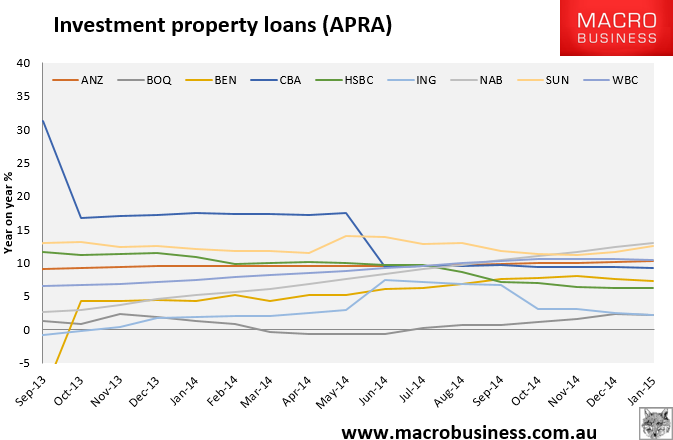

Today I thought I’d have ago at what kind of impact APRA’s declared 10% growth limit for bank lending to property investors actually means for house prices.

To begin, the top ten banks in Australia have seen property investor growth of $44.7 billion in the year to January 2015. In descending order, Mac Bank miles ahead on 73%, NAB is growing at 13%, SUN at 12.5%, WBC at 10.4%, ANZ is 10.3%, CBA at 9.2%, HSBC at 6.2%, ING at 2.3% and BOQ is at 2.2%.

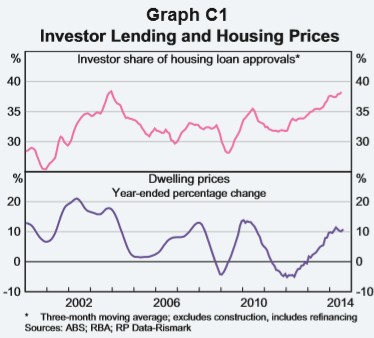

So, half of the biggest banks are over the line. By my calculations, if APRA were to pull these five banks behind 10% then growth in investor credit, all things equal, would fall roughly $3-4 billion over the next twelve months. We can draw a strong correlation between investor credit and house prices, sadly: