Former Prime Minister, Paul Keating, seems to be losing his marbles in his old age, last night recommending that Australian workers get slugged another levy to cover “geriatric” care for people aged 80-plus:

“We have to have, I believe, a commonwealth insurance scheme for the 80-100s with a calibrated, precise product, which guarantees people income support, aged care and aged accommodation”…

When asked how to fund it Mr Keating suggested: “a longevity levy of a kind — 2 or 3 per cent of wages”…

“You pay it at an early age and it simply goes into a pool.”

Let me get this right. Instead of arguing to broaden Australia’s taxation base by say raising the GST and indirect taxes, and/or implementing taxes on land and minerals, Keating has effectively recommended accentuating Australia’s extreme reliance on inefficient personal income taxes, and in the process making Australia’s diminishing pool of workers shoulder even more of the tax burden?

However, Keating’s war on workers did not end there. He also recommended lifting the compulsory superannuation rate to “at least 12%”.

Needless to say, lifting the superannuation guarantee to 12% would be a retrograde move. Not only would it effectively reduce worker’s disposable income even more, it would also cost the Budget dearly.

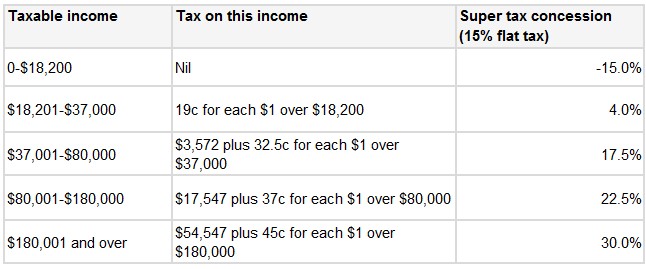

Without reforming the system of tax concessions, which taxes superannuation contributions at a flat rate of 15%, higher income earners would gain even bigger tax benefits under Keating’s proposal, whereas those at the lower end of the tax scale would receive minimal benefits (see below table).

Tax concessions on superannuation already cost nearly as much as the Aged Pension ($44.8 billion compared to $44.9 billion for Aged Pension), and are growing more rapidly, meaning they will become an even bigger Budget drain over time. Keating’s proposal would enlargen the Budget black hole, while doing little to boost superannuation savings for lower income workers – those most likely to be reliant on the Aged Pension.

If Keating was fair dinkum about raising retirement savings, he would instead argue to replace the 15% flat tax with, say, a flat 15% concession. This would have the benefit of: 1) providing all taxpayers with the same taxation concession, thereby improving equity; 2) boosting lower income earners’ super savings, thereby reducing reliance on the Aged Pension; and 3) reducing overall costs to the Federal Budget.