Throughout this year, we’ve heard outlandish claims that granting a CPI increase in the minimum wage would cause inflation to soar, driving up mortgage rates.

The most egregious example came from Hospitality king pin Wes Lambert, who claimed the price of a coffee would soar to $7 if the minimum wage was increased “close to CPI”:

“Any minimum wage increase that is close to CPI runs the risk of severely hampering the recovery of the hospitality industry after Covid, as consumers are not going to be prepared for major price increases”…

“I think if the minimum wage increase is CPI or higher, Australian consumers had better be ready for $7 coffees.”

Thankfully, The Australia Institute (TAI) has injected some sense into the debate, showing that wage growth has “played no significant role in the recent surge in inflation” nor would if wages rose in line with headline inflation by 5%. Moreover, the typical $4 coffee would only rise by 9 cents if they sought to pass on the full cost, with the full economy cost rise only 1.85%:

Advertisement

The analysis presented below makes clear that because wages only account for, on average, 25.3 percent of the costs of Australian business there is no reason to expect that a five percent increase in wages could possibly drive price increases of anything like five percent. Needless to say, if only the minimum wage were to rise by five percent, then the impact on business costs would be much lower than that described below. Furthermore, the following analysis ignores labour productivity growth which means the flow on price impacts of a wage increase presented below will be higher than will likely arise as if there is any increase in labour productivity then the impact of a minimum wage rise on total labour costs would be even lower than the estimates provided…

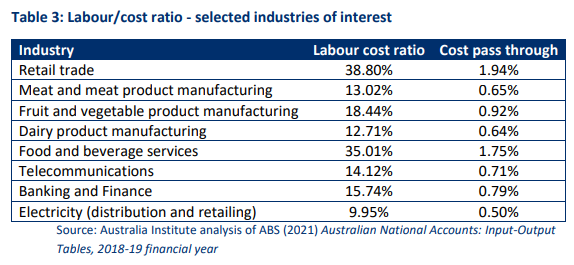

Table 3 features a selection of industries that contain some of the largest employers and that supply some of the key components of the Consumer Price Index. Table 3 makes clear that the processing of meat, fruit, vegetables and milk are not very labour intensive, and would all experience an increase in direct labour costs of less than one percent if all wages paid in those industries (not just the minimum wage) were to increase by five percent. While retail trade and food and beverage services both have significantly higher labour/cost ratios than food processing both would experience an increase in costs of less than two percent, well within the ABS inflation target range, if all wages were to rise by five percent.

Based on the data provided in the ABS Input-output tables the cost of a $4 soy latte at the local café might be expected to increase by around 7 cents if the café wanted to recoup the entire cost of their staff’s five percent wage rise. Such a modest increase sits in stark contrast to suggestions that $7 coffees may soon be on the way in Australia…

Economy-wide impacts

Based on the ABS Input-output tables if there was a uniform five percent wage increase and all industries changed their prices to cover the subsequent increase in their wage costs the average economy-wide price increases would be just 1.27 percent…

According to the ABS Input-output table, including these second round price effects would lead to an average economy-wide price increase of 1.85 percent. To put that into context, while the first round impact of a five percent wage rise on the cost of a $4 soy latte was 7 cents, when the second round impacts are included the café’s costs would likely rise by extra 2 cents to $4.09…

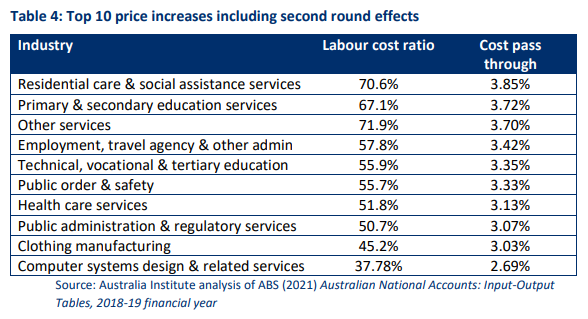

Table 5 shows the ten industries likely to experience the highest cost increases when the second round effects of a five percent economy-wide wage rise are included…

Conclusion

While significant concerns have been raised about the inflationary impacts of a five percent increase in the minimum wage, in reality the direct inflationary impact of a five percent increase in all wages is only 1.27 percent, and even when the second round impacts are included the increase in price level would likely only be 1.85 percent. To put these figures into context, they suggest that the direct impact of a five percent increase in wages on the price of a $4 cup of coffee would be only 7 cents and, even after the second round impacts of increased input costs are included the price increase would only be 9 cents.

The reason that the direct and indirect impacts of wage increases on prices are so low is the fact that wages account for a relatively small portion of the total costs of Australian businesses.

While the estimates of the price impact of wage increases presented above are modest they are likely an overestimate as the Input-output table analysis did not allow firms to substitute away from higher cost inputs for lower cost inputs, and labour costs would be lower if trend rates of labour productivity growth were included. Further, as the industries that are the most labour intensive (and whose costs would rise the most) are dominated by government services for which the price is often set to zero, the economy-wide CPI impact of a price increase would be significantly lower than the figures presented above.

While economy-wide wage increases have a limited impact on prices, attempts by firms to use wage increases as an excuse to increase profit margins the impact of prices is far more significant. For example, if firms only pass on their actual increase in wage costs the impact on prices (after allowing for second round increases in input costs) is only 1.85 percent. Whereas if firms try to increase their prices by an average 2.5 percent in response to the 1.27 percent increase in total costs that would accompany a five percent increase in wage costs then (again after allowing for second round increases in input costs) the price level would increase by 3.73 percent.

In conclusion, given that an economy-wide increase in wages of five percent would have such a small impact on prices, the inflationary risks of a five percent increase in the minimum wage approaches the trivial. Indeed, the risk of firms exaggerating the impact of wage increases on their costs in order to increase their profit margins seems far more significant. In short, it would seem that the ACCC has a bigger role to play in controlling Australia’s inflation than the Fair Work Commission. The abuse of market power, and Australia’s record profit share of GDP represent real threats to Australia’s inflation and macroeconomic performance more generally.

Why is it that the business lobby never complains when housing inflation runs rampant, when private toll road operators like Transurban gouge consumers with hefty toll rises, or about the grotesque Stage 3 Tax Cuts? But when it comes to Australia’s lowest paid workers getting an inflation-matching pay rise amid ‘acute labour shortages’, business groups refuse?

Hand wringing over Australia’s anaemic wage growth hit fever pitch in the years leading up to the pandemic, with politicians, economists, the Reserve Bank and the media all shedding crocodile tears.

Advertisement

But now that workers finally have the upper hand via the tightest labour market in generations, and wages pressures are beginning to manifest, wage rises are all of a sudden considered dangerous and must fall in real terms?

Leith van Onselen is Chief Economist at the MB Fund and MB Super. He is also a co-founder of MacroBusiness.

Leith has previously worked at the Australian Treasury, Victorian Treasury and Goldman Sachs.