RP Data weekly Australian house price update

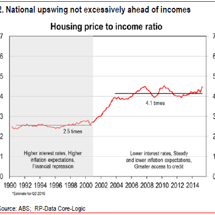

By Leith van Onselen In the week ended 11 June 2015, the Core Logic-RP Data 5-city daily dwelling price index, which covers the five major capital city markets, fell by 0.50% – the fifth consecutive weekly decline, which typically happens this time of year (see next chart).