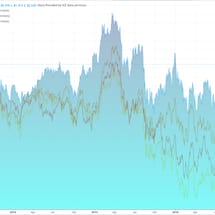

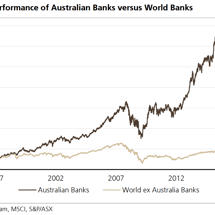

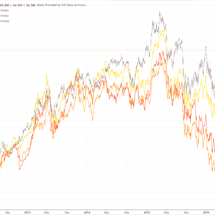

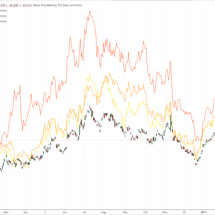

You want to know how good Aussie banks have it?

This good, via UBS: Australian Banks Have Outperformed Global Banks & The Australian Market The absence of a domestic recession for more than 25 years, alongside a progressive decline in interest rates, has created a fertile backdrop for Australian banks to significantly outperform both global banks and the broader Australian market.