The AFR’s David Bassanese has written a good article today on the ever-expanding black hole that is Australia’s compulsory superannuation system, which is failing on almost every count and sucking the Budget dry:

It is time Australian policymakers admitted their mistakes and faced facts: our unique system of privately run superannuation – Paul Keating’s baby – is a failure.

It is overly expensive, overly complex and highly iniquitous. It needs major reform.

…Joe Hockey [recently] conceded “despite spending billions of dollars in taxation benefits for superannuation, by 2050 the ratio of Australians receiving a full or part pension will still be around four out of five”…

Even with superannuation, generous income and asset tests also allow many well-off Australians to retain some pension…

About half of retiring Australians are also still able to take their super as a lump sum – and before pensionable age – increasing the risk of “double dipping” into the public system later…

Then there’s the inequity…

Bassanese is spot on. It is hard to find a bigger and more egregious tax lurk than superannuation concessions, which already cost nearly as much as the Aged Pension ($44.8 billion compared to $44.9 billion in age pension), but are also growing more rapidly, meaning they will become a bigger Budget burden over time.

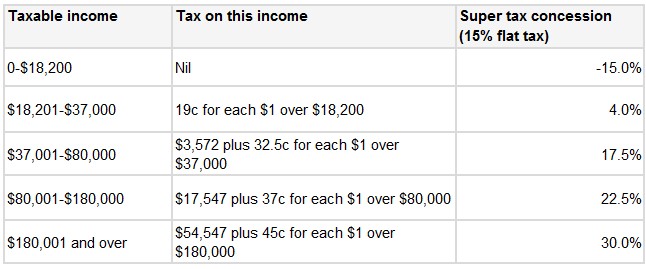

To add insult to injury, superannuation concessions are very poorly targeted, with higher income earners receiving the lion’s share of concessions when they contribute to super, whereas lower income earners actually incur a tax penalty (see below table).

As noted by John Hewson last week:

As a result of this poorly targeted tax concession, 36.1 per cent of the benefits go to the top 10 per cent of income earners, whereas the bottom 10 per cent don’t receive any assistance at all, but are instead penalised…

Treasury estimates that from the combined support of superannuation tax concessions and the age pension, most people (about 80 per cent) receive around $270,000 support over their lifetime. In contrast, the top 1 per cent of male income earners receives about $520,000 support over their lifetime, because of significant tax concessions to high-income earners.

So, by providing massive taxation concessions to those on the highest incomes, the Budget is losing billions of dollars of forgone revenue. The super system is also failing to relieve pressure on the Aged Pension, since those that are most likely to need it – lower and middle income earners – receive minimal concessions (or get penalised), which both hinders their ability to build-up a retirement nest egg and discourages them from making additional contributions.

A related problem is that superannuation can be accessed well before the Aged Pension (i.e. tax free at 60) – a problem that will be exacerbated if the Pension access age is pushed-out to 70, but the superannuation access age remains the same.

If the Government is genuine about tackling entitlements and restoring the Budget back to health, it must place reform of the superannuation system front-and-centre, starting with:

- Providing everyone with the same superannuation concession (e.g. 15%), rather than skewing concessions towards the wealthy;

- Increasing the access age to superannuation (from 55 years currently), so that it more closely matches the pension access age; and

- Reducing the ability to draw superannuation as a lump-sum, to ensure that balances are not exhausted too quickly.

As noted by Bassanese, Australia’s ineffective and poorly targeted superannuation system is a major and growing problem and “politicians have little choice but to chip away at these grotesque failings over time”.