CBA is out with its trading update today and it continues the trend of recent “utility” profits, via AFR:

Commonwealth Bank has met expectations on Tuesday morning after announcing a small rise in third quarter cash profit to March 31 of $2.4 billion from $2.3 billion from the previous corresponding period.

The result was augmented by above system growth in household deposits and business lending while the bank pulled back from home lending. The bank grew its home lending book over the period by 7 per cent compared with system growth of 7.8 per cent.

Market watchers however are likely to zero in on the deterioration in the net interest margin – the difference between the price it pays for funds and what it can lend it for – which fell slightly over the period and was sheeted the back to the competitive environment. The bank’s NIM fell 4 basis points to 211 at the bank’s interim results in February.

ABC’s The Business ran a segment last night examining the potential impact of a housing downturn on the Australian banks’ growth, given their heavy reliance on home lending.

The segment features Patterson Securities’ Tony Farnham, who believes that while a housing crash is unlikely, bank revenue and profits are likely to be crimped as regulators clamp-down on the investor segment of the market, unless business lending can pick-up the slack.

Steve Johnson from Forager Funds Management is more bearish, noting that “the size of the mortgage market in Australia relative to the economy is larger than anywhere in the world and it is impossible for other parts of the economy to take up the slack there… They can lend 80-90% against the value of houses, but they would never lend that much against a business or a different asset class”.

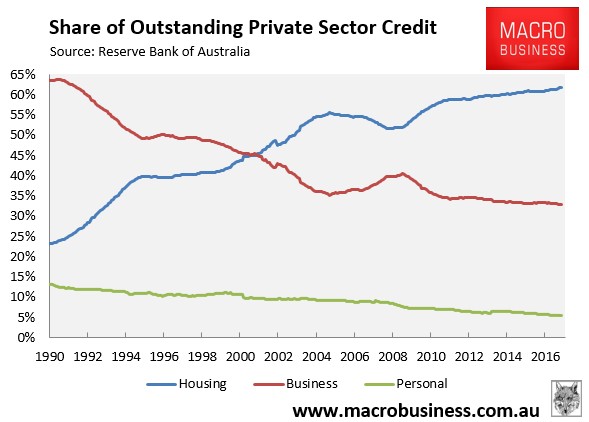

We concur with Steve Johnson’s assessment for several reasons.

First, the share of bank lending going to mortgages is roughly twice that of business lending:

Hence, for every 1% fall in mortgage lending, business lending would need to rise by roughly 2% (other things equal) just for the banks to tread water.

Second, as noted by Johnson, the leverage available to housing lending – 80% to 90% is way higher than that available to business lending.

Third, APRA bank capital rules are far more generous towards housing lending than business lending. That is, the typical risk-weight applied to mortgage lending will rise to just 25% for the major banks, whereas it is far higher for business lending (e.g. 100% for corporate borrowers without a credit rating).

In short, there is no way that business lending can pick-up the slack from mortgage lending. Where goes Australian property goes Australia’s banks.