Iron ore sinks as Chinese yields rip

Advertisement

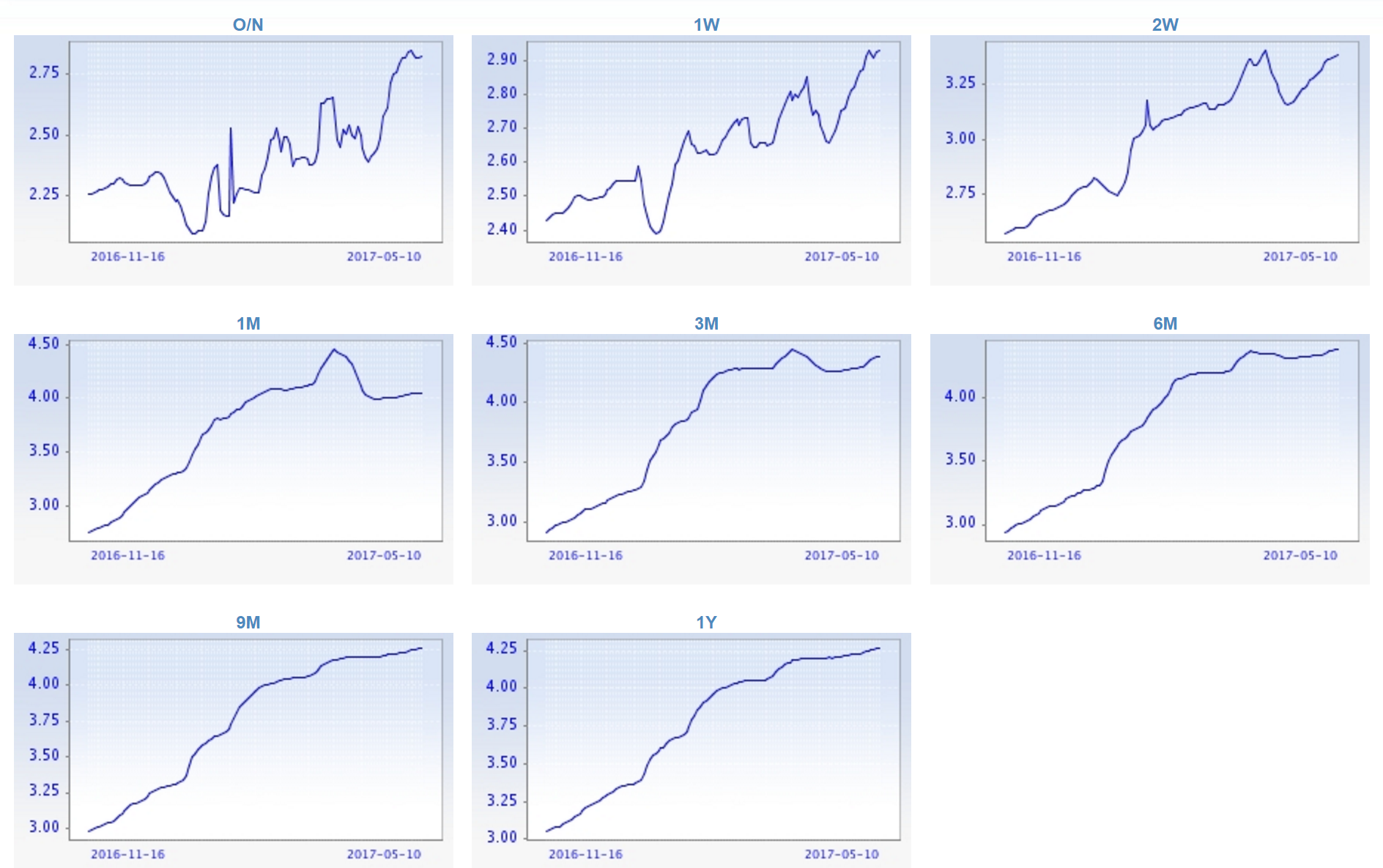

Chinese yields are putting on an extraordinary display. Interbank markets remain tight for SHIBOR and repo:

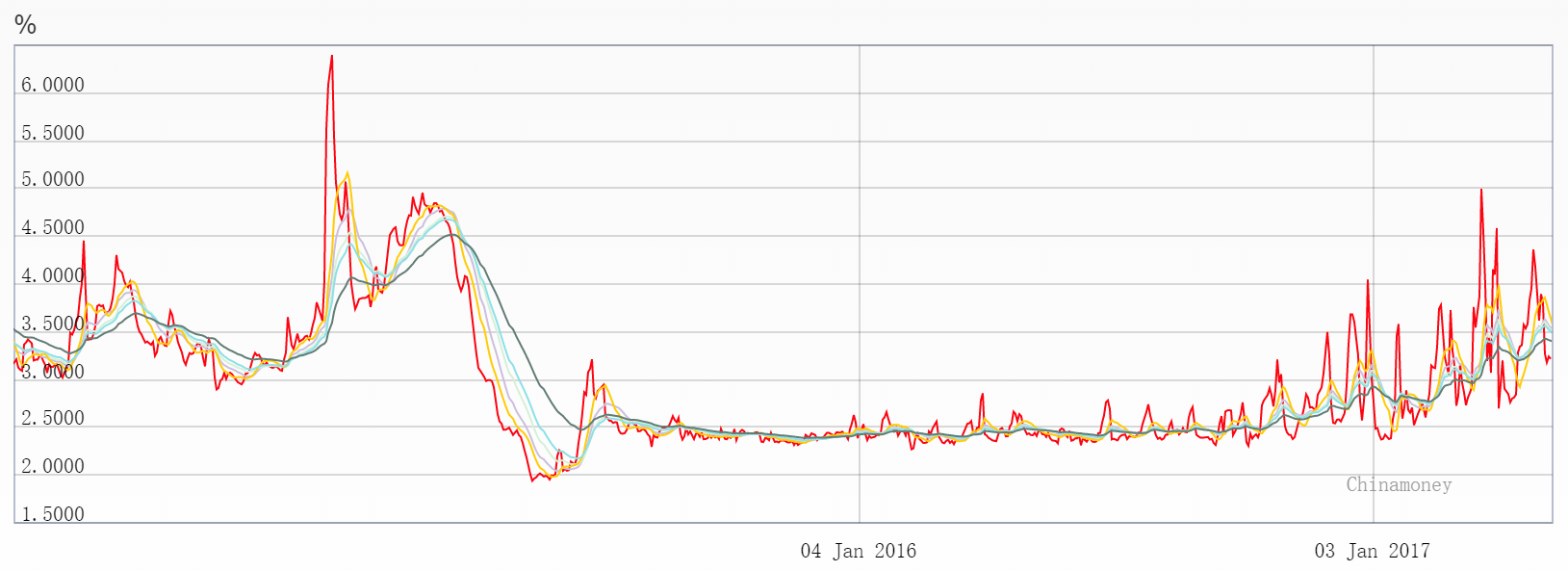

But what’s really going nuts is bond yields:

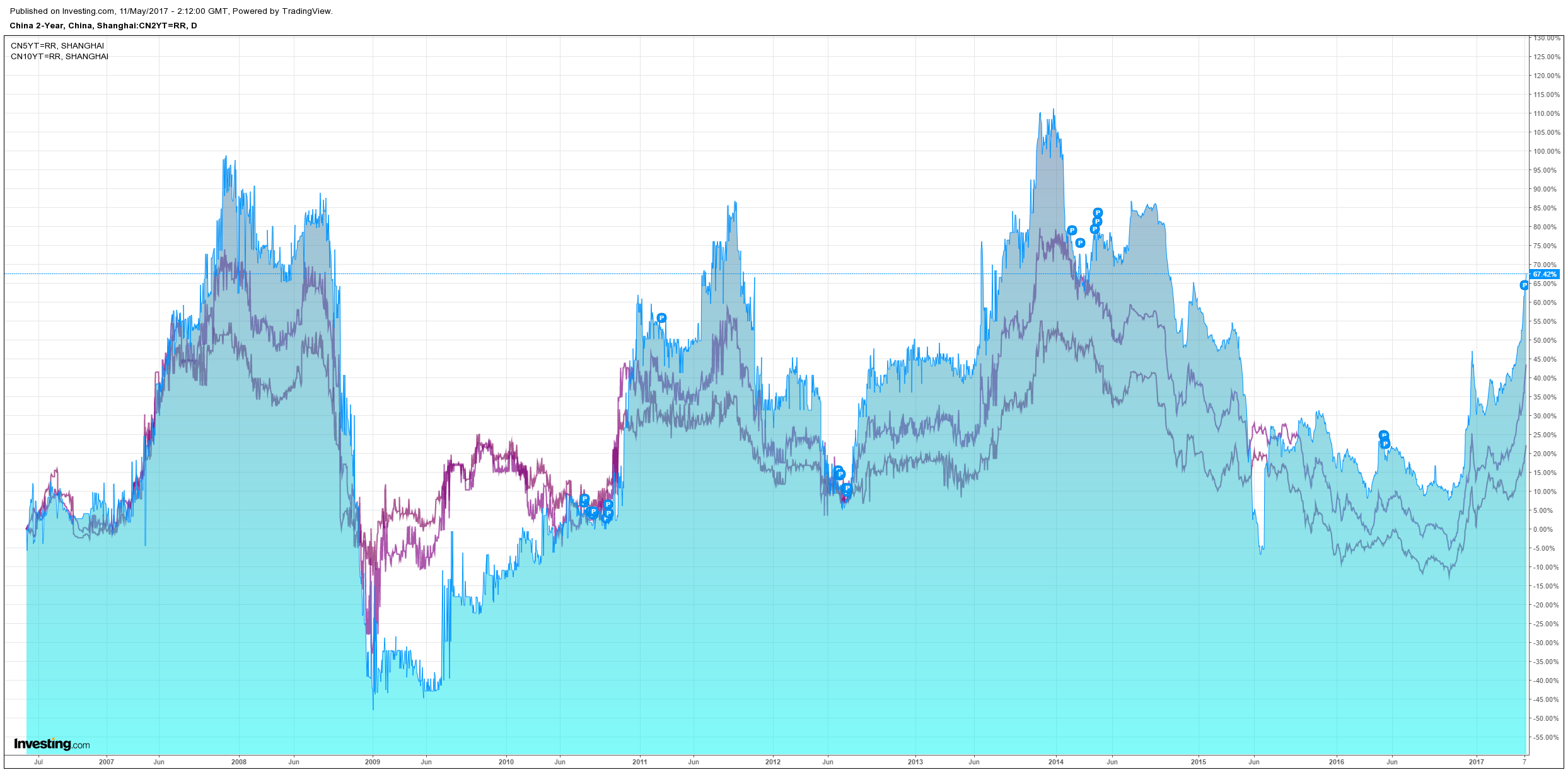

You will have noted, I’m sure, that such bond bear markets have preceded all three major Chinese slowdowns in 2009, 2012 and 2015. The further this runs the more likely it is that we’re entering a serious correction not just blowing a bit of froth off the top.

Advertisement

The full text of this article is available to MacroBusiness subscribers

Cancel at any time through our billing provider, Stripe

About the author

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific's leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.

Advertisement