Earlier this week we argued that the Reserve Bank of Australia (RBA) was fighting the Morrison Government on wages, given recent comments from governor Phil Lowe that low immigration is required to achieve the Bank’s goal of lowering unemployment and lifting wage growth.

Yesterday, Governor Phil Lowe took his wages jawboning to another level in a speech to Economic Society of Australia. In this speech, Lowe explicitly noted that lifting immigration will unambiguously hurt wage growth [my emphasis]:

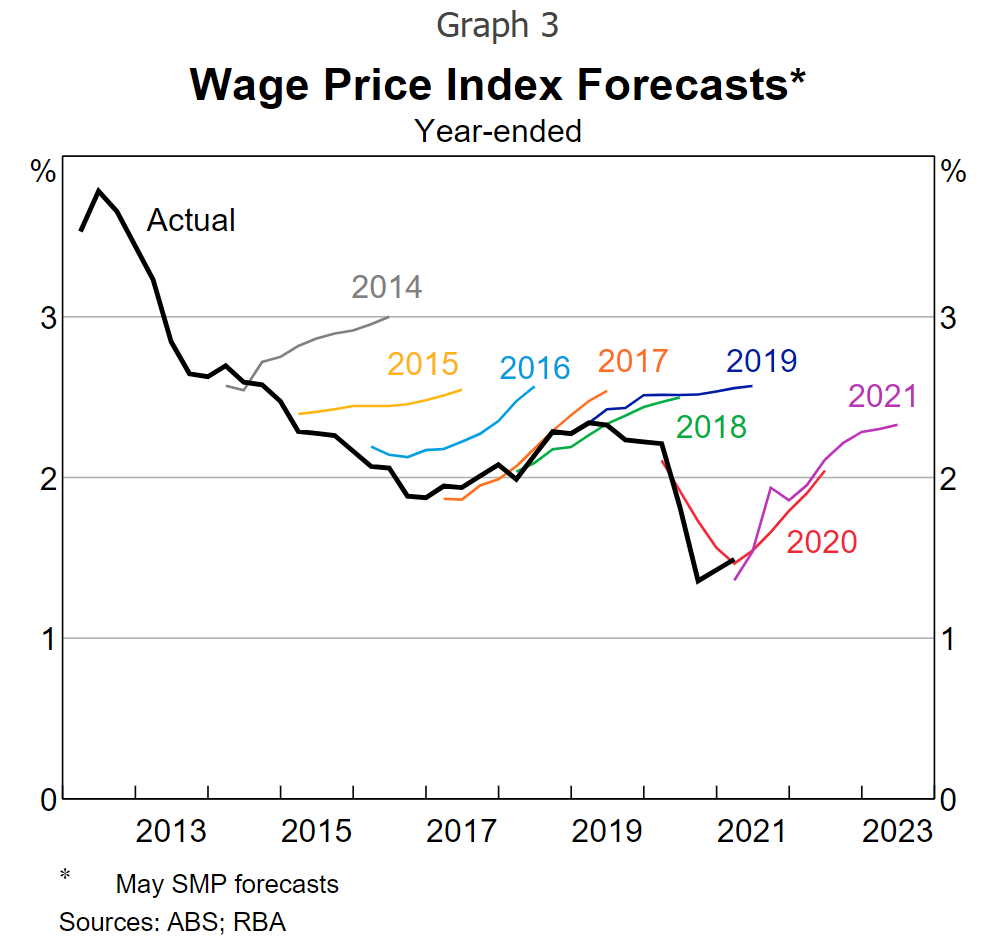

This combination of surprisingly positive employment growth and subdued wages growth had become a familiar pattern before the pandemic. This is evident in the next couple of graphs. The first shows the RBA’s successive forecasts for growth in the WPI from 2014 (Graph 3). The picture is very clear: wages growth was persistently lower than forecast.

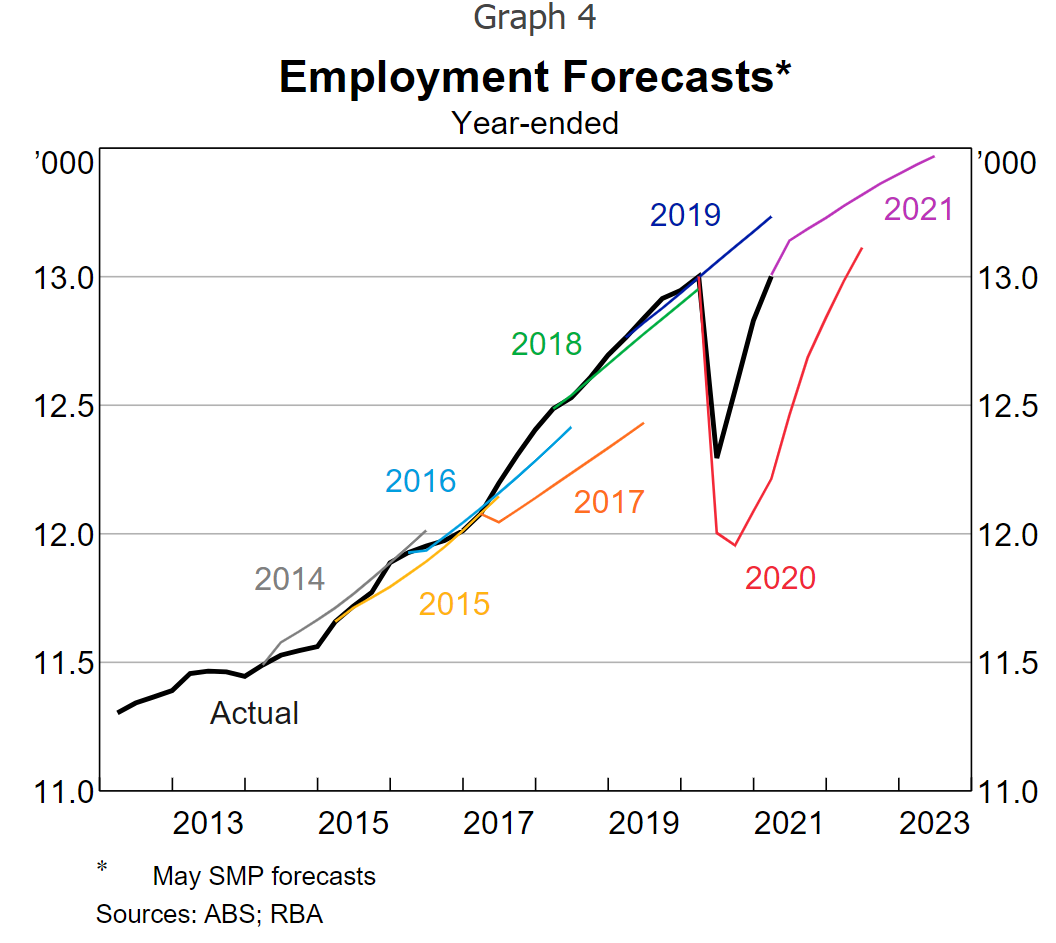

The next graph is similar, but shows successive forecasts for the level of employment (Graph 4). The picture here is not quite as clear, but employment growth has mostly been in line with, or exceeded, expectations, with the obvious exception of last year…

Strong growth in labour demand was closely matched by a strong increase in labour supply. With both demand and supply rising, there was little need for the price – that is wages – to move…

[One] supply side factor is the ability that firms have had to draw on overseas workers when skills or workers were in short supply in Australia… This hiring dilutes the upward pressure on wages in these hotspots and it is possible that there are spillovers to the rest of the labour market. This hiring can also dilute the incentive for businesses to train workers to do the required job…

In conceptual terms, one can think of this ability to tap into the global labour market for workers that are in short supply as flattening the supply curve for these workers. A flat supply curve means that a shift in demand has only a small effect on prices, or in this case wages. In my view, this is one of the factors that has contributed to wages being less sensitive to shifts in demand than was once the case…

Strong labour demand was met with a strong supply response. The result was that the price of labour did not move much…

So what does this all mean for the future?

The big change on the supply side has been the closure of our international borders. This has contributed to labour shortages in some areas given the strong pick-up in labour demand. In turn, some workers have received sizeable wage increases…

Given this experience, an important consideration for the outlook is how long the borders remain closed.

One plausible scenario is that they open gradually over the period ahead, especially for workers with skills that are in short supply. This would relieve some of the current pressure points in the labour market. Alternatively, it is also possible that the borders remain closed for an extended period and that the pressure points build further. If so, aggregate wages growth would pick up more quickly than currently expected, but production and investment would be also be constrained…

While it is hard to be sure, it is likely that the unemployment rate will need to be sustained in the low 4s for the Australian economy to be considered to be operating at full employment. Underemployment will also need to decline further. To achieve this, a further period of strong employment growth will be required…

These are important conclusions from a policy perspective, especially given the RBA’s strategy is to get the unemployment rate down so that wages growth picks up and inflation returns in a sustainable way to the target range.

Phil Lowe expanded on these comments further in the Q&A section:

Advertisement

“The last time that wages growth in Australia was above 3% was a decade ago. It took a decade to go from 3% to 1.5%… I don’t see those factors going away quickly. They were there for a decade… The grind higher in wages will be slow… If wages growth is going to have a s in front of it, it is going to be very difficult for us to deliver inflation…

“The reason why the private sector has stronger wage growth forecasts is that the closure in the borders will lead to a hot house environment and wages will rise more quickly. That’s possible. But I think it is more plausible that eventually the borders open again and some of the hot house pressures in the labour market dissipate…

So according to Phil Lowe:

Australia’s high levels of immigration has contributed to the nation’s low wages growth of recent years; and

High immigration has given businesses an incentive not to train their workers.

This helps explain why business groups lobby so hard for immigration, since it holds their wage costs down, abrogates their need to provide training, and expands the number of people to sell goods and services to.

Advertisement

Basically, Australia has run a Work Choices immigration system – designed specifically to neuter Australian workers and fatten company profits.

As far as we are aware, Phil Lowe is the first RBA governor to have directly linked Australia’s high immigration program with the country’s weak wage growth. In doing so, he has fired a direct shot at the federal government’s and Australian Treasury’s desire to reboot immigration back to pre-COVID levels at the earliest opportunity. He has also successfully lit a fuse under the Big Australia debate.

The Labor Opposition should (but probably won’t) stand up and take a lower immigration policy to the upcoming federal election. Not only is it the right thing to do for Australian workers, but it also has the backing of the RBA.

Advertisement

Finally, this moment cannot pass without a brief recognition that the RBA’s new regime is exactly the same as the arguments prosecuted by MacroBusiness for nearly a decade (including regularly schooling the RBA – e.g. here, here, here, here, here and here). In particular, Leith van Onselen, who for his trouble has received very little public recognition, and a whole lot of abuse from the racially obsessed pork chops of the left.

A memo to the lot you. Interpreting data and facts with fierce objectivity is what public intellectualism is all about.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific's leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.