The Mining GFC can’t catch a break. One day it is China and its devaluing currency, the next its stabilisation and a stronger US dollar! Remember that as H&H has described for several years, the real problem is the unwind of Chimerican imbalances. With so much of post-GFC global growth driven by rises in Chinese commodity demand and a weak US dollar firing commodity price rises, as well as the gargantuan emerging market supply response, weakness in China and strength in the US dollar is a near perfect reversal of the business cycle.

China intervened in its currency yesterday and attacked the offshore yuan carry trade into the US dollar by driving up Hong Kong borrowing costs, from the FT:

China has opened a new front in its war to curb currency depreciation by buying up renminbi offshore, foiling the burgeoning carry trade and driving the cost of borrowing to a record high.

The elevated overnight CNH Hong Kong Interbank Offer Rate (Hibor) shows how volatility in China’s currency — once a highly domestic sideshow for global investors — is fanning across the globe through renminbi internationalisation. Hong Kong, the biggest offshore market, bears the brunt.

The overnight CNH Hibor, a daily benchmark for offshore renminbi interbank lending, hit a record-high 13.4 per cent on Monday, up from 4 per cent on Friday and the highest level since the benchmark was launched in 2013. The one-week rate surged from 7.1 per cent to 11.2 per cent.

…By buying CNH the PBoC also frustrates the short-term carry trade designed to profit from weakening renminbi. That trade involves borrowing CNH, exchanging the loan proceeds for foreign currency, then repaying the loan once the renminbi has fallen.

That may work for a while but not long. A weakening China still needs more monetary stimulus and that poses the “impossible trinity” wherein policy can only control two of three variables in interest rates, capital flows and currency value. The PBOC is really only fighting to slow the yuan’s fall. That has Goldman issuing a warning for more to come:

Advertisement

After the weakening of the RMB fix against the Dollar by 1.5 percent in December, the first full week of 2016 saw the pace of depreciation pick up, with the $/CNY fix weakening a further one percent. Besides the faster pace, the recent devaluation trend is notable because the Dollar has traded sideways versus the majors over the past month. Our China economists on Friday lifted their 12-month forecast for the $/CNY fix to 7.00 from 6.60 previously, while also raising their end-2017 forecast to 7.30 from 6.80 before, in part because year-to-date moves may signal a different reaction function of the authorities and because of their long-standing view that the cyclical picture remains weak. We complement that forecast change by giving some context to recent moves and provide some interpretation of what policy intentions might be.

China’s balance of payments has seen large capital outflows over the past year, which some argue makes large-scale devaluation inevitable. We caution against treating capital outflows as an exogenous variable, which marches to its own tune. After all, the two months in 2015 with the largest outflows were August and December, months when the authorities devalued the RMB. Our point here is not that there isn’t some “steady state” capital outflow, as Dollar-denominated liabilities are gradually unwound. After all, there were outflows last September and October, when – after the shock of the mini-devaluation in August – RMB fixed stronger. Instead, our point is that the authorities heavily influence the pace of capital outflows via the $/CNY fix (a policy variable), and thus – by extension – the drawdown in official FX reserves they need to absorb. This point is important, because it means that the balance of payments is not “out of control,” a comment we often hear. The opposite is true. A large and growing current account surplus – our last FX Views estimated it at $300 bn in 2015, likely to grow to $360 bn in 2016 – means that China is well equipped to absorb “steady state” outflows. The puzzle is why China weakens the RMB periodically, given that this fans fears of a larger devaluation, exacerbating outflows and thereby – endogenously – reserve losses.

One reason could be their stated objective of making the RMB more flexible and market determined (note that the intention to devalue the RMB has been repeatedly denied by the authorities). If this is what is going on, it helps to recall that the current account is typically weakest in the first quarter, a well-known seasonality that doesn’t just reflect Chinese new year. Between 2006 and 2015, the current account surplus has been $43 bn in Q1, $61 bn in Q2, $68 bn in Q3 and $78 bn in Q4 on average, making fundamentals for the currency the weakest in the first quarter. If a policy objective is to make the exchange rate more flexible and market determined, the first quarter is no doubt a prime candidate for weakening the RMB. Subsequent quarters could then see relative RMB strength, as the current account rises and flows improve. The revised forecast for the $/CNY reflects this rationale, by front-loading RMB weakness and noting that volatility, in addition to direction, may be at play in recent developments.

That is the orderly base case, sure. The risk case is lower, faster, as panic grows. JP Morgan sums it up:

… last year’s capital outflows have been mostly driven by four main components in balance of payments: “loans” and “currency and deposits” within foreign liabilities, and “currency and deposits” and “trade credits” within foreign assets. And the Q3 balance of payments release showed that all these four components experienced a sharp deterioration between Q2 and Q3.

…But beyond the above components, there were two additional components which experienced a big decline in Q3: FDI and portfolio liabilities. The FDI inflow into China declined from $71bn in Q2 to only $39bn in Q3 the lowest quarterly flow since 2009. At the same time the FDI outflow out of China into the rest of he world increased from $29bn to $32bn. As a result, the net FDI balance deteriorated by $35bn on the quarter to a net flow of only $7bn in Q3, the lowest since 2000. Our China economist Haibin Zhu points out that if the reduced FDI inflow into China in Q3 was confined to repatriation of cumulated investment returns rather than exiting of existing investments, this could be a mitigating factor. The Ministry of Commerce data that separate the repatriation of investment returns are only available for July, so we cannot use them to cross check the balance of payments data for Q3 yet.

On the portfolio liability side, Q3 balance of payments revealed that foreign investors sold $17bn of Chinese equities and bonds in Q3 following buying of $16bn in Q2, a swing of $33bn. It is the first time since the fourth quarter of 2011 that the portfolio liabilities’ balance turned negative.

The deterioration in FDI and portfolio liabilities is a worrying development. Up until Q2 capital outflows mostly reflected short-term opportunistic rather than portfolio or long-term FDI flows. As of Q3 this is no longer true. In other words the Chinese capital outflow picture appears to have entered a new phase in Q3, broadening to include FDI and portfolio instruments, something that could make future capital outflows practically boundless. This is especially true with FDI, the stock of which (FDI assets owned by foreigners) stood at $2.85tr in Q3. The stock of Chinese portfolio assets owned by foreigners stood at $788bn in Q3, which is much smaller than the FDI stock but still high in absolute terms.

…In all, a step by step currency depreciation process has proved increasingly more costly for China as capital outflows persist and broaden. This, coupled with the progress in hedging foreign currency debt, raises fears of a steeper depreciation from here.

Advertisement

Anyway, for the night the PBOC succeeded for a few hours in calming markets but then the US dollar firmed and Brent oil crashed -7% also taking down stocks:

“Oil in the $20s is possible,” said Morgan Stanley analyst Adam Longson in a report that focused on risks posed to commodities by the possibility of China further devaluing its currency.

A slowdown in China, whose growth led the rise in global oil demand over the past decade, in recent weeks has added fears of slowing consumption to massive oversupply, even after a 70 per cent price drop over the past 18 months.

While efforts to further weaken China’s currency could help shore up its export-focused economy, it would make imports of oil and other dollar-priced commodities more expensive and would be likely to further hit demand.

“[That] could lead to another round of commodity weakness and send oil into the $20s,” said Mr Longson in the report. “$20-$25 oil price scenarios are possible simply due to currency.’’

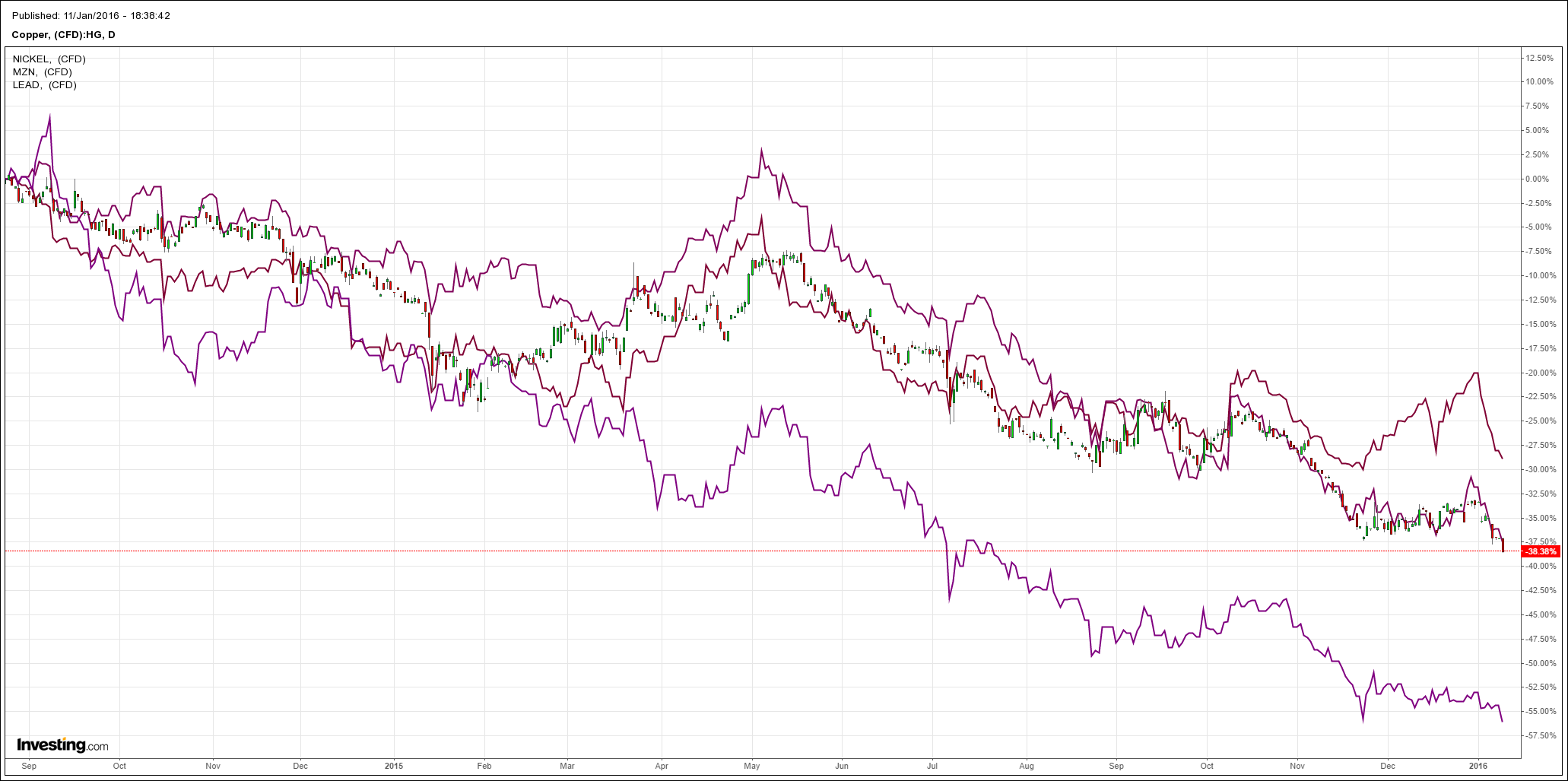

Base metals were flogged with copper hitting new post-GFC lows:

Advertisement

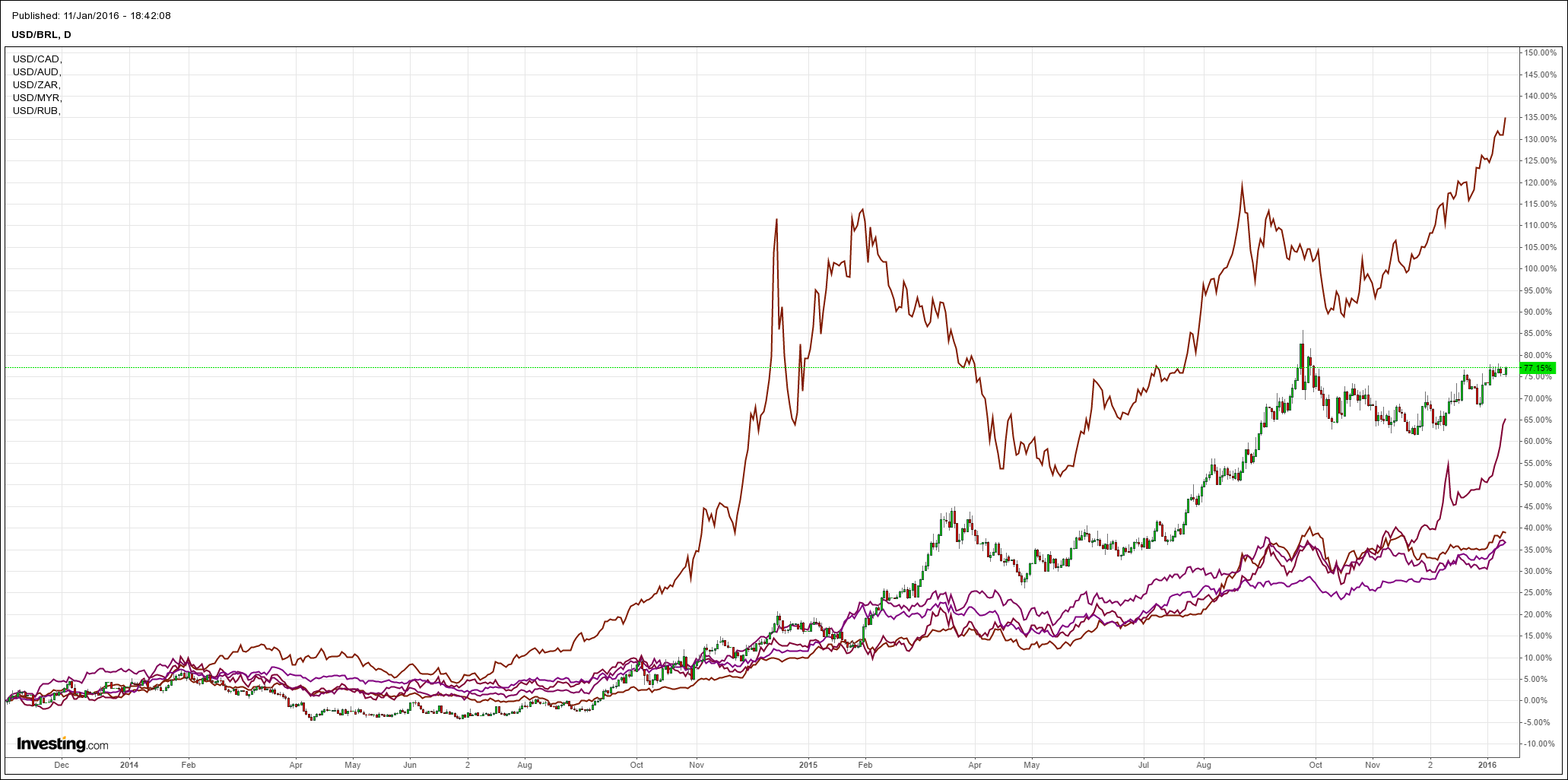

Commodity currencies were thrashed:

And high yield as well as emerging market debt also fell:

Advertisement

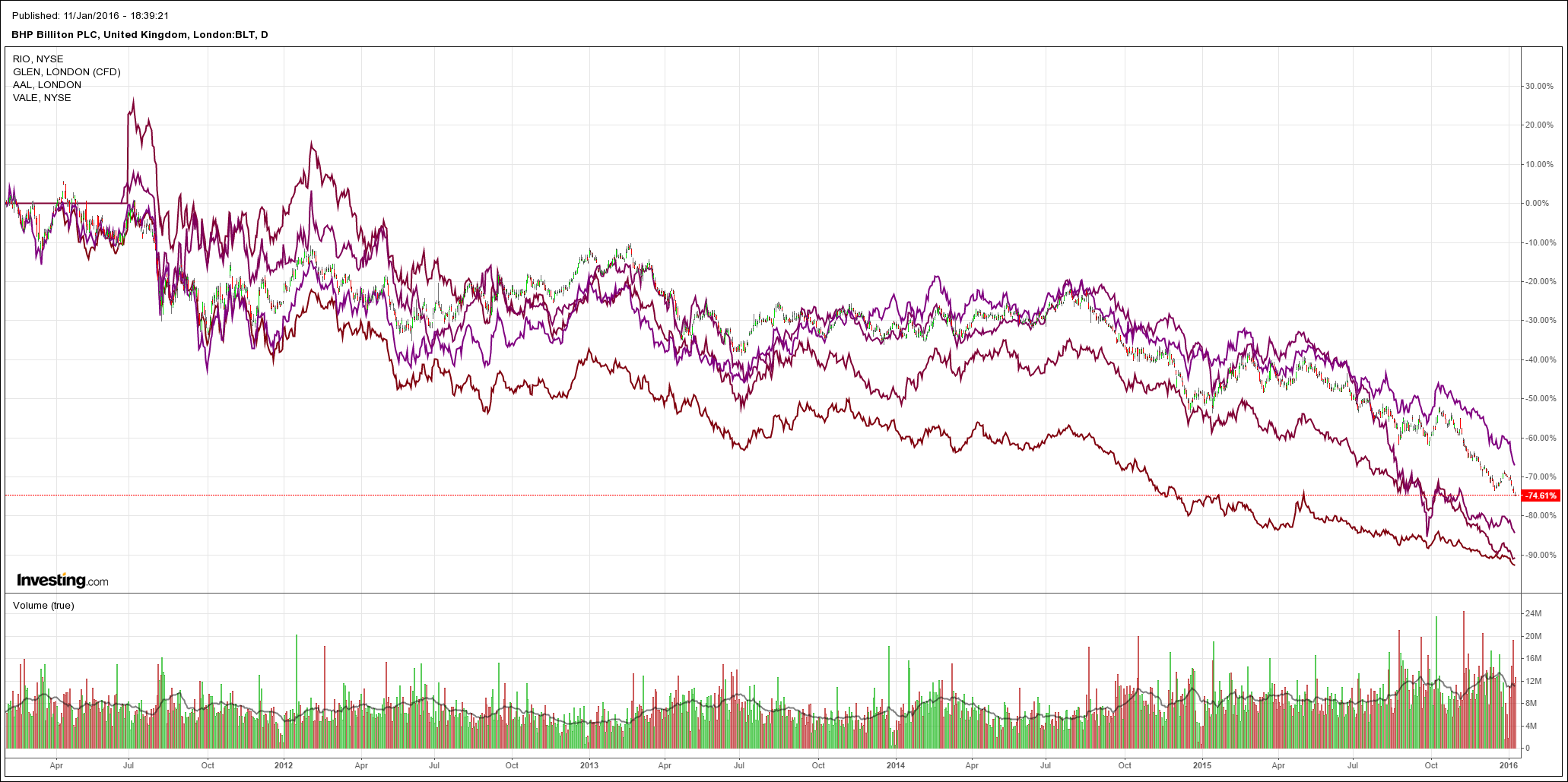

But the real action was in firms. Big miners were smashed again, especially Glencore as it plunges towards its 2015 low:

And Glencore’s cousin firm, Noble Group, also saw its cost of debt rocket, via FTAlphaville

The last print from Bloomberg had Noble 1-year CDS at 2130.51 (click to expand):

And the reason we’re talking one-year instead of five-year CDS is because, well, the curve is well and truly inverted:

Noble’s 2020-yr bond is apparently yielding above 22 per cent, according to Reuters data.

S&P cut the commodity trader citing the higher risk nature of Noble’s trading positions, which it believed would increase the volatility of earnings and profitability at the company.

Advertisement

And we are still to see anyone of magnitude actually go under!

For perspective, this is how a business cycle ends:

a reversal of the dominant investment theme of the period;

a toxic cycle of crushed equity and more expensive debt that continues until something big enough breaks that policy-makers react;

that injects volatility but help comes too late and panic sets in as markets crash;

the shock hits the real economy as households wake in fright;

policy-makers panic, the recession begins and markets bottom.