Blame excessive business profits, not wages for inflation

Recall that the Reserve Bank of Australia (RBA) last month based its 0.25% rate hike, in part, on expected strong wage growth based on industry liaison:

Members observed that information received over the preceding month, particularly through the Bank’s liaison program, had indicated that labour costs were rising at a faster pace and that this was likely to continue. Liaison indicated that many firms were having difficulty hiring workers with the right skills. Given the tight labour market and increase in job mobility, more firms were having to pay higher wages to attract and retain staff, and labour costs were picking up at a faster rate than over the preceding year. Looking ahead, growth in the Wage Price Index (WPI) was forecast to be around 3¾ per cent by the end of the forecast period, which would be the fastest pace since 2012. The outlook for broader measures of labour costs had also been revised up; average earnings were expected to increase at a faster pace than the WPI, as firms turned to bonuses, allowances and other measures to attract and retain workers. While the inertia arising from multi-year enterprise agreements and current public sector wages policies would continue to weigh on aggregate wages growth in the near term, a period of faster growth in labour costs overall was in prospect.

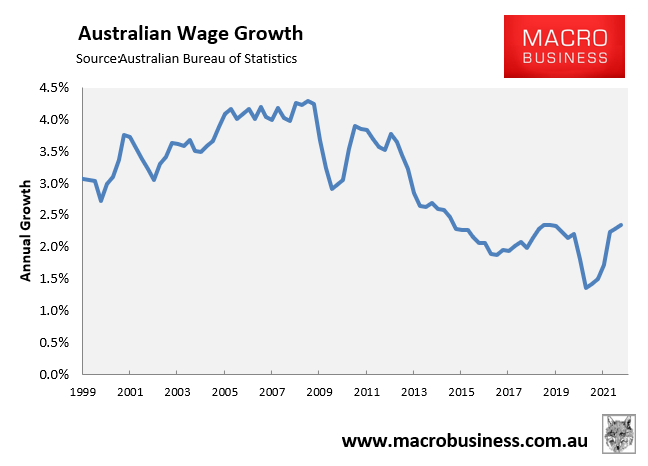

As we all know, the RBA was humiliated by last month’s wage price index, which came in at a tepid 2.35% in the March quarter:

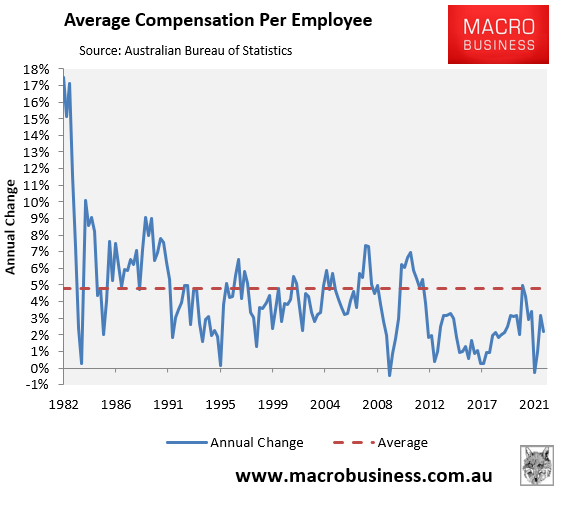

Yesterday’s March quarter National Accounts further humiliated the RBA, with the average compensation of employees rising only 2.2% in the year to March:

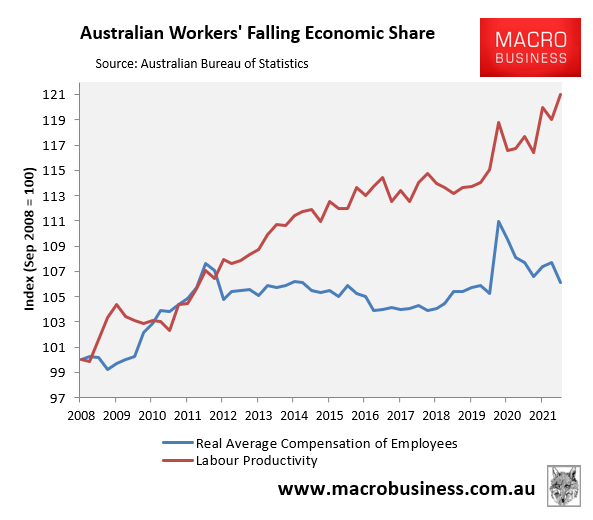

This came despite labour productivity soaring over the past year, according to the national accounts:

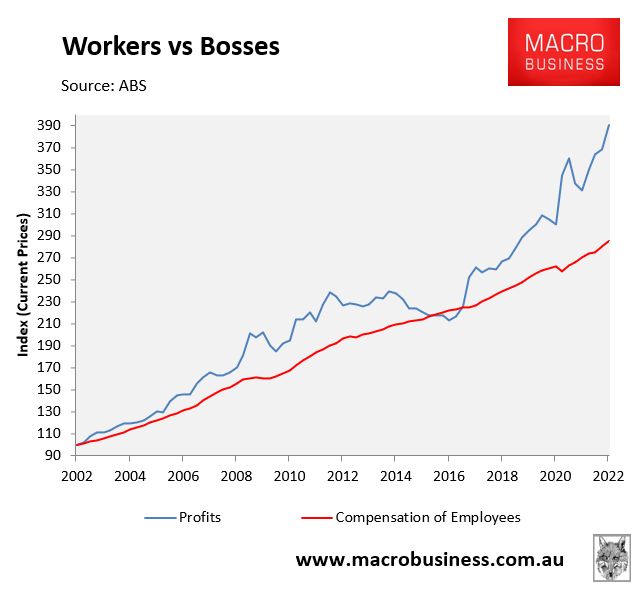

At the same time as workers’ remuneration has languished, company profits have soared to new heights, rising 18.1% in aggregate terms in the year to March versus only a 5.5% rise in aggregate employee compensation:

This has sent the wages share of national income to around the lowest on record at just 49.8%:

The above results completely debunk the business lobby’s claim that inflation-adjusted wage rises would drive up inflation. In reality, profiteering and price gouging from our oligopolistic companies is far more likely to drive inflation than workers’ wage claims.

As noted last month by Jim Stanford from the Centre for Future Work:

Whatever is causing inflation, it isn’t firms passing on higher wage costs to their customers. Some are passing on higher profit margins. If anything, what we are experiencing is more like profit-price inflation than wage-price inflation.

During the COVID crisis, profits climbed to a record high as a share of GDP while labour compensation (mainly wages) fell to its lowest point in postwar history.

Richard Denniss, chief economist at The Australian Institute, made a similar assessment:

In conclusion, given that an economy-wide increase in wages of five percent would have such a small impact on prices, the inflationary risks of a five percent increase in the minimum wage approaches the trivial. Indeed, the risk of firms exaggerating the impact of wage increases on their costs in order to increase their profit margins seems far more significant. In short, it would seem that the ACCC has a bigger role to play in controlling Australia’s inflation than the Fair Work Commission. The abuse of market power, and Australia’s record profit share of GDP represent real threats to Australia’s inflation and macroeconomic performance more generally.

Former ACCC head, Rod Sims, also believes the stronger market power of companies has contributed to higher prices for consumers and lower wages for workers:

“The share of profits in our national income has been rising steadily since the 1970s; and correspondingly the share of national income going to Australia’s workers has been steadily declining since then”…

“We currently have an election discussion about low wages. In the discussion, however, there is little link to Australia’s concentrated economy.”

In short, the business lobby is talking its own book in arguing that wage increases in line with CPI would drive inflation skywards and threaten the economy. If anything, they would deliver productivity gains as firms are forced to innovate and invest in labour-saving technologies.

Besides, if the business lobby is genuinely concerned about inflation, it should look in the mirror at its own price gouging.