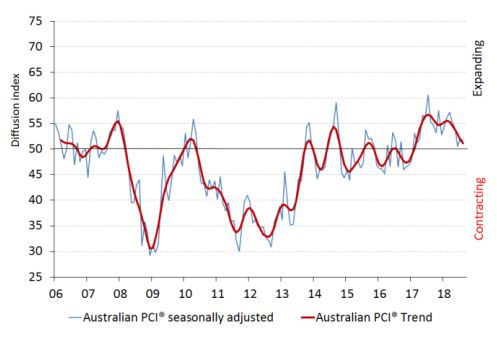

▪ The seasonally adjusted Australian Industry Group/Housing Industry Association Australian Performance of Construction Index (Australian PCI®) fell by 0.2 points to 51.8 points in August. This signalled a positive but marginally slower pace of overall industry growth (readings above 50.0 points indicate expansion with higher numbers indicating a stronger rate of expansion).

▪ For the construction industry as a whole, activity and employment both fell into mild negative territory (i.e. below 50 points) following subdued growth in July. However, the new orders subindex lifted solidly on the back of stronger demand conditions across the major building and infrastructure project areas of construction.

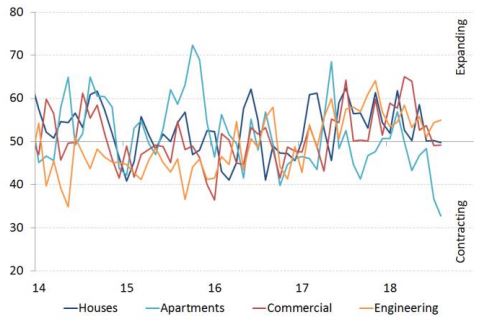

▪ Across sectors, engineering construction drove growth in industry conditions in August. This was consistent with reports of new tender wins and ongoing support from a strong and expanding pipeline of publicly funded investment in large-scale infrastructure projects.

▪ House building activity drifted into negative territory in August, although the rate of decline was marginal and broadly in line with the stabilisation of conditions evident over the previous two months.

▪ Apartment building was the weakest performing sub-sector in August with activity contracting for a sixth consecutive month, and at its sharpest rate in almost six years.

▪ Commercial construction was again subdued in August, remaining in slight negative territory for a second month although businesses reported an improvement in tendering opportunities which is likely to support firmer activity ahead.

▪ House building respondents to the Australian PCI® continued to indicate support from a solid backlog of work. However, businesses noted that tighter lending conditions and a more cautious approach by prospective buyers were adversely impacting on housing demand.

▪ Apartment builders indicated that activity was being driven lower in response to project completions, reduced enquiries and falling investor demand.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.