Societe Generale with the note:

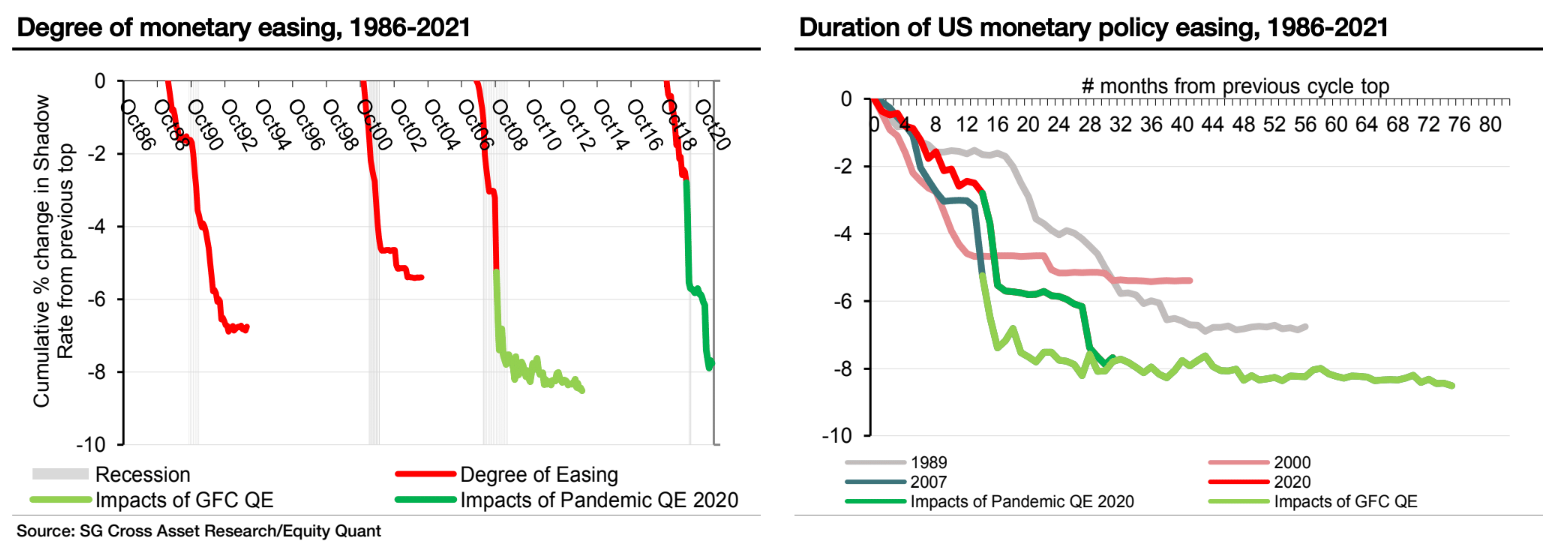

The ongoing post-pandemic monetary easing cycle started with the first rate cut of July 2019 after tightening reached a peak in December 2018. After two cuts, the Fed policy rate had declined to 1.75% by February 2020 from a tightening peak of 2.5%. With the global pandemic bringing economies to a stand-still, monetary policy went into overdrive in the following month, with further rate cuts and a series of unconventional QE policies that provided extraordinary liquidity support. As a consequence, the shadow rate, reflecting the overall monetary policy stance, fell precipitously by a total of about 790bps, and appeared to have bottomed out by the end of May 2021. This compares well with the plunge of about 850 bps in shadow rates at the trough of the post-GFC easing cycle in November2013. Given that the economic slowdown that precipitated the easing cycle was not a cyclical downturn typical of normal business cycles, this was one of the shortest easing phases historically. It was also a testbed of massive unconventional policies.

Focusing on the most recent cycles, the figure below shows the degree of monetary easing since the mid-1980s. In the last two cycles, unconventional policy measures in the form of QE have contributed a large part of monetary easing. In the post-GFC cycle of monetary easing, after three rounds of QE, forward guidance and other unconventional policies, the cumulative short rate fell by 850 bps over an extended period of five years, bottoming out in November 2013, a month before the start of QE tapering. In the process, the QE measures accounted for about 62% of the total monetary easing during the cycle. Of the total monetary easing provided in the ongoing post-pandemic monetary easing cycle (790 bps), by our estimates, more than65% could be attributed to the series of large-scale QE measures implemented in 2020.

The full text of this article is available to MacroBusiness subscribers