Brace. Glencore is entering a death spiral and taking big miners with it. Last night it crashed 29.42% to 68 pence:

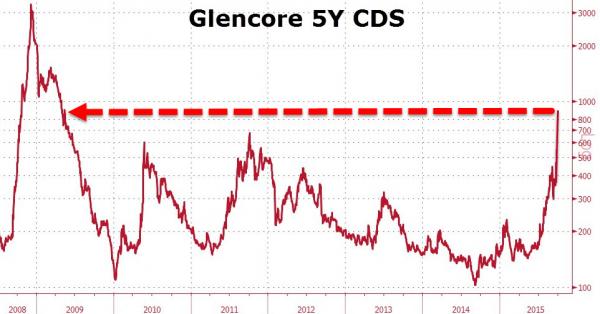

It’s now down -87% from its peak. And whether it survives is an open question. The CDS market is very skeptical, screaming towards GFC peaks:

Advertisement

And, as Bloomberg reports, counter-parties are assuming the worst:

Derivatives traders started demanding upfront payments to protect against a default by the company, the first time that’s happened since 2009, according to data provider CMA

The cost of five-year credit-default swaps jumped so high that they effectively were pricing in 54% odds that the company defaults, CMA data show

“Glencore management need to make an official announcement to calm nerves,” said Darren Reece, a money manager at GAM Holdings AG in London, which oversees $127b.

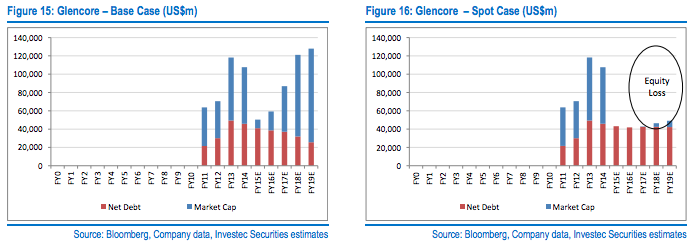

Good luck with that. Instead, Investec put out a dire note, via FTAlphaville:

Advertisement

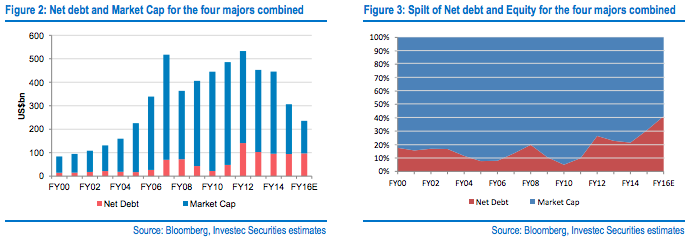

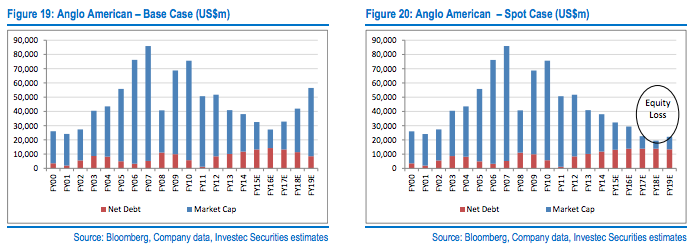

It is the rising percentage of debt that makes this cyclical downturn so toxic for equity holders. Strangely enough, BHP Billiton, Rio Tinto and Anglo American started this century with not dissimilar gearing ratios (defined here as net debt to market capitalisation), ranging between 15% (Anglo American) and 27% (BHP Billiton)…

As we progressed into the Supercycle, shareholders began to own a greater proportion of the overall enterprise value of the company, with average gearing (net debt:equity) falling to 8% in FY05/06. The adoption of debt-based growth strategies in recent years, especially after the GFC, has led to profound changes within the sector. The ready availability of low-cost debt encouraged companies to take on additional gearing to finance the race to grow production, with iron ore development and expansions being the key culprits. The recent fall in commodity prices has compounded the proportion of earnings consumed by debt service – both interest and repayments. This has seen gearing ratios rise to 18% and 25% for Rio Tinto and BHP Billiton respectively, with Anglo American currently at 70% and highly-geared newcomer, Glencore at over 300%, for an aggregate gearing ratio of 41%.

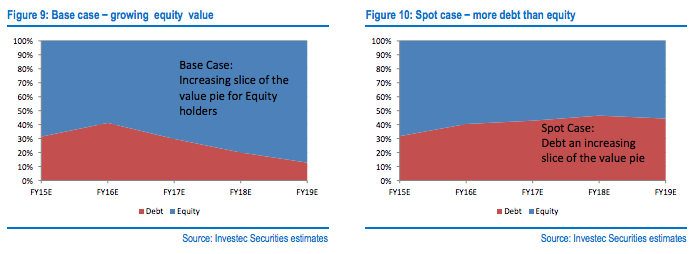

“The challenging environment for mining companies leads us to the question of how much value will be left for equity holders if commodity prices do not improve.”

There is a reason that miners typically carry low gearing. It’s because the industry is so inherently volatile, underlying prices are so very cyclical, and capital demands are large and lumpy. It’s actually not unlike a bank’s core function of maturity transformation in borrowing short to lend long. In the miner’s case it is dig short to repay long. It’s the same reason for why they typically pay low dividends.

Amid the hoopla of the past few years they forgot. As such equity holders in this cycle are in the gun for major losses as they bail out the debt holders.

Advertisement

And here is today’s major miners equity carnage chart:

Last night GLEN was down -29%, Kumba was down -14%, Anglo was down -10%, Vale was down -8%, and in London BHP was down -6% and RIO -5%, which I have assumed will translate to local price above. In short, everyone will be at new lows in the declining trend today.

Back to GLEN, what happens now is a familiar tale as it is surely only a matter of time before credit downgrades enter the fray and repayments on GLEN’s $50 billion gross debt balloons. Here’s what it has to say on such in its own regulatory releases:

Advertisement

Glencore’s objectives in managing its “capital attributable to equity holders” include preserving its overall financial health and strength for the benefit of all stakeholders, maintaining an optimal capital structure in order to provide a high degree of financial flexibility at an attractive cost of capital and safeguarding its ability to continue as a going concern, while generating sustainable long-term profitability. Paramount in meeting these objectives is maintaining an investment grade credit rating status. Glencore’s current credit ratings are Baa2 (stable) from Moody’s and BBB (stable) from S&P.

…Glencore actively and continuously monitors the credit quality of its counterparties through internal reviews and a credit scoring process, which includes, where available, public credit ratings. Balances with counterparties not having a public investment grade or equivalent internal rating are typically enhanced to investment grade through the extensive use of credit enhancement products, such as letters of credit or insurance products.

The strength of those pieces of paper is about to be tested across the entire commodities complex. We’ve seen this story before, no? Toxic assets do not hold up well in an inferno of panic. Commodity liquidation looms.

Perhaps the most interesting dimensions of the growing crisis is that GLEN’s business model might itself prove to be its ultimate downfall. By that I do not mean its monstrous debt. Rather, I mean that as a miner it’s only real competitive advantage is tax minimisation. By definition that leaves it a free-floating multi-national entity with ties to no sovereign or central banks anywhere.

Advertisement

In short, there is nobody to rescue it. It employs 18k Australians.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.