Industry Super Australia (ISA) has spun more propaganda claiming that if the Morrison Government overturns the legislated increase in the superannuation guarantee (SG) to 12%, it will punish future taxpayers:

ISA slammed backbench MPs for attempting to dump the increase of the super guarantee from 9.5 per cent to 12 per cent by 2025, with a scheduled increase to 10 per cent set to take place from 1 July 2021.

“If those MPs get their way, more workers would be more reliant on the aged pension – a bill everyone pays through higher taxes,” ISA stated.

“The Prime Minister and Treasurer must stick by their promise to increase the super rate because it’s critical to helping these people rebuild savings they’ve wiped out, and avoid tax hikes on working people to prop up more people drawing a full pension,” [ISA chief executive Bernie Dean said].

ISA obviously believes that if is repeats a lie often enough, it becomes true.

Australia’s compulsory superannuation system unambiguously costs the federal budget ($43 billion a year currently) more than it saves in Aged Pension costs.

Advertisement

Don’t just take my word for it. Here’s actuarial firm Rice Warner:

Actuarial firm Rice Warner said that lifting compulsory super contributions to 12% would not have much impact on the age pension for many years, and would save the budget only about 0.1% in lower age pension spending in the second half of this century.

In contrast, extra super tax breaks from higher compulsory super would cost an average of 0.22% of GDP “through this century”…

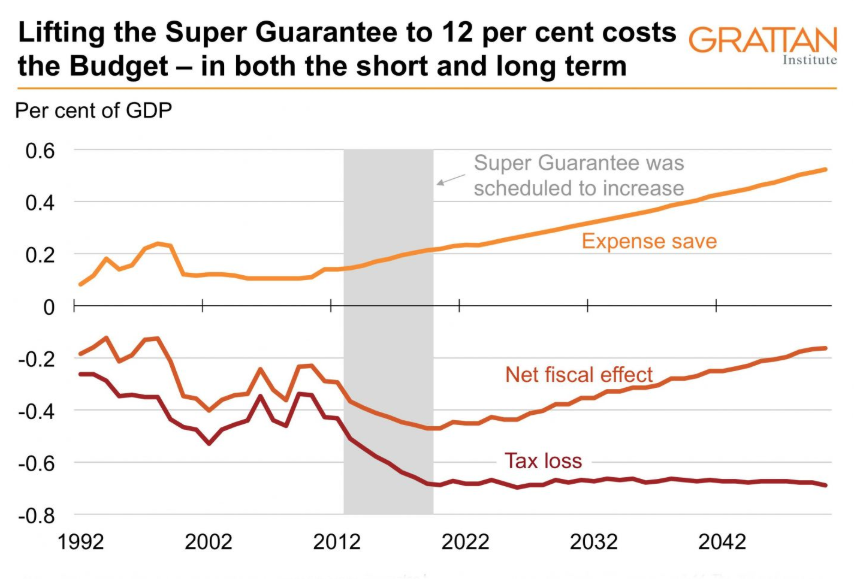

Here’s the Grattan Institute, which estimated that lifting the SG to 12% would cost the federal budget another $2 billion a year and would far outweigh any benefits from lower Aged Pension payments:

Advertisement

The purpose of superannuation is to save for the future and reduce future age-pension payments. In both the short and long term, though, superannuation costs the budget more than it saves, because the tax breaks cost the government more than the pension savings.

An increase in the superannuation guarantee would … have a net cost to government revenue even over the long term (that is, the loss of income tax revenue would not be replaced fully by an increase in superannuation tax collections or a reduction in Age Pension costs).

Advertisement

The main reason why compulsory superannuation fails to relieve the federal budget is because it lavishes tax concessions on those that do not need it and were never going to become reliant on the Aged Pension – i.e. high income earners. This was explained by The Australia Institute’s chief economist, Richard Denniss, earlier this year:

This year, the government will spend more than $41 billion on tax concessions for superannuation with the stated purpose of helping people save for their retirement. But the way the rules are designed give the vast majority of that money to people who will already retire comfortably…

60 per cent of superannuation tax concessions go to the top 20 per cent of households, with just 11 per cent going to the bottom half of all Australian households…

Superannuation tax concessions aren’t just enormous and unfair, though: they are also growing – at about 8.5 per cent a year, twice the rate of growth for the age pension…

One of the biggest justifications for putting 9.5 per cent of our wage into superannuation, and for spending $41 billion a year on tax concessions for that super, is that it “takes pressure off the age pension system”. The only problem with this argument is that it’s not true. Not even close.

ISA is once again talking its own book in lobbying for an increase in the SG to 12%. Because doing so would boost ISA members’ funds under management and fees, courtesy of the Australian taxpayer.

Leith van Onselen is Chief Economist at the MB Fund and MB Super. He is also a co-founder of MacroBusiness.

Leith has previously worked at the Australian Treasury, Victorian Treasury and Goldman Sachs.