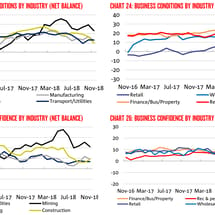

ABS: Half of Australia’s employment growth ‘bullshit jobs’

This is not a picture of economic strength, via the ABS: The number of jobs that where filled in Australia increased by 0.3 per cent in the September quarter of 2018, with around half of the increase being secondary jobs, according to new labour market insights released by the Australian Bureau of Statistics (ABS).