And so, the MB thesis goes mainstream with Moody’s onto it:

» The commodity downturn is staggering in its breadth and severity. Commodity sectors are facing exceptionally severe adverse conditions driven by a potent mix of slower-than-expected global consumption and excess supply. Prices of oil, copper, iron ore, coal and other commodities have fallen to deep multi-year lows. A key catalyst is slowing demand for materials to fuel China’s industrial and infrastructure sectors. The disappointing outlook for global economic growth signals a long wait for a rebalancing of demand against excess productive capacity. The price decline for most commodities from peak to trough is more pronounced than in past downturns and some commodities may not have yet reached bottom.

» Profound impact for front line sectors of oil and gas and metals and mining. While representing 14% of Moody’s global non-financial corporate ratings, oil and gas and metals and mining comprised a disproportionate 36% of 2015 downgrades through October, and 48% of defaults. The trailing 12-month speculative-grade default rate for the two sectors combined surged to 7.9% in October, from 3.5% a year earlier.

» Credit quality will deteriorate further in 2016. Notwithstanding the high number of downgrades this year, a third of oil and gas and metals and mining companies remain on review for downgrade or have a negative outlook. This is indicative of the bleak outlook for 2016. We expect this downturn to be longer lasting than average and project a further spike in commodity related defaults over the next 12 months. Many companies were temporarily cushioned by hedging programs and fixed-price contracts. Others have been supported by cash cushions that are now eroding. Diminishing liquidity and restricted access to capital markets are pushing more firms closer to default.

» The commodity crisis is the sole driver of the year-over-year increase in the global speculative-grade default rate to 2.7% from 2.1%. For the universe of nonfinancial corporate issuers excluding oil and gas and metals and mining, the trailing 12- month speculative-grade default rate was 2% in October, just marginally higher than the low 1.9% rate recorded a year earlier. Credit conditions outside of commodities remain generally stable. The year to date ratio of downgrades to upgrades for the total universe excluding commodities was a balanced 1-to-1 through October while downgrades outnumbered upgrades 6 to 1 across oil and gas and metals and mining.

Debt-Financed Capacity Spurred Downturn and Will Delay Its Resolution

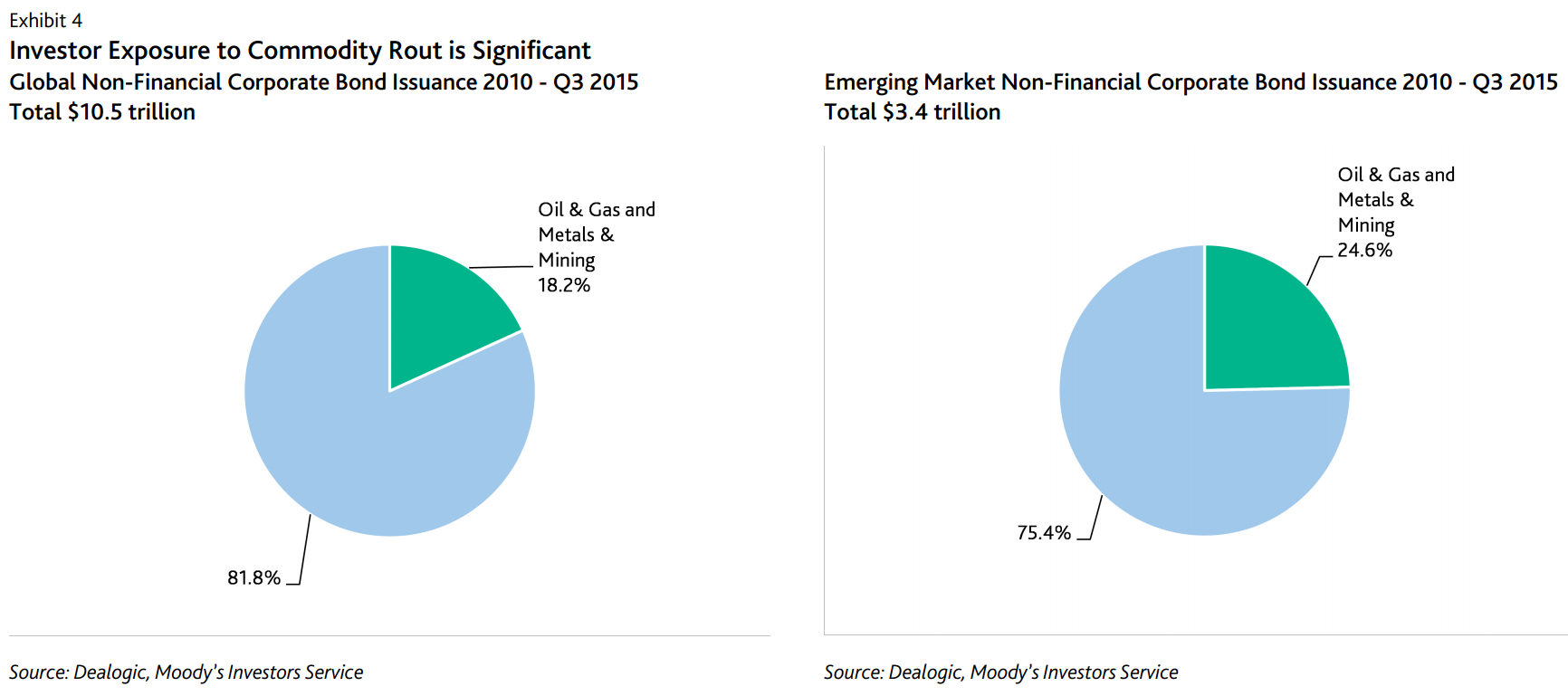

Investors have significant exposure to the commodity downturn due to the surge in global debt sold in recent years to finance capacity expansion. Over the period from 2010 through the first nine months of 2015, oil and gas and metals and mining companies sold $1.9 trillion in bonds, about 18% of global non-financial bond issuance, according to Dealogic. A meaningful share of this activity, 44%, originated from emerging markets and about a quarter of newly minted bonds consisted of speculative-grade issues. This wave of issuance was tied to both the historically low interest rate environment and a consensus expectation that China’s infrastructure development needs would continue to grow rapidly.

Additional production capacity created by this surge in investment has continued to come on line during the commodity downturn as companies complete projects planned and begun when prices were higher. This additional capacity has subsequently led to excess supply. For example, the International Energy Agency calculates that the supply of global oil has increased 9% since 2011 to a production rate of about 96 million barrels per day, ahead of estimated world demand of 94 million barrels. Copper, aluminum, iron ore and other metals are facing similar supply- demand imbalances, while additional secular factors have created particularly severe stress in the coal sector. These include favorable pricing for competing fuels and efforts to reduce carbon emissions. For some commodities (e.g. oil) supply capacity is falling as production depletes reserves and aggregate spending on new projects falls. We note that this is being partially offset by improved efficiency in reinvestment spending, which slows the capacity adjustment process.

Large Sectors Under Stress May Contribute to Broader Market Challenges

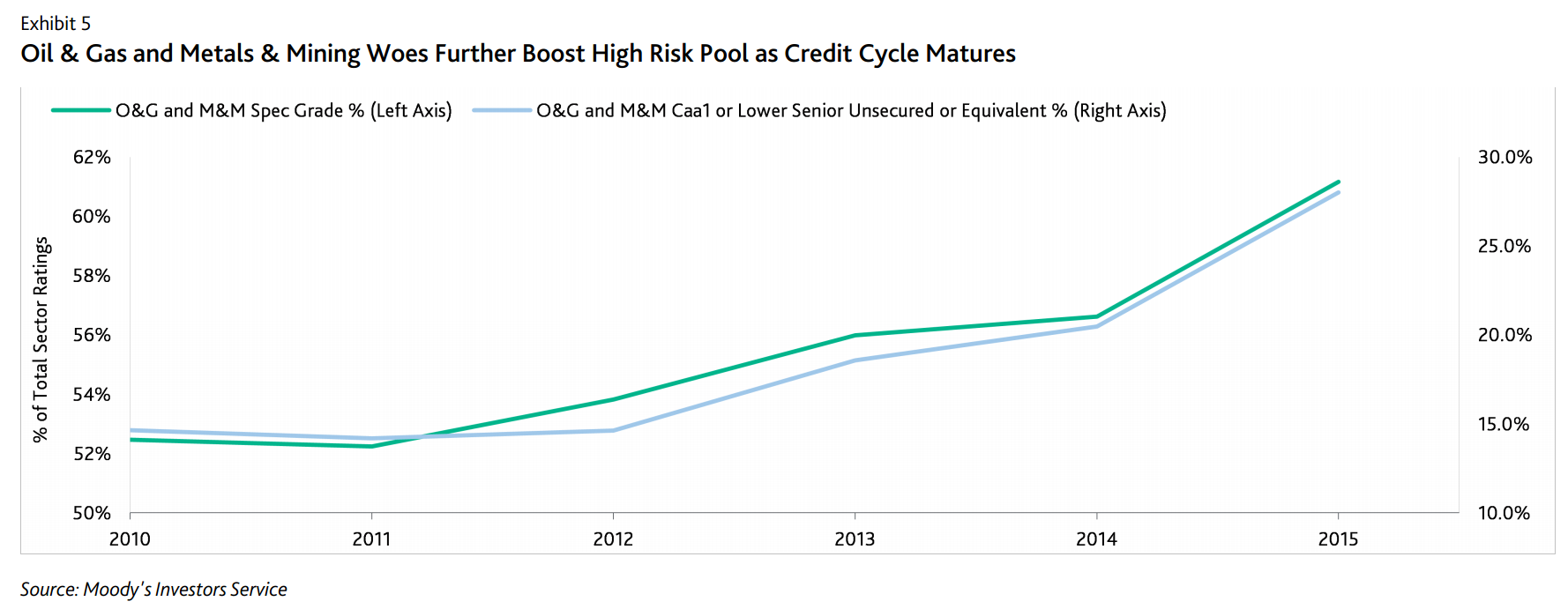

Across the universe of Moody’s rated non-financial issuers, oil and gas and metals and mining companies comprise a meaningful 14% of total ratings. More importantly for default-rate expectations, the number of speculative-grade issuers within these sectors has increased to 61% of ratings in 2015 from 53% in 2010. Prior to 2015, the marked deterioration in the combined group’s average credit quality was mostly due to high downgrade rates in the metals and mining sector. The precipitous but more recent drop in oil prices has put a similar strain on oil and gas issuers. A consequence of the deepening commodity rout in 2015 has been a strong increase in the number of oil and gas and metals and mining companies with senior unsecured or equivalent ratings of Caa1 or lower. Historically such a significant increase in Caa1 or lower issuers has preceded an eventual surge in defaults. The commodity crisis has produced these very low rated issuers at a faster clip than either organic credit deterioration in other industries or downgrades linked to aggressive financial policies.

Adjustments to production in the face of weak prices have been modest, suggesting that for most commodities improving prices will be more dependent upon demand growth that may be painfully slow to build. As long as prices are higher than production costs, most companies continue to produce, even if revenues do not recoup sunk costs to find and develop the assets. Highly leveraged commodity companies are more constrained in their ability to cut back production because they are striving to maximize cash generation to service their heavy debt loads. The weak supply response that results heightens default risks by prolonging low price conditions. An additional concern is that when troubled companies do restructure their debt, this does not typically result in a closure of operating assets. Either the restructured entity or another party that buys its assets is motivated to continue to produce as long as revenues exceed costs.

Oil and gas and metals and mining have already contributed nearly half of the defaults by non-financial corporates year-to-date in 2015. The year-over-year increase in the global speculative-grade default rate to 2.7%, from 2.1%, is wholly due to activity stemming from these two sectors. The vast majority of the defaulters to date have been low-rated, with none being rated higher than B1 a year prior to default.

We believe that the speed and degree of price deterioration and negative market sentiment surrounding weaker companies in commodity sectors will lead to a further spike in defaults in 2016. These sectors are expected to contribute disproportionately to a significant increase in the global speculative-grade issuer default rate to 3.4% by October 2016, although the default rate is also expected to rise for the corporate universe excluding commodity sectors.

We expect an increase in the default rate for the broad universe of corporate issuers excluding commodities due to the growing population of very weak low rated borrowers and reduced investor willingness to fund higher risk credits. However, we expect stress in the commodity space to make a larger contribution to the increase in the default rate in 2016 as hedging arrangements expire, liquidity cushions are consumed, and a larger number of commodity companies restructure untenable debt structures through a combination of distressed exchange transactions and bankruptcy filings.

The sheer volume of commodity related debt poses broader challenges because credit losses from commodity investments will be substantial for many investors. Considering the maturing stage of the current credit cycle, growing losses on commodity company debt seem likely to intensify the capital markets’ swing to greater risk aversion in the year ahead.

Read that report twice. It shows precisely why commodity prices are falling so fast and how that will likely end in an end-of-cycle global debt accident.

On the first point note just how much of the recent growth cycle has been driven by commodity supply chain expansion, some 20-25% of non-financial investment. That has all hit a brick wall and so its own use of commodities has collapsed and, ironically, is collapsing demand for its own product.

Advertisement

On the second point, this is Australia’s global financial crisis finally coming home. A global commodity complex debt freeze would hammer everything Australian from the Budget to bank funding costs to the stock market and house prices.

This is why you need to be preparing your war chest.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.