Australia’s industry superannuation funds continue to scaremonger against freezing the compulsory superannuation guarantee (SG) at the current 9.5%, warning that it will rob workers, leave taxpayers worse off, and increase inequality:

Industry funds are calling on the government to release a retirement income report which could potentially change the amount of superannuation paid by employers to their workers…

Industry Super Australia (ISA), which represents 15 industry funds… said the review could unwind the legislated increase in superannuation guarantee payments, which will force employers to pay 12 per cent in contributions to workers instead of the current 9.5 per cent…

According to ISA, eight million Australians would be negatively impacted by the scrapping of the scheduled rise in superannuation contributions made by employers.

“For an average 30-year-old couple working full time, cutting the super guarantee increase would deprive them of up to $200,000 in super by the time they retire,” ISA said…

“Super is already a great economic leveller for most Australians but we need to do more to avoid us ending up as divided nation, with millions of women and low-income earners scraping by just on the aged pension,” he said…

“The government needs to keep policy stable and stick with the legislated increases in super. That’s the proven and best way to get workers savings and the economy going again.”

The notion that the SG is paid for by employers is demonstrably false. It is paid by workers via lower take home wages. This was confirmed by the Henry Tax Review, the Reserve Bank of Australia, the Grattan Institute. and the Government paper announcing the establishment of compulsory superannuation in 1992, entitled Security in Retirement: Planning for Tomorrow Today.

Thus, lifting the SG by 2.5% would lower wage growth by a similar amount (other things equal), in turn reducing consumption across the economy. Given Australia is experiencing a deep recession, this constitutes an additional risk to recovery.

ISA’s claim that superannuation “is a great economic leveller for most Australians” could also not be more wrong. By reducing their take home pays, the SG hits lower-income earners especially hard, leaving them with less to live on.

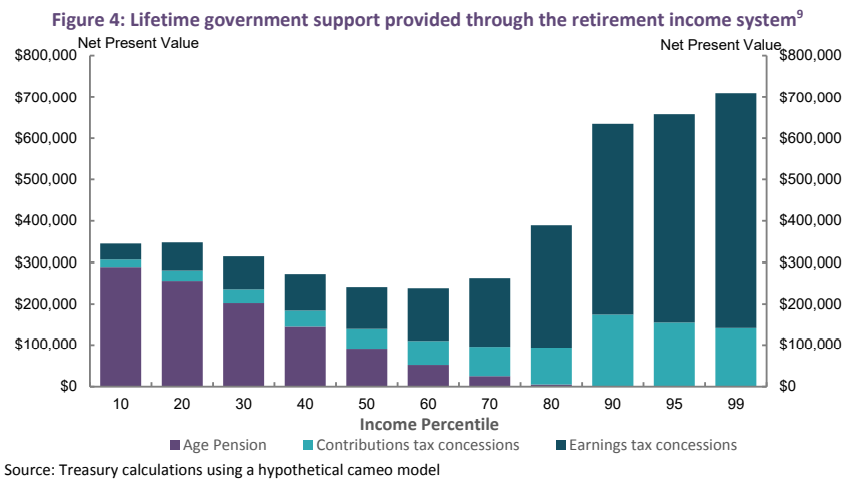

The SG also increases inequality, since the lion’s share of concessions flow to high income earners:

So in actual fact, the superannuation system works more like a tax avoidance scheme for the rich than a genuine retirement pillar.

Finally, lifting the SG by 2.5% would worsen the long-term sustainability of the Budget. This is because the cost of superannuation concessions outweighs the benefits from lower pension outlays.

The main beneficiaries from raising the SG to 12% are superannuation funds, as they would be able to skim bigger fees from more funds under management. But this would come at the direct expense of ordinary Australians.