Minack on whether mining will bust housing

Exclusively for MB paying members from Gerard Minack of Minack Advisors.

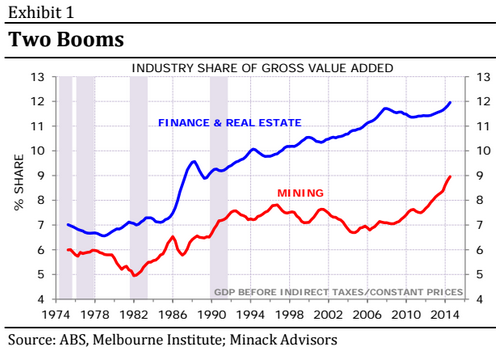

Australia enjoyed two booms over the past 20 years: the well-known once-in-a-century mining boom, as well as an unprecedented boom in banking, borrowing and buying houses. The economy is now struggling with the end of the mining boom. The bear case for Australia is that a mining bust bursts the banking boom.

Australia’s 24 year expansion has run on the back of two booms, in mining and housing/banking. Exhibit 1 shows the rising share of real GDP for both sectors. This under-states the impact of their growth. For mining, it misses the income boost from the sharp rising in the price of mining output, and also the rise in mining-related investment.

The full text of this article is available to MacroBusiness subscribers