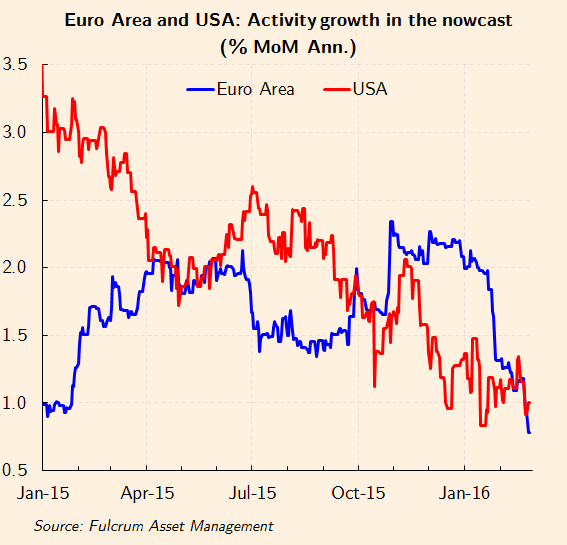

In the next few weeks we have the BOJ, ECB and Fed meetings. Europe is close to outright deflation and “nowcast” models are showing the economy slowing fast too, from Gavyn Davies:

Advertisement

We commented on many occasions during 2015 that the firmness of the eurozone economy was one of the bright spots in the global economic firmament. After many years in which the eurozone growth rate had continuously under-performed that in the US, often by a wide margin, the gap was entirely eliminated in the second half of last year. This was the main reason why growth in the global economy was broadly stable, rather than falling, over that period.

It was probably always too much to hope that the eurozone would take over as the global “locomotive” for very long. The burst of growth seen last year was due to a series of adjustments coming together – less fiscal austerity, the depreciation in the euro, normalisation of bank lending, lower oil prices and the lagged effects of stronger growth in the US in 2013/14. For a time, these forces were sufficient to overcome the weakness of trend growth (now estimated at only 1.3 per cent) and persistent concerns about deflation, so the “Japanification” of the eurozone seemed to be less of a concern.

Unfortunately, this now seems to have been a false dawn. The latest nowcasts show eurozone growth at only 0.8 per cent, compared to 2.3 per cent in late 2015. This result is substantiated by other similar tracking models – for example, the Goldman Sachs “Retina” model now estimates that growth is running at only 0.4 per cent annualised. Eurozone growth has therefore now dropped to below that in the US, even though the latter has remained disappointing at only around 1.0 per cent.

The ECB is going to act. Neither is Japan going to sit on its hands while the yen keeps rising:

I expect both central banks to do moar and the Fed to do less. Then we’ve got Brexit hitting the pound. The US dollar could well find another thermal.

In short, the G20 only served to remind the savvy that all authorities remain miles behind the Mining GFC curve and markets will need to remind them of that fact in the not too distant future. Steen Jakobsen at Saxo Bank has been horribly wrong on a commodity rebound for a year or so but is making more sense today:

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.

We commented on many occasions during 2015 that the firmness of the eurozone economy was one of the bright spots in the global economic firmament. After many years in which the eurozone growth rate had continuously under-performed that in the US, often by a wide margin, the gap was entirely eliminated in the second half of last year. This was the main reason why growth in the global economy was broadly stable, rather than falling, over that period.