Via the AFR comes Wesfarmers chairman Michael Chaney:

The influential business leader said it was not unrealistic to think house prices in Sydney and Melbourne could fall by as much as 20 per cent… any continued softening in the housing market would be greatly exacerbated by the prospect of a Labor government removing negative gearing.

Although Wesfarmers does not issue a state-by-state breakdown on the performance of its retail divisions, Mr Chaney said his Perth base was a good example of the impact of softening house prices.

“It [falling house prices] has the potential to cause a recession, to cause a recession in spending in the retail sector, and it has been underestimated,” he said.

This follows the very recent panic by CEO Rob Scott at the AFR:

Chief executives from outside the financial services sector are concerned reforms flowing from the Hayne royal commission could hurt the economy if they dry up credit for small business and consumers.

“The risk is that if banks and financial institutions become so risk averse they slow down the provision of credit to individuals and businesses. That would be the key risk which I hope doesn’t happen,” Wesfarmers chief executive Rob Scott said.

Advertisement

Quite right. Here’s the chart:

It’s the recession we have to have so why is WES so upset about it suddenly? Becasue it is the one that has done the under-estimating. Recall Chanticleer recently:

…perhaps the best supporting evidence for Scott’s big Coles spin-off comes when you examine the returns on capital each division of this conglomerate is producing.

At Bunnings, which will officially be crowned the flagship of the Wesfarmers fleet after the Coles demerger, return on capital was a staggering 49.4 per cent, up from 41.8 per cent.

At Officeworks, it was 16.6 per cent, up from 14.7 per cent last year. In the chemicals, energy and fertiliser business, it was 27.7 per cent, and it was 32.8 per cent in department stores.

But at Coles, return on capital was 9.2 per cent, down from 9.7 per cent in 2017, and 11.2 per cent in 2016.

Were we at a different point the cycle then this would be spot on. But we ain’t. Despite what might be an uplift in return on equity, WES is going to get demolished by over-exposing itself to the falling housing cycle and discretionary consumer without the counterweight of the staples business in Coles.

Advertisement

Bunnings is at severe risk from the especially acute downside ahead for residential construction. Other cyclical correction bottoms are a very long way down from here:

Renovations are already rolling over as well, as UBS made clear recently George Tharenou noted recently:

Advertisement

A broad retracement in lead indicators of renovations suggest activity is about to roll over. 1) Total (new + established) home sales fell 8-10% y/y to the ~lowest level in 20 years; and 2) declining listings suggest ongoing weakness in sales ahead; 3) owner-occupier loans for alterations & additions slumped ~20% y/y (contrasting the solid up trend in recent years); 4) which suggests further weakness in A&A building approvals, which flipped from a trend of ~+10% y/y in prior months, to – 9% in June.

Contrary to popular belief, renos do fall during housing busts. See 1990, 2000 (made worse by GST), 2008 and 2012:

Advertisement

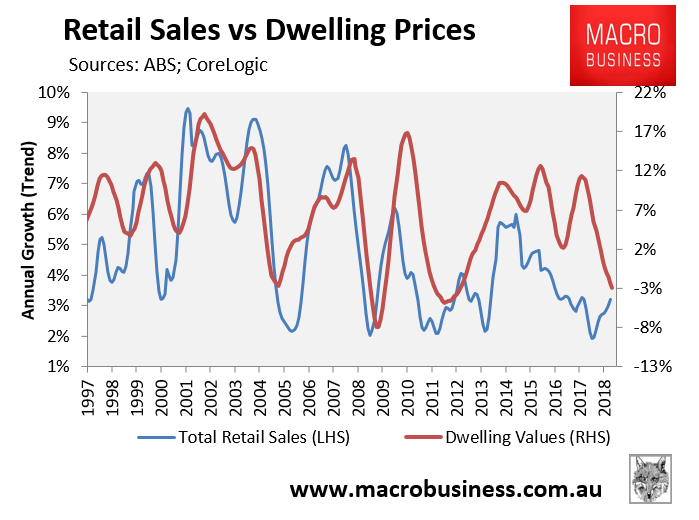

And discretionary spending always tracks house prices eventually, via Credit Suisse:

Advertisement

Smashing WES’s other discretionary spending retail verticals.

Coles will be fine but WES is transforming itself into the perfect short for Australia’s housing bust cycle. Whoops!

Yet the market is yet to price any of this:

Advertisement

Perhaps it should start listening to the panicky WES executives…

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.