Here’s what the Lunatic RBA said in Minutes this week:

Turning to domestic economic conditions, members observed that price pressures were intensifying and there was upward pressure on wages. Activity and conditions in the labour market had been resilient in the face of global and domestic supply shocks, and strong underlying momentum was expected to be sustained over the course of the year.

The key domestic development since the previous meeting was that inflation had increased to its highest rate in many years. Headline inflation was 2.1 per cent in the March quarter and 5.1 per cent over the year. Fuel and new dwelling costs accounted for around half of the quarterly increase. Trimmed mean inflation had increased to 1.4 per cent in the quarter and 3.7 per cent in year-ended terms. This increase in underlying inflation was consistent with a broadening of inflationary pressures.

Information from the Bank’s liaison program indicated that upstream price pressures were increasingly being passed on to final consumer prices of many goods, as supply chain pressures persisted and demand remained strong. Members noted it was possible that firms’ price-setting behaviours were undergoing a change from the pre-pandemic period, with businesses becoming more confident that raising prices would not significantly reduce demand or erode their competitive position.

The forecasts for inflation had been revised materially higher compared with those presented three months earlier. Headline inflation was expected to peak at around 6 per cent in year-ended terms, and trimmed mean inflation at around 4¾ per cent, in the second half of the year. Headline inflation was expected to be boosted by large increases in the prices of fuel and new dwellings over the remainder of 2022, and to remain higher than underlying inflation for some time. As supply-side disruptions eased, both headline and underlying inflation were forecast to moderate to around the top of the 2 to 3 per cent target range by mid-2024. The underlying drivers of inflation were anticipated to evolve over the forecast period, with the effects of global supply-side disruptions and dwelling cost inflation easing while domestic labour costs picked up. These forecasts were based on an assumption of further increases in interest rates, in line with expectations derived from surveys of professional economists and financial market pricing.

In their discussion of the labour market, members noted that conditions had strengthened further since the start of the year and were the tightest in many years. The unemployment rate had been steady in March but had declined over the first quarter as a whole, and the participation rate and employment-to-population ratio were both at historically high levels. High vacancy rates and other leading indicators of labour demand suggested that employment growth was likely to remain strong over the remainder of the year. As a result, the unemployment rate was forecast to decline to around 3½ per cent in early 2023, a little lower than previously expected, and to remain around this level for some time. This would be the lowest rate of unemployment in almost half a century.

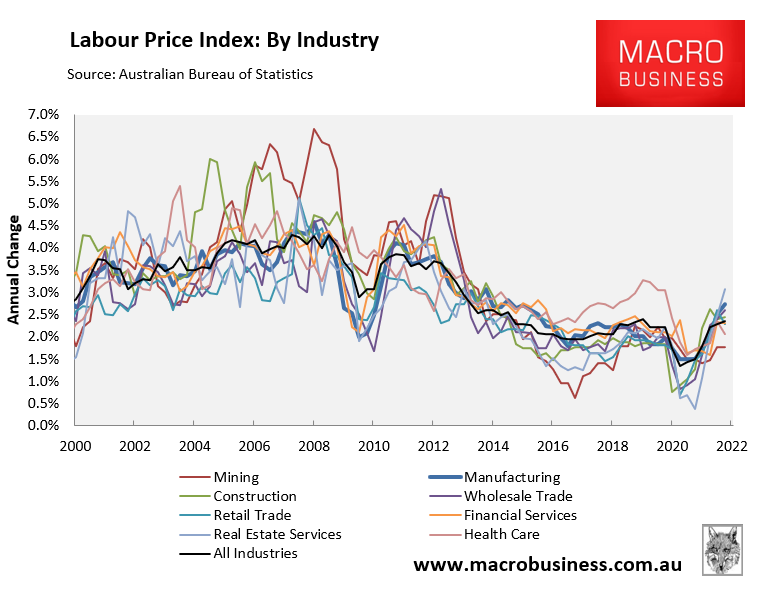

Members observed that information received over the preceding month, particularly through the Bank’s liaison program, had indicated that labour costs were rising at a faster pace and that this was likely to continue. Liaison indicated that many firms were having difficulty hiring workers with the right skills. Given the tight labour market and increase in job mobility, more firms were having to pay higher wages to attract and retain staff, and labour costs were picking up at a faster rate than over the preceding year. Looking ahead, growth in the Wage Price Index (WPI) was forecast to be around 3¾ per cent by the end of the forecast period, which would be the fastest pace since 2012. The outlook for broader measures of labour costs had also been revised up; average earnings were expected to increase at a faster pace than the WPI, as firms turned to bonuses, allowances and other measures to attract and retain workers. While the inertia arising from multi-year enterprise agreements and current public sector wages policies would continue to weigh on aggregate wages growth in the near term, a period of faster growth in labour costs overall was in prospect.

That’s pretty hawkish stuff. Especially for a central bank that a few months ago was going to wait to see wage rises of 3-4% before moving.

And now, the Wage Price Index has missed big:

The RBA needs 0.8% WPI growth next quarter as it falls behind its own schedule. Wages need to keep accelerating from there to nearly 1% per quarter next year, the strongest since the middle of the once per century mining boom ten years ago:

If you read the fine print there you will find an even larger problem. These forecasts assume a path of interest rate rises that is the consensus. That is around 1.5% by year-end and 2.5 % by the end of 2023.

So, according to the RBA, wages are also going accelerate dramatically as house prices crash 20% through the same period, at least in Sydney and Melbourne, and soon enough everywhere else.

There are two more issues as well. One cyclical and one structural.

Global tightening of interest rates is bringing forward the next recession fast. Even the most conservative strategists see it happening by the end of 2023. My bet is it is coming later this year. If so, financial assets and commodity prices will be deflating as well.

Structurally, there is this:

Former competition watchdog Rod Sims says political leaders have failed to link weak wages growth to the stronger market power of companies in banking, beer, groceries, mobile phones, aviation, rail freight, energy retailing, internet search and mobile apps.

In his first major speech since departing the Australian Competition and Consumer Commission in March, Mr Sims said market concentration was high in Australia, which contributed to higher prices for consumers and lower wages for workers.

“The share of profits in our national income has been rising steadily since the 1970s; and correspondingly the share of national income going to Australia’s workers has been steadily declining since then,” Ms Sims said in a speech to the Financial Counselling Australia conference.

I might add, the further from COVID we get, the more migration there will be as well, adding to labour supply.

The weak-kneed RBA should have waited for the wages pressure like it said it would.