Following Treasury Secretary, Martin Parkinson’s, defining speech at the Sydney Institute earlier this month detailing the stiff headwinds facing the Federal Budget, which is facing decades of heavy deficits without major reforms to taxes and expenditure, as well as rising productivity, the Australian Treasury has reportedly warned that the nation is facing its most sustained period of weak growth for at least 50 years, with the economy forecast still to be feeling the effects of falling commodity prices and weak income growth in 2020:

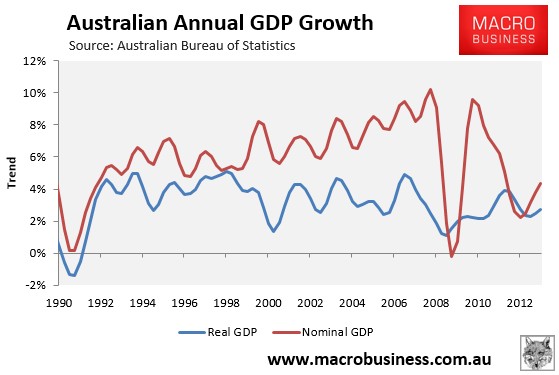

Treasury estimates of nominal GDP, or the value of goods and services produced in the economy, show it will grow by only 3.7 per cent this year and 3.4 per cent in 2014-15, little more than half its 20-year average growth of 6.3 per cent.

Nominal GDP… is expected to average only 4.7 per cent out to June 2018, before rising to 5.6 per cent by June 2021.

The full national accounts published since 1961 show there has never been a period with more than three years of growth less than 5 per cent, while estimates going back to World War II also show no similar period of extended slow growth.

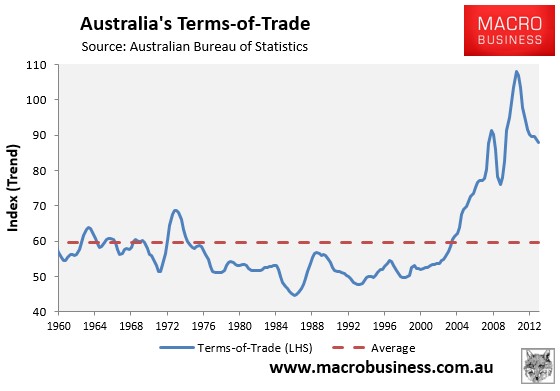

The Treasury is right to be concerned. Nominal GDP is the dollar value of what’s produced and earned. It’s also the measure that drives taxation revenue. Due primarily to the inexorable rise in commodity prices and the terms-of-trade between 2003 and 2011 (with the exception of a brief collapse during the GFC), the Government enjoyed strong nominal GDP growth and booming tax receipts from rising personal and company taxes, not to mention increased capital gains taxes as asset markets boomed. However, since then, the terms-of-trade has begun to trend down, meaning that nominal GDP growth has been weak, as have tax receipts (see next chart).

The problem for the Federal Government going forward is that the terms-of-trade is likely to continue to trend down towards its longer-term average (see next chart), which will drag heavily on income growth and nominal GDP. As a result, personal and company tax collections will be soft relative to past experience, whereas Budget outlays could increase to the extent that weaker employment leads to higher welfare payments.

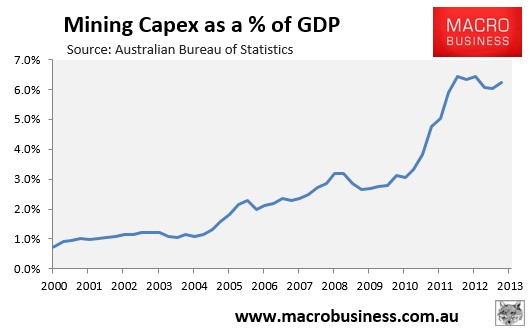

Another related headwind is the decline of mining-related capital expenditures (see next chart), which will detract from Australia’s GDP growth and employment, again placing pressure on government budgets via lower personal and company tax receipts and GST, as well higher welfare payments.

With these budgetary pressures in mind, it was interesting to read speculation emerged over the long weekend that the Abbott Government is considering introducing a temporary “Budget debt levy” on higher income workers in order to eliminate the Budget deficit:

Australia had debt and deficits “stretching out as far as the eye can see”, [Abbott] told reporters in Brisbane.

“It’s important that the mess be tackled,” the prime minister said on Sunday.

“Now we are going to do it in ways which are faithful to the commitments that we made to the Australian people.

“We will do it in ways which are fair, which are equitable, and which I believe will be seen to be fair by the Australian people.”

Introducing a “levy” is clever politics. In doing so, the Coalition can claim that it has not “raised taxes” – as it promised during the election campaign. By claiming that the levy is temporary only – designed merely to eliminate “Labor’s debt” – it can also placate the effected taxpayers, who are less likely to view the tax rise as an assault on workers.

That said, it is also poor economics as it does not address the crumbling structure of Australia’s taxation system associated with Treasury’s weak forecasts.

As argued numerous times before, Australia’s tax base is shrinking. Two of the three main sources of tax revenue – company taxes and indirect taxes (mainly GST and fuel excise) – are either falling or about to fall. Company taxes will fade as the once-in-a-century mining boom unwinds, which will weakening mining company profitability and reduce the corporate tax take. GST revenues are also growing more slowly than the economy (and will continue to do so) as Australians spend a higher proportion of their earnings on GST-exempted items, such as health and education. Likewise, the relative tax take from fuel excise has been shrinking for more than a decade following the Howard Government’s short-sighted decision to end indexation prior to the 2001 Federal Election.

This leaves personal income tax as the only prospective source of revenue growth left for the Federal Government, despite its base also shrinking in a relative sense as the population ages. In turn, the tax burden will increasingly be pushed onto the (shrinking) working population.

The Coalition’s proposed Budget debt levy would, therefore, exacerbate these pressures: increasing the burden on personal income taxes, when instead fundamental tax reform is required to spur productivity, broaden the tax base and share the tax burden.

As highlighted many times before, the Henry Tax Review found personal income tax (along with company taxes) to be highly inefficient, producing a “marginal excess burden” (i.e. the loss in consumer welfare relative to the net gain in government revenue) higher than most other forms of taxation (see next chart).

By comparison, raising or broadening the GST in exchange for cuts to personal income taxes (or giving back bracket creep) would result in clear efficiency gains, with tax expert, Professor John Freebairn, claiming that “changing the tax mix from (income taxes to indirect taxes) brings gains of 20c to 30c in the dollar and beats anything that a major corporation could do on productivity”.

There are also compelling reasons to shift the tax system back towards resource rents, as well as broad-based land taxes, which as shown above (via the Petroleum Resource Rents Tax and Municipal Rates) have almost zero marginal excess burden, since they apply to a tax base that is completely immobile – land. Both taxes are also more equitable than either consumption taxes or income taxes.

The Abbott should, therefore, be seeking fundamental reform to Australia’s tax system, in order to reduce the tax burden on the shrinking working-aged population, and to improve efficiency, productivity, and equity, rather than introducing short-term politically expedient measures like a Budget debt levy, which exacerbate the flaws in Australia’s tax structure. It should also be seeking to plug Budget holes via clamping down on Australia’s world-beating tax expenditures, by limiting tax lurks like superannuation concessions and negative gearing.